9Introduction to Correlation and Regression Analysis

9.1 Introduction

The distinction between correlation and causation represents a fundamental challenge in statistical analysis. While correlation measures the statistical association between variables, causation implies a direct influence of one variable on another.

Statistical relationships form the backbone of data-driven decision making across disciplines—from economics and public health to psychology and environmental science. Understanding when a relationship indicates mere association versus genuine causality is crucial for valid inference and effective policy recommendations.

9.2 Covariance

Covariance measures how two variables vary together, indicating both the direction and magnitude of their linear relationship.

cat("\nStandard deviation of X:", sd(study_hours))

Standard deviation of X: 3.162278

cat("\nStandard deviation of Y:", sd(test_scores))

Standard deviation of Y: 11.93734

# Calculate confidence interval and p-valuecor_test <-cor.test(study_hours, test_scores, method ="pearson")print(cor_test)

Pearson's product-moment correlation

data: study_hours and test_scores

t = 15, df = 3, p-value = 0.0006431

alternative hypothesis: true correlation is not equal to 0

95 percent confidence interval:

0.8994446 0.9995859

sample estimates:

cor

0.9933993

Interpretation: r = 0.994 indicates an almost perfect positive linear relationship between study hours and test scores. The p-value < 0.05 suggests this relationship is statistically significant.

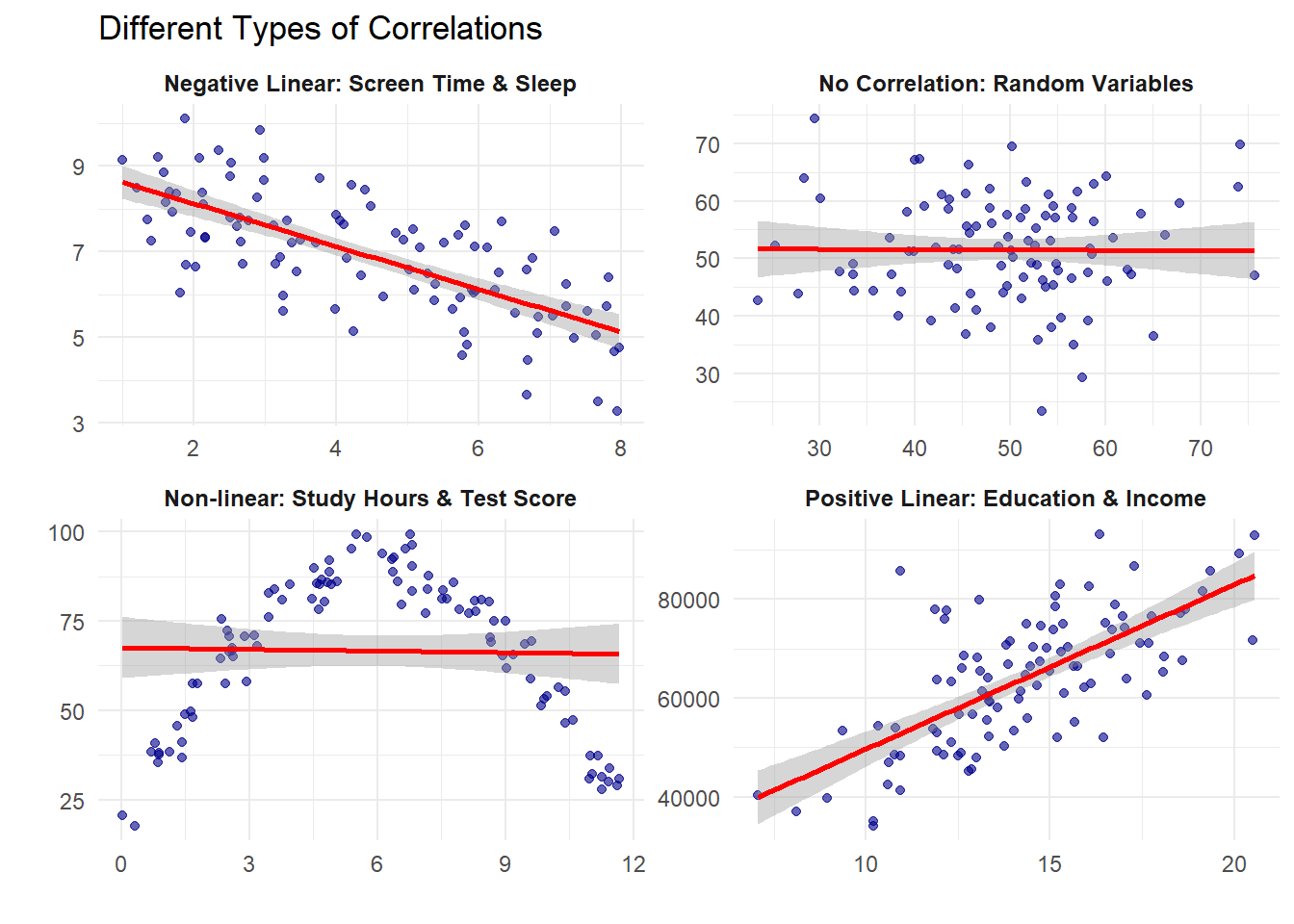

9.5 Spearman Rank Correlation

Spearman correlation measures monotonic relationships using ranks instead of raw values.

r = 0.85 between hours of practice and performance score

Answer: Strong positive relationship. As practice hours increase, performance scores tend to increase substantially.

r = -0.72 between outside temperature and heating costs

Answer: Strong negative relationship. As temperature increases, heating costs decrease substantially.

r = 0.12 between shoe size and intelligence

Answer: Very weak/no meaningful relationship. Shoe size and intelligence are essentially unrelated.

9.8 Important Points to Remember

Correlation measures relationship strength: Values range from -1 to +1

Correlation ≠ Causation: High correlation doesn’t prove one variable causes another

Choose the right method:

Pearson: For linear relationships in continuous data

Spearman: For monotonic relationships or ranked data

Check assumptions:

Pearson assumes linear relationship and normal distribution

Spearman only assumes monotonic relationship

Watch for outliers: Extreme values can greatly affect Pearson correlation

Visualize your data: Always plot before calculating correlation

9.9 Summary: Decision Tree for Correlation Analysis

CHOOSING THE RIGHT CORRELATION METHOD:

Is your data numerical?

├─ YES → Is the relationship linear?

│ ├─ YES → Use PEARSON correlation

│ └─ NO → Is it monotonic?

│ ├─ YES → Use SPEARMAN correlation

│ └─ NO → Consider non-linear methods

└─ NO → Is it ordinal (ranked)?

├─ YES → Use SPEARMAN correlation

└─ NO → Use CROSS-TABULATION for categorical data

Quick Reference Card

Measure

Use When

Formula

Range

Covariance

Initial exploration of relationship

\frac{\sum(x_i-\bar{x})(y_i-\bar{y})}{n-1}

-∞ to +∞

Pearson r

Linear relationships, continuous data

\frac{\text{cov}(X,Y)}{s_X s_Y}

-1 to +1

Spearman ρ

Monotonic relationships, ranked data

1 - \frac{6\sum d_i^2}{n(n^2-1)}

-1 to +1

Cross-tabs

Categorical variables

Frequency counts

N/A

9.10 Understanding Ordinary Least Squares (OLS): A Quick-start Guide

Understanding Ordinary Least Squares (OLS): A Quick-start Guide

Introduction: What is Regression Analysis?

Regression analysis helps us understand and measure relationships between things we can observe. It provides mathematical tools to identify patterns in data that help us make predictions.

Consider these research questions:

How does study time affect test scores?

How does experience affect salary?

How does advertising spending influence sales?

Regression gives us systematic methods to answer these questions with real data.

The Starting Point: A Simple Example

Let’s begin with something concrete. You’ve collected data from 20 students in your class:

Student

Study Hours

Exam Score

Alex

2

68

Beth

4

74

Carlos

6

85

Diana

8

91

…

…

…

When you plot this data, you get a scatter plot with dots all over. Your goal: find the straight line that best describes the relationship between study hours and exam scores.

But what does “best” mean? That’s what we’ll discover.

Why Real Data Doesn’t Fall on a Perfect Line

Before diving into the math, let’s understand why data points don’t line up perfectly.

Deterministic vs. Stochastic Models

Deterministic Models describe relationships with no uncertainty. Think of physics equations: \text{Distance} = \text{Speed} × \text{Time}

If you drive at exactly 60 mph for exactly 2 hours, you’ll always travel exactly 120 miles. No variation, no exceptions.

Stochastic Models acknowledge that real-world data contains natural variation. The fundamental structure is: Y = f(X) + \epsilon

Where:

Y is what we’re trying to predict (exam scores)

f(X) is the systematic pattern (how study hours typically affect scores)

\epsilon (epsilon) represents all the random stuff we can’t measure

In our example, two students might study for 5 hours but get different scores because:

One slept better the night before

One is naturally better at test-taking

One had a noisy roommate during the exam

Pure chance in which questions were asked

This randomness is natural and expected - that’s what \epsilon captures.

The Simple Linear Regression Model

We express the relationship between study hours and exam scores as: Y_i = \beta_0 + \beta_1X_i + \epsilon_i

Let’s decode this:

Y_i = exam score for student i

X_i = study hours for student i

\beta_0 = the intercept (baseline score with zero study hours)

\beta_1 = the slope (points gained per study hour)

Key insight: We never know the true values of \beta_0 and \beta_1. Instead, we use our data to estimate them, calling our estimates \hat{\beta}_0 and \hat{\beta}_1 (the “hats” mean “estimated”).

Understanding Residuals: How Wrong Are Our Predictions?

Once we draw a line through our data, we can make predictions. For each student:

Actual score (y_i): What they really got

Predicted score (\hat{y}_i): What our line says they should have gotten

Residual (e_i): The difference = Actual - Predicted

So a student studying 5 hours: Predicted score = 60 + 4(5) = 80 points

Effect Size and Practical Significance

Statistical significance tells us whether an effect exists. Practical significance tells us whether it matters. Understanding both is crucial for proper interpretation.

Calculating and Interpreting Raw Effect Sizes

The raw (unstandardized) effect size is simply your slope coefficient \hat{\beta}_1.

Example: If \hat{\beta}_1 = 4 points per hour:

This is the raw effect size

Interpretation: “One hour of additional study yields 4 exam points”

To assess practical significance, consider:

Scale of the outcome: 4 points on a 100-point exam (4%) vs. 4 points on a 500-point exam (0.8%)

Cost of the intervention: Is one hour of study time worth 4 points?

Context-specific thresholds: Does 4 points change a letter grade?

Calculating Standardized Effect Sizes

Standardized effects allow comparison across different scales and studies.

Formula for standardized coefficient (beta weight):\beta_{std} = \hat{\beta}_1 \times \frac{s_X}{s_Y}

Where:

s_X = standard deviation of X (study hours)

s_Y = standard deviation of Y (exam scores)

Step-by-step calculation:

Calculate the standard deviation of X: s_X = \sqrt{\frac{\sum(x_i - \bar{x})^2}{n-1}}

Calculate the standard deviation of Y: s_Y = \sqrt{\frac{\sum(y_i - \bar{y})^2}{n-1}}

Nachylenie / Slope (\beta_1) PL: Przy wzroście X o 1 jednostkę (ceteris paribus), przeciętna wartość Y zmienia się o \beta_1 jednostek. ENG: When X increases by 1 unit (ceteris paribus), the expected value of Y changes by \beta_1 units.

gdzie s_X i s_Y to odchylenia standardowe X i Y. PL: Przy wzroście X o 1 odchylenie standardowe (SD), przeciętna wartość Y zmienia się o \beta_{1}^{(\mathrm{std})}odchyleń standardowychY. ENG: For a 1 standard deviation (SD) increase in X, the expected value of Y changes by \beta_{1}^{(\mathrm{std})}SDs ofY. Uwaga/Note: W regresji prostej \beta_{1}^{(\mathrm{std})} = r (Pearson). / In simple regression, \beta_{1}^{(\mathrm{std})} = r (Pearson).

PL: Model wyjaśnia 100\times R^2% zmienności Y względem modelu tylko z wyrazem wolnym (in-sample). ENG: The model explains 100\times R^2% of the variance in Y relative to the intercept-only model (in-sample). W wielu zmiennych rozważ: \text{adjusted } R^2. / With multiple predictors consider: adjusted R^2.

Wartość p / P-valueFormalnie/Formally:

p \;=\; \Pr\!\big(\,|T|\ge |t_{\mathrm{obs}}| \mid H_0\,\big),

gdzie T ma rozkład t przy H_0. PL: Zakładając prawdziwość H_0 i spełnione założenia modelu, prawdopodobieństwo uzyskania co najmniej tak ekstremalnej statystyki jak obserwowana wynosi p. ENG: Assuming H_0 and the model assumptions hold, p is the probability of observing a test statistic at least as extreme as the one obtained.

Przedział ufności / Confidence interval (np. dla\beta_1) Konstrukcja/Construction:

PL (ściśle): W długiej serii powtórzeń 95% tak skonstruowanych przedziałów zawiera prawdziwą wartość \beta_1; dla naszych danych oszacowanie mieści się w [\text{lower},\ \text{upper}]. ENG (strict): Over many repetitions, 95% of such intervals would contain the true \beta_1; for our data, the estimate lies within [\text{lower},\ \text{upper}]. PL (skrót dydaktyczny): „Jesteśmy 95% pewni, że \beta_1 leży w [\text{lower},\ \text{upper}].” ENG (teaching shorthand): “We are 95% confident that \beta_1 lies in [\text{lower},\ \text{upper}].”

Najczęstsze nieporozumienia / Common pitfalls

PL:pnie jest prawdopodobieństwem, że H_0 jest prawdziwa. ENG:p is not the probability that H_0 is true.

PL: 95% CI nie zawiera 95% obserwacji (od tego jest przedział predykcji). ENG: A 95% CI does not contain 95% of observations (that’s a prediction interval).

PL/ENG: Wysokie R^2 ≠ przyczynowość / High R^2 ≠ causality. Zawsze sprawdzaj/Always check diagnozy reszt, skalę efektu, i dopasowanie poza próbą.

Critical Reminders:

Association does not imply causation

Statistical significance does not guarantee practical importance

Every model is wrong, but some are useful

Always visualize your data and residuals

Consider both effect size and uncertainty when making decisions

OLS provides a principled, mathematical approach to finding patterns in real-world data. While it cannot provide perfect predictions, it offers the best linear approximation possible along with honest assessments of that approximation’s quality and uncertainty.

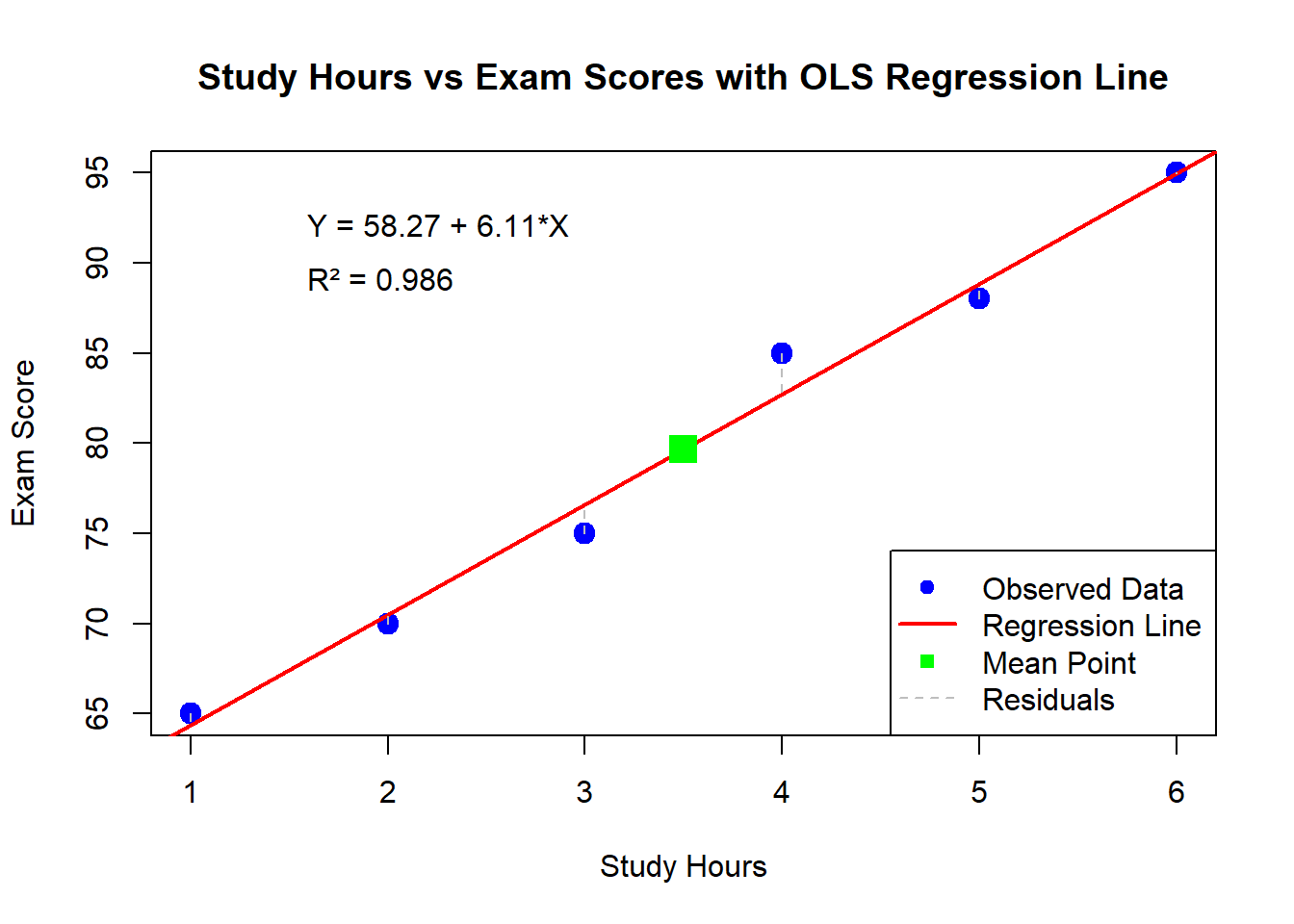

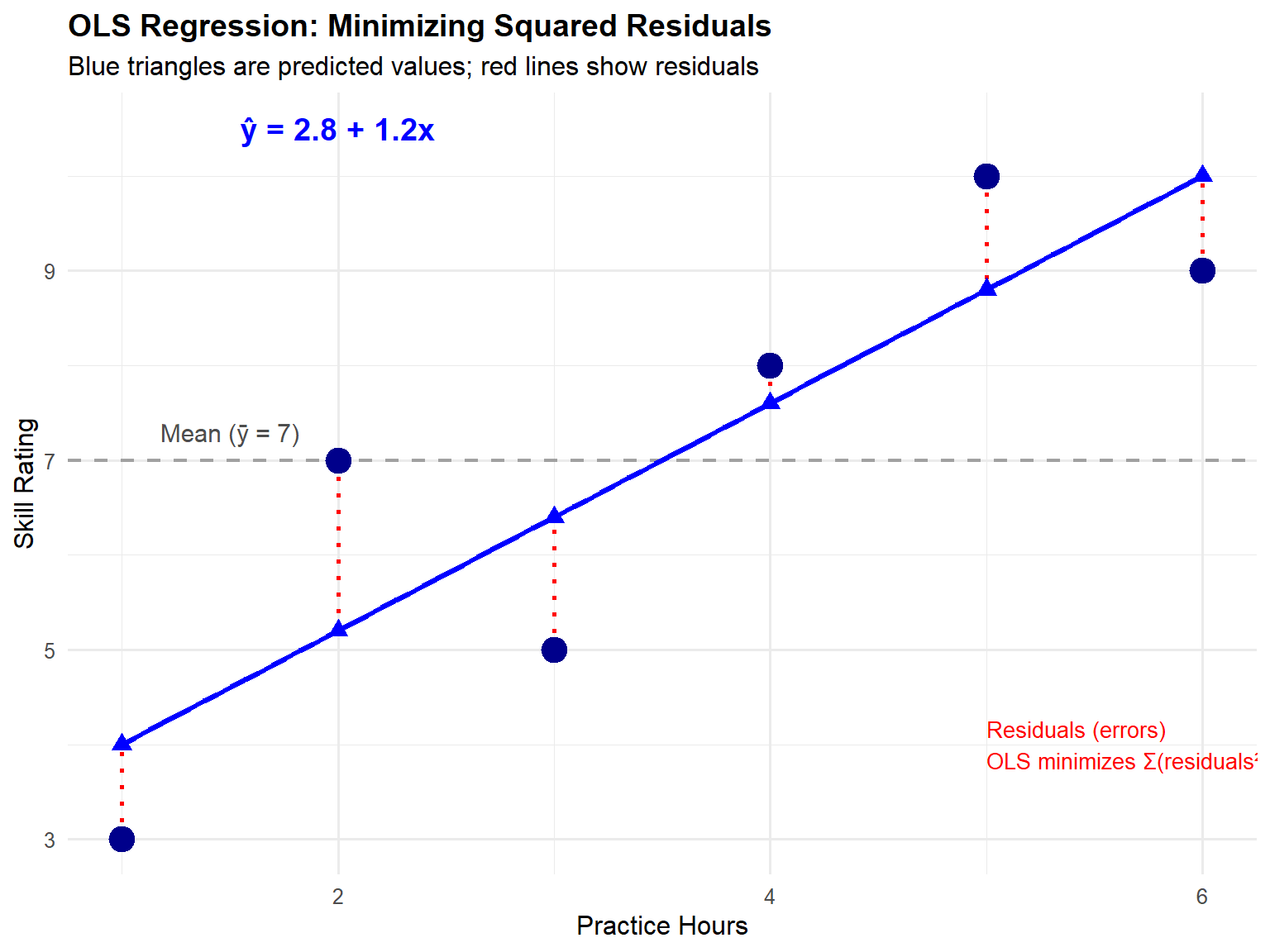

9.11 Complete Manual OLS Calculation: A Step-by-Step Example

A professor wants to understand the relationship between hours spent studying and exam scores. She collects data from 6 students:

Student

Study Hours (X)

Exam Score (Y)

A

1

65

B

2

70

C

3

75

D

4

85

E

5

88

F

6

95

Our goal: Find the best-fitting line \hat{Y} = \hat{\beta}_0 + \hat{\beta}_1X using OLS.

9.12 Step 1: Calculate the Means

First, we need the mean of X and Y.

For X (study hours):\bar{X} = \frac{1 + 2 + 3 + 4 + 5 + 6}{6} = \frac{21}{6} = 3.5

For Y (exam scores):\bar{Y} = \frac{65 + 70 + 75 + 85 + 88 + 95}{6} = \frac{478}{6} = 79.67

9.13 Step 2: Calculate Deviations from Means

For each observation, calculate (X_i - \bar{X}) and (Y_i - \bar{Y}):

Student

X_i

Y_i

X_i - \bar{X}

Y_i - \bar{Y}

A

1

65

1 - 3.5 = -2.5

65 - 79.67 = -14.67

B

2

70

2 - 3.5 = -1.5

70 - 79.67 = -9.67

C

3

75

3 - 3.5 = -0.5

75 - 79.67 = -4.67

D

4

85

4 - 3.5 = 0.5

85 - 79.67 = 5.33

E

5

88

5 - 3.5 = 1.5

88 - 79.67 = 8.33

F

6

95

6 - 3.5 = 2.5

95 - 79.67 = 15.33

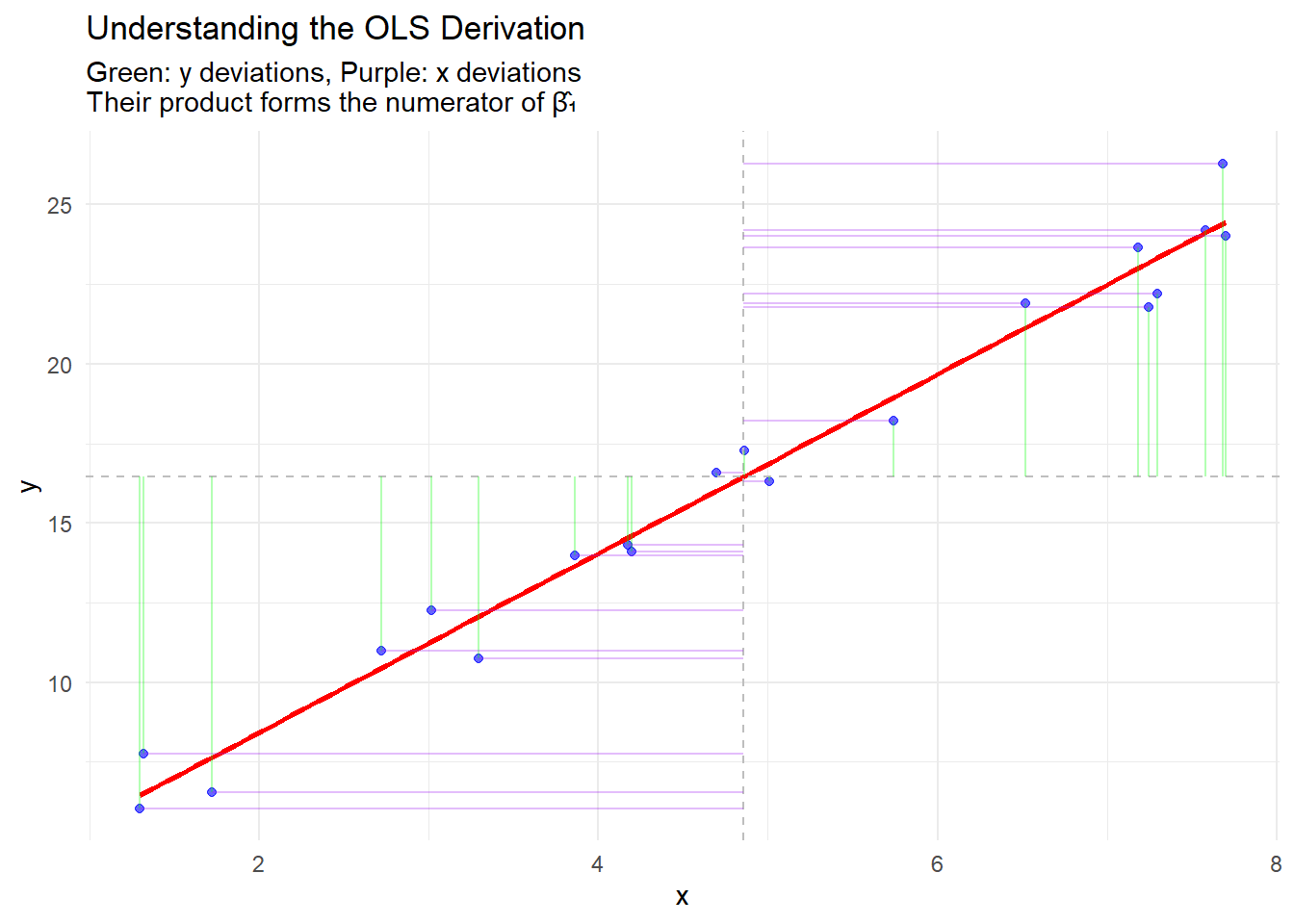

9.14 Step 3: Calculate Products and Squares

Now calculate (X_i - \bar{X})(Y_i - \bar{Y}) and (X_i - \bar{X})^2:

Student

(X_i - \bar{X})(Y_i - \bar{Y})

(X_i - \bar{X})^2

A

(-2.5)(-14.67) = 36.68

(-2.5)² = 6.25

B

(-1.5)(-9.67) = 14.51

(-1.5)² = 2.25

C

(-0.5)(-4.67) = 2.34

(-0.5)² = 0.25

D

(0.5)(5.33) = 2.67

(0.5)² = 0.25

E

(1.5)(8.33) = 12.50

(1.5)² = 2.25

F

(2.5)(15.33) = 38.33

(2.5)² = 6.25

Sum

107.03

17.50

9.15 Step 4: Calculate the Slope (\hat{\beta}_1)

Using the OLS formula: \hat{\beta}_1 = \frac{\sum(X_i - \bar{X})(Y_i - \bar{Y})}{\sum(X_i - \bar{X})^2} = \frac{107.03}{17.50} = 6.12

Interpretation: Each additional hour of study is associated with a 6.12-point increase in exam score.

9.16 Step 5: Calculate the Intercept (\hat{\beta}_0)

# Step 11: Calculate Effect Sizes# Raw effect size (just the slope)cat("\n--- Effect Size Calculations ---\n")

--- Effect Size Calculations ---

cat("Raw effect size (slope):", round(beta_1_manual, 2), "points per hour\n")

Raw effect size (slope): 6.11 points per hour

# Standard deviations for standardized effectsd_x <-sd(data$X) # Standard deviation of Xsd_y <-sd(data$Y) # Standard deviation of Ycat("\nStandard deviations:\n")

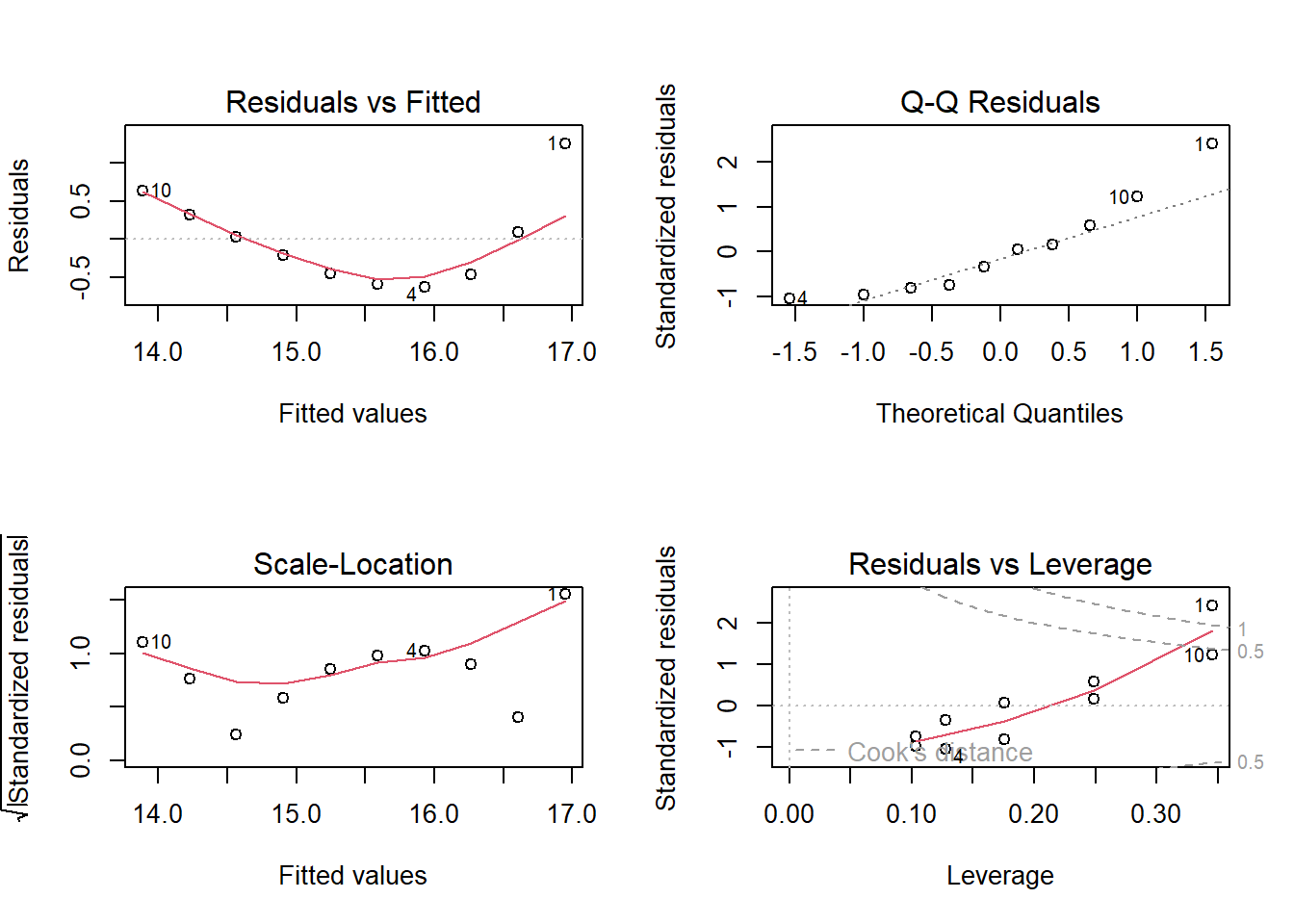

A plot showing the data points, regression line, and residuals

This verification confirms that our pen-and-paper calculations were correct!

9.26 The Linear Regression Model

Regression analysis provides a statistical framework for modeling relationships between a dependent variable and one or more independent variables. This methodology enables researchers to quantify relationships, test hypotheses, and make predictions based on observed data.

Simple Linear Regression

The simple linear regression model expresses the relationship between a dependent variable and a single independent variable:

Y_i = \beta_0 + \beta_1 X_i + \varepsilon_i

Where: - Y_i represents the dependent variable for observation i - X_i represents the independent variable for observation i - \beta_0 is the intercept parameter - \beta_1 is the slope parameter - \varepsilon_i is the error term for observation i

Multiple Linear Regression

The multiple linear regression model extends this framework to incorporate k independent variables:

This formulation allows for the simultaneous analysis of multiple predictors and their respective contributions to the dependent variable.

Ordinary Least Squares Estimation

Defining the Optimization Criterion

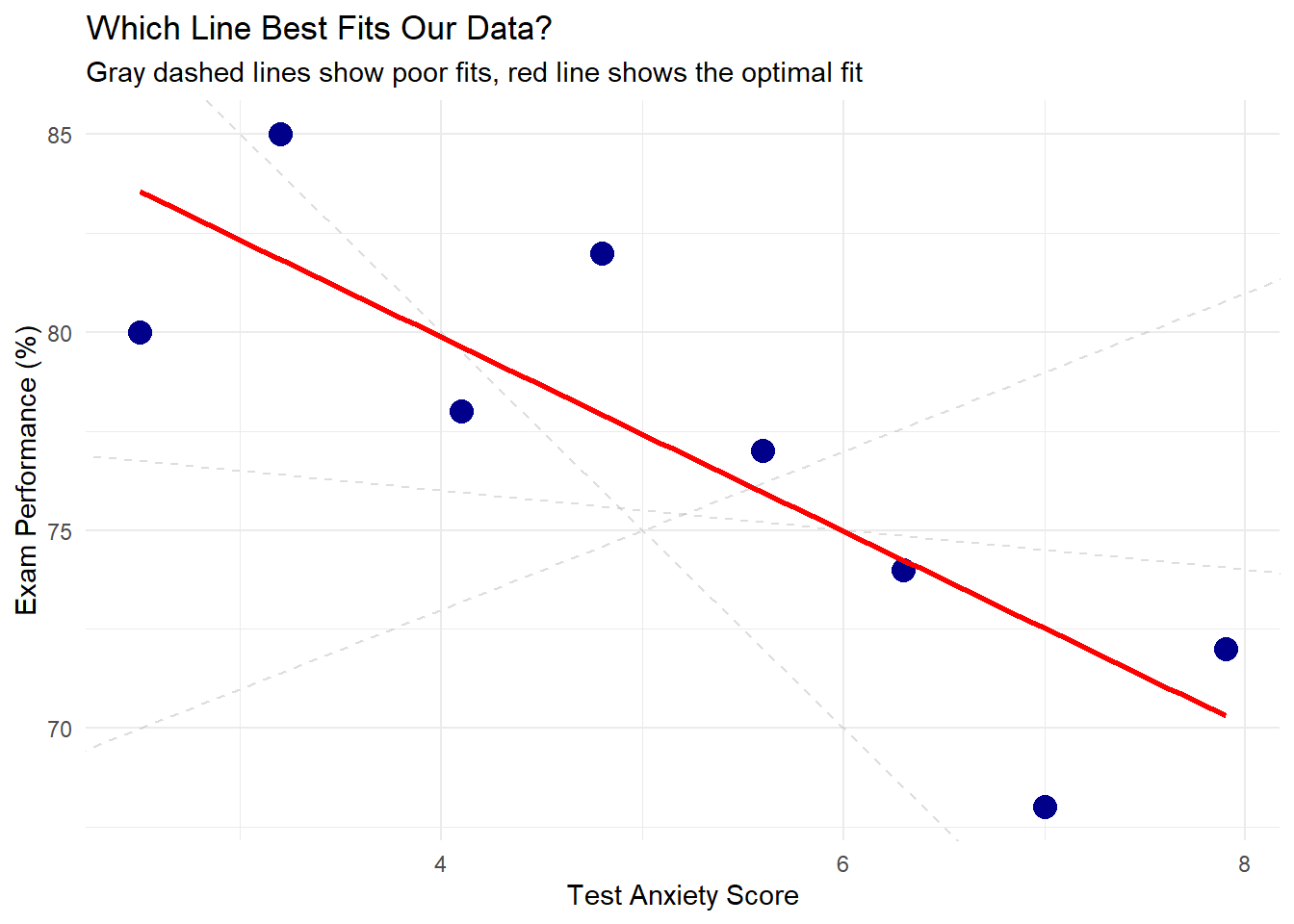

The estimation of regression parameters requires a criterion for determining the “best” fit. Consider three potential approaches for defining the optimal line through a set of data points:

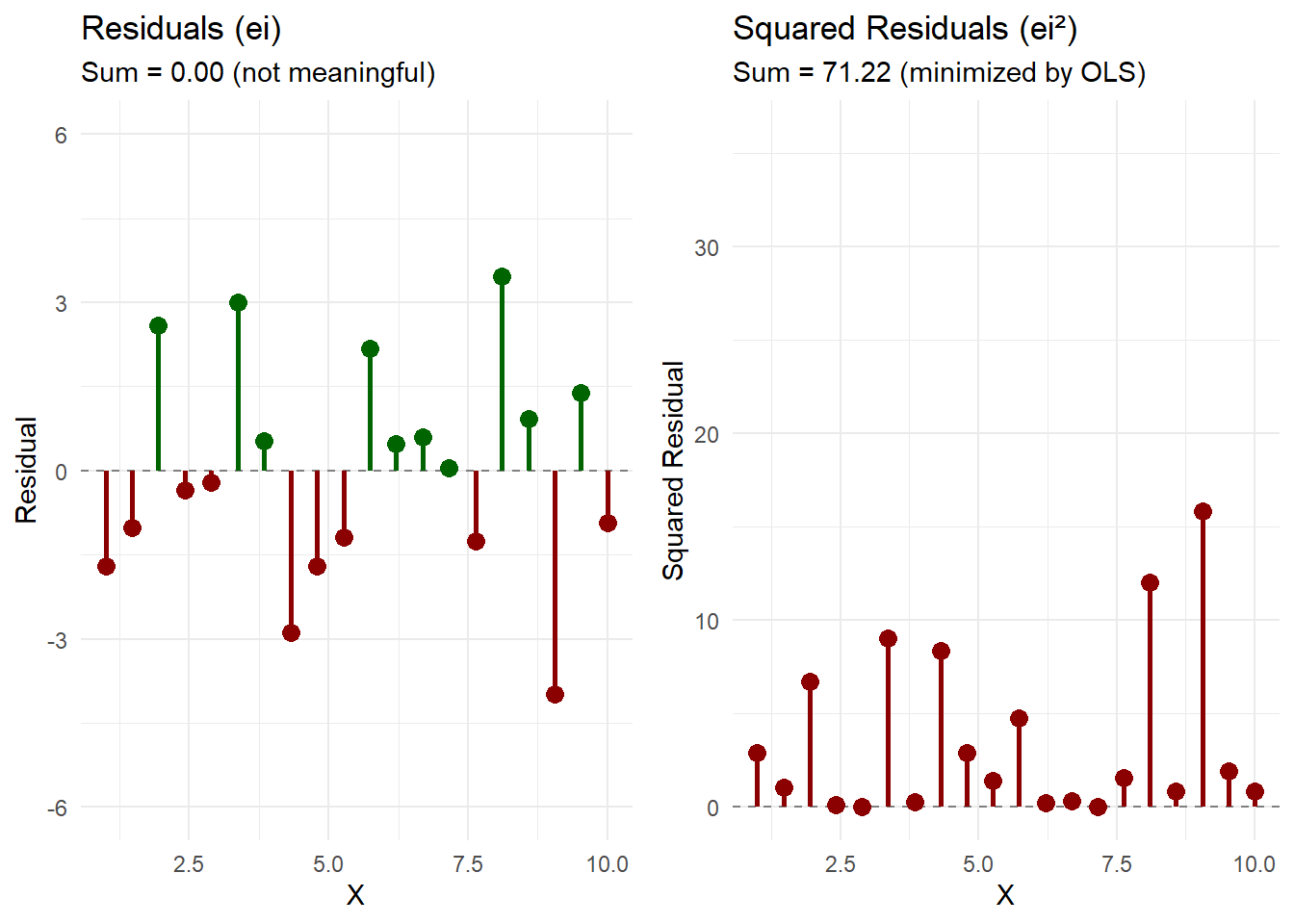

This approach is fundamentally flawed. For any line passing through the data, we can always find another line where positive and negative residuals sum to zero. In fact, infinitely many lines satisfy \sum e_i = 0. This criterion fails to uniquely identify an optimal solution. Moreover, a horizontal line through the mean of Y would achieve zero sum of residuals while ignoring the relationship with X entirely.

Approach 2: Minimizing the Sum of Absolute Residuals

This criterion, known as Least Absolute Deviations (LAD), addresses the cancellation problem by taking absolute values. It produces estimates that are more robust to outliers than OLS. However, this approach presents significant challenges:

The absolute value function is not differentiable at zero, complicating analytical solutions

Multiple solutions may exist (the objective function may have multiple minima)

No closed-form solution exists; iterative numerical methods are required

Statistical inference is more complex, lacking the elegant properties of OLS estimators

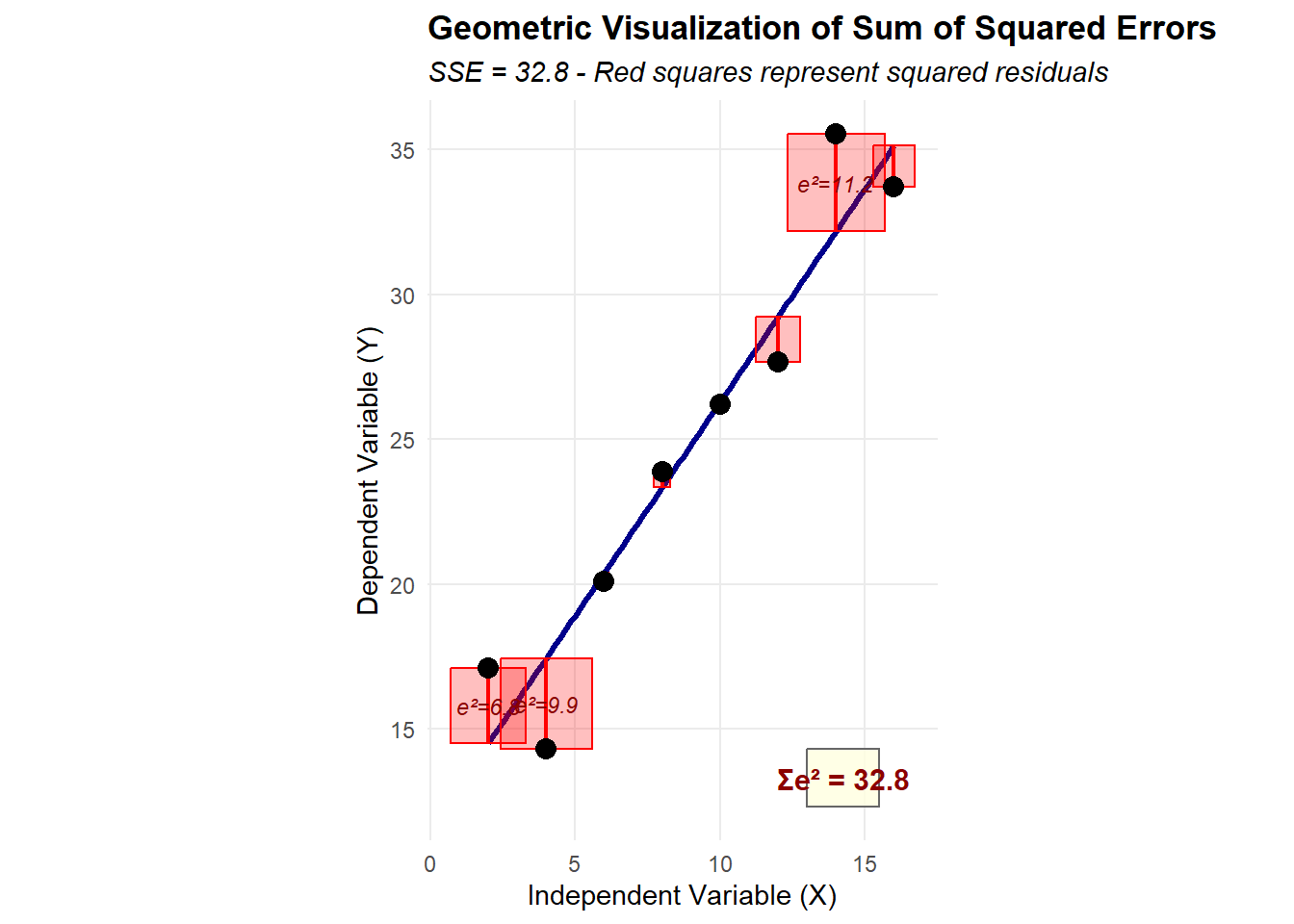

Approach 3: Minimizing the Sum of Squared Residuals

Taking partial derivatives with respect to \beta_0 and \beta_1 and setting them equal to zero yields the normal equations. Solving this system produces:

The OLS procedure guarantees several important properties:

Zero sum of residuals: \sum_{i=1}^{n} e_i = 0

Orthogonality of residuals and predictors: \sum_{i=1}^{n} X_i e_i = 0

The fitted regression line passes through the point(\bar{X}, \bar{Y})

Zero covariance between fitted values and residuals: \sum_{i=1}^{n} \hat{Y}_i e_i = 0

Classical Linear Model Assumptions

Core Assumptions

For OLS estimators to possess desirable statistical properties, the following assumptions must hold:

Assumption 1: Linearity in Parameters

The relationship between the dependent and independent variables is linear in the parameters: Y_i = \beta_0 + \beta_1 X_{1i} + ... + \beta_k X_{ki} + \varepsilon_i

Assumption 2: Strict Exogeneity

The error term has zero conditional expectation given all values of the independent variables: E[\varepsilon_i | X] = 0

This assumption implies that the independent variables contain no information about the mean of the error term. It is stronger than contemporaneous exogeneity and rules out feedback from past errors to current regressors. This assumption is critical for unbiased estimation and is often violated in time series contexts with lagged dependent variables or in the presence of omitted variables.

This assumption is particularly important for our discussion of spurious correlations. Violations of the exogeneity assumption lead to endogeneity problems, which we will discuss later.

Assumption 3: No Perfect Multicollinearity

In multiple regression, no independent variable can be expressed as a perfect linear combination of other independent variables. The matrix X'X must be invertible.

Assumption 4: Homoscedasticity

The variance of the error term is constant across all observations: Var(\varepsilon_i | X) = \sigma^2

This assumption ensures that the precision of the regression does not vary systematically with the level of the independent variables.

Assumption 5: No Autocorrelation

The error terms are uncorrelated with each other: Cov(\varepsilon_i, \varepsilon_j | X) = 0 \text{ for } i \neq j

Assumption 6: Normality of Errors (for inference)

The error terms follow a normal distribution: \varepsilon_i \sim N(0, \sigma^2)

This assumption is not required for the unbiasedness or consistency of OLS estimators but is necessary for exact finite-sample inference.

Gauss-Markov Theorem

Under Assumptions 1-5, the OLS estimators are BLUE (Best Linear Unbiased Estimators):

Best: Minimum variance among the class of linear unbiased estimators

Linear: The estimators are linear functions of the dependent variable

Unbiased: E[\hat{\beta}] = \beta

Visualization of OLS Methodology

Geometric Interpretation

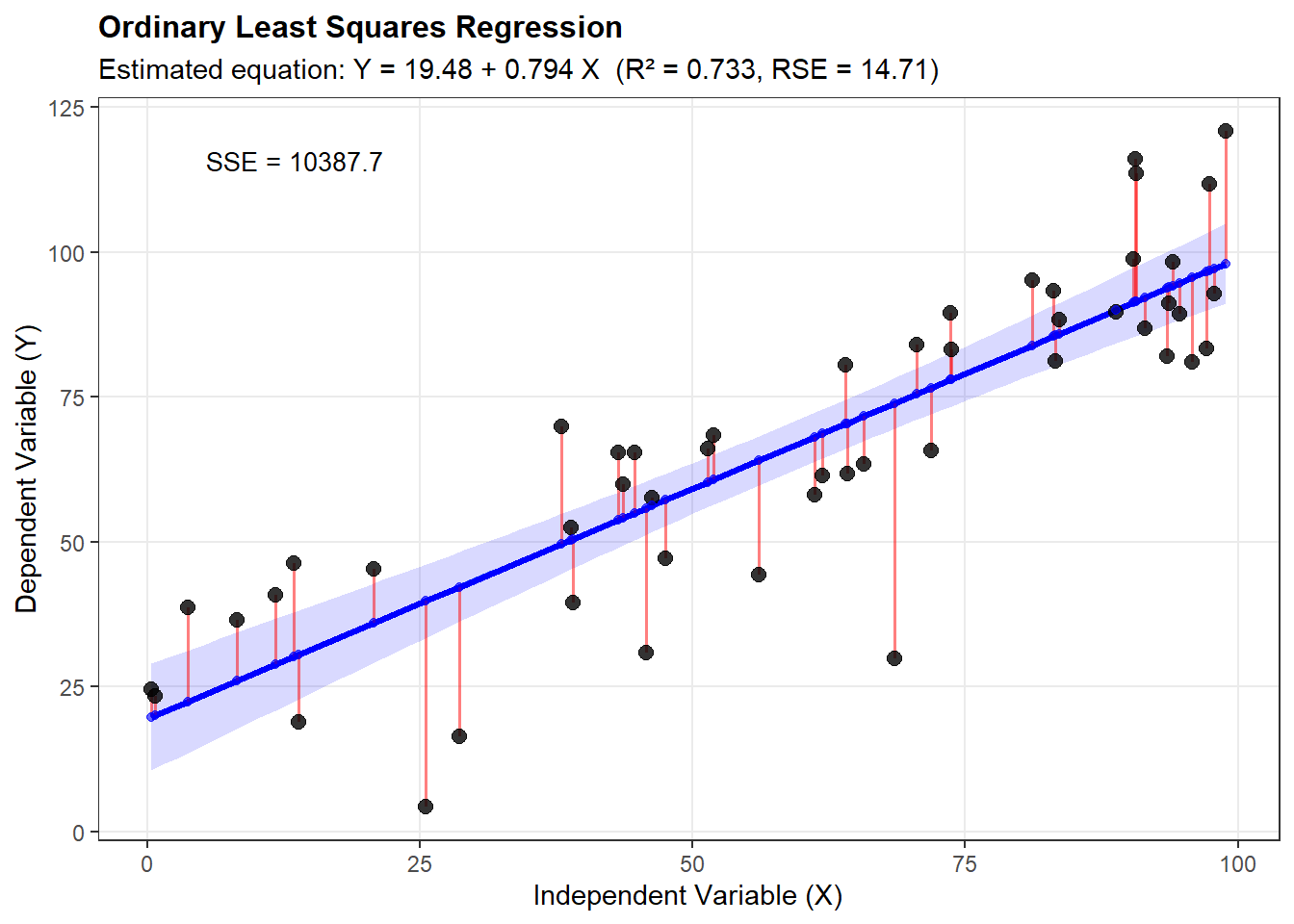

# Comprehensive visualization of OLS regressionlibrary(ggplot2)# Generate sample dataset.seed(42)n <-50x <-runif(n, 0, 100)epsilon <-rnorm(n, 0, 15)y <-20+0.8*x + epsilon# Create data framedata <-data.frame(x = x, y = y)# Fit regression modelmodel <-lm(y ~ x, data = data)data$fitted <-fitted(model)data$residuals <-residuals(model)# Create comprehensive plotggplot(data, aes(x = x, y = y)) +# Add confidence intervalgeom_smooth(method ="lm", se =TRUE, alpha =0.15, fill ="blue") +# Add regression linegeom_line(aes(y = fitted), color ="blue", linewidth =1.2) +# Add residual segmentsgeom_segment(aes(xend = x, yend = fitted), color ="red", alpha =0.5, linewidth =0.7) +# Add observed pointsgeom_point(size =2.5, alpha =0.8) +# Add fitted valuesgeom_point(aes(y = fitted), color ="blue", size =1.5, alpha =0.6) +# Annotationstheme_bw() +theme(panel.grid.minor =element_blank(),axis.title =element_text(size =11),plot.title =element_text(size =12, face ="bold") ) +labs(title ="Ordinary Least Squares Regression",subtitle =sprintf("Estimated equation: Y = %.2f + %.3f X (R² = %.3f, RSE = %.2f)",coef(model)[1], coef(model)[2], summary(model)$r.squared, summary(model)$sigma),x ="Independent Variable (X)",y ="Dependent Variable (Y)" ) +annotate("text", x =min(x) +5, y =max(y) -5,label =sprintf("SSE = %.1f", sum(residuals(model)^2)),hjust =0, size =3.5)

Ordinary Least Squares regression remains a fundamental tool in statistical analysis. The method’s mathematical elegance, combined with its optimal properties under the classical assumptions, explains its widespread application. However, practitioners must carefully verify assumptions and consider alternatives when these conditions are not met. Understanding both the theoretical foundations and practical limitations of OLS is essential for proper statistical inference and prediction.

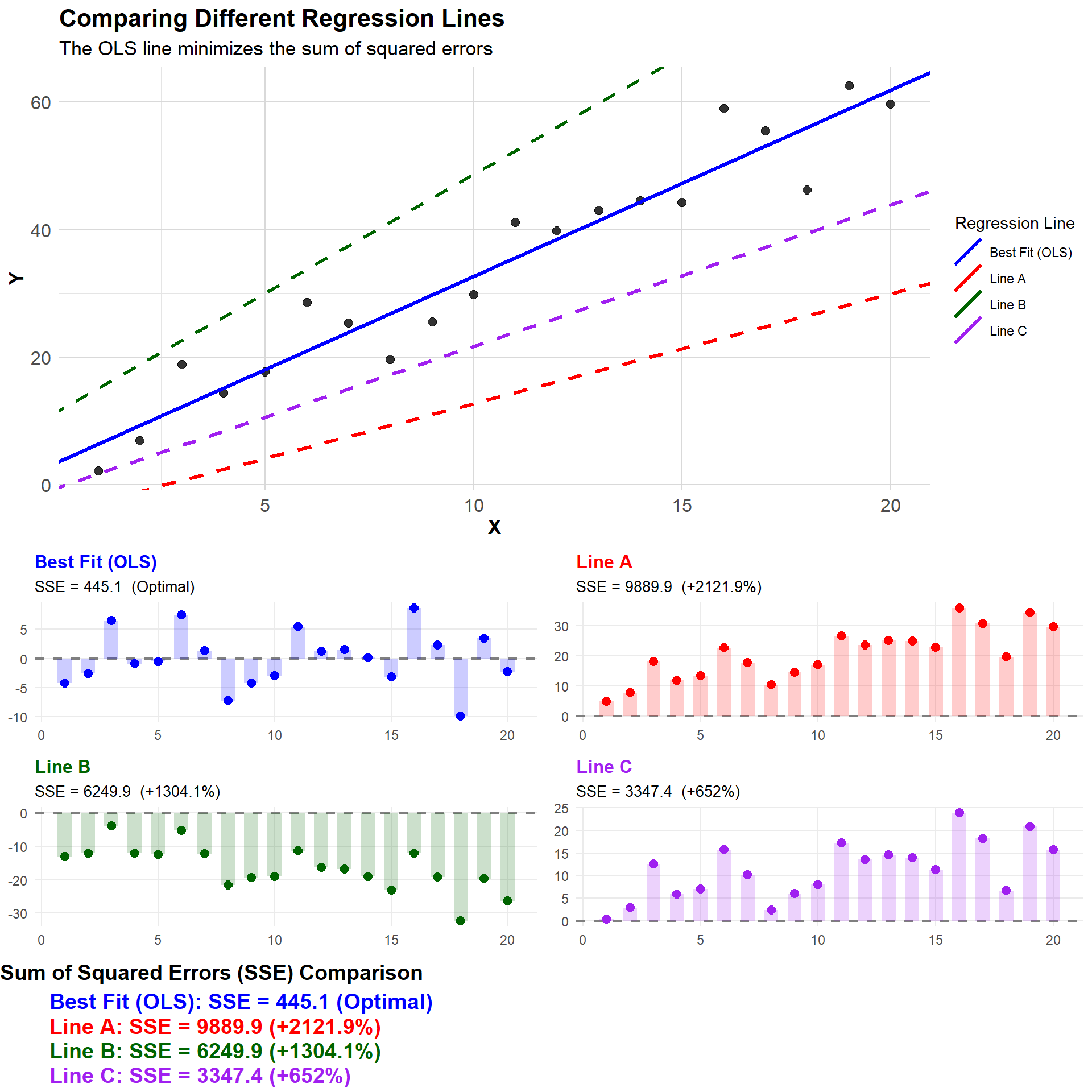

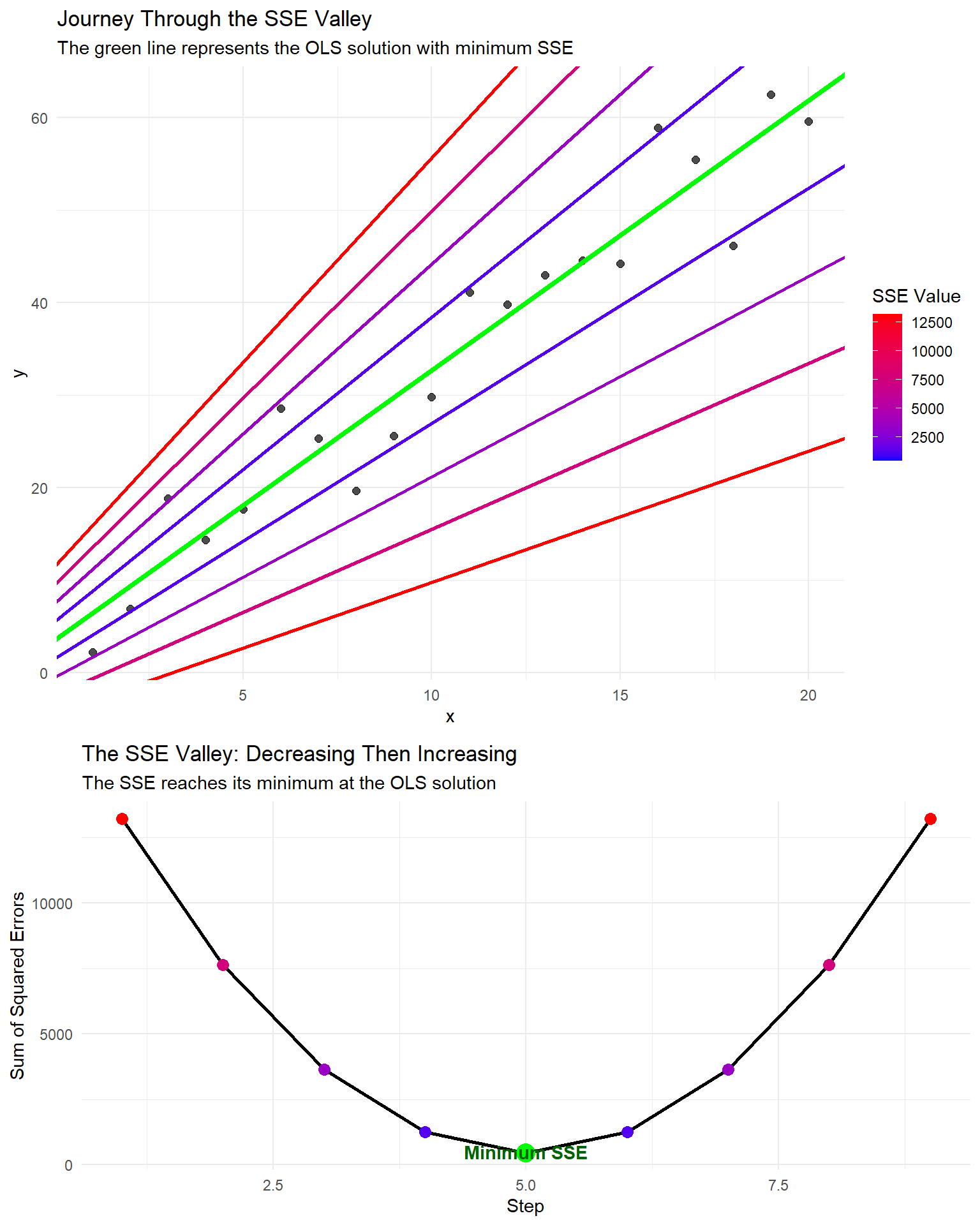

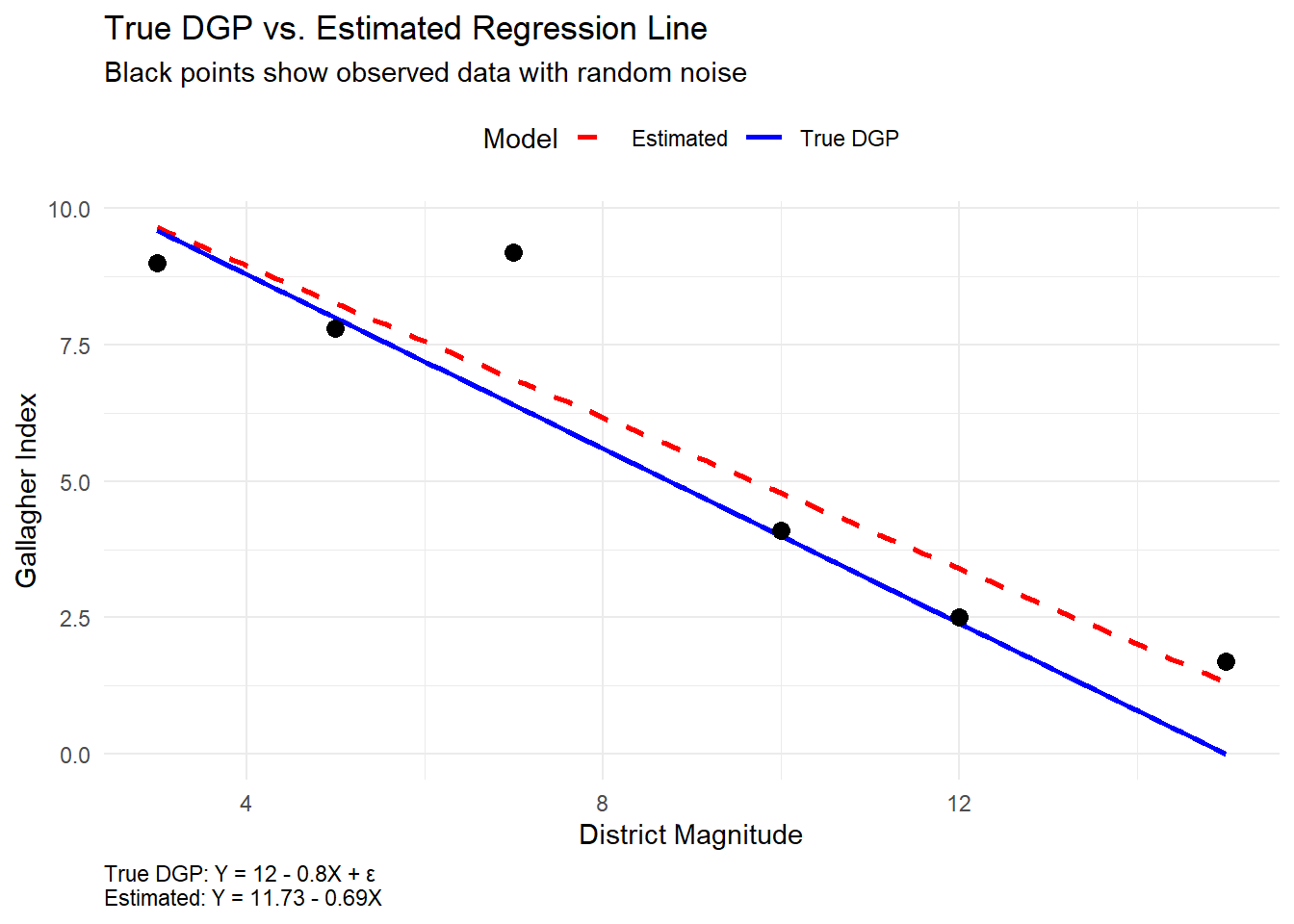

Visualizing OLS Through Different Regression Lines

A simple but effective way to visualize the concept of “best fit” is to compare multiple lines and their resulting SSE values:

# Load required librarieslibrary(ggplot2)library(gridExtra)# Create sample dataset.seed(123)x <-1:20y <-2+3*x +rnorm(20, 0, 5)data <-data.frame(x = x, y = y)# Fit regression modelmodel <-lm(y ~ x, data = data)coef <-coefficients(model)# Define different lines: optimal and sub-optimal with clearer differenceslines <-data.frame(label =c("Best Fit (OLS)", "Line A", "Line B", "Line C"),intercept =c(coef[1], coef[1] -8, coef[1] +8, coef[1] -4),slope =c(coef[2], coef[2] -1.2, coef[2] +0.8, coef[2] -0.7))# Calculate SSE for each linelines$sse <-sapply(1:nrow(lines), function(i) { predicted <- lines$intercept[i] + lines$slope[i] * xsum((y - predicted)^2)})# Add percentage increase over optimal SSElines$pct_increase <-round((lines$sse / lines$sse[1] -1) *100, 1)lines$pct_text <-ifelse(lines$label =="Best Fit (OLS)", "Optimal", paste0("+", lines$pct_increase, "%"))# Assign distinct colors for better visibilityline_colors <-c("Best Fit (OLS)"="blue", "Line A"="red", "Line B"="darkgreen", "Line C"="purple")# Create data for mini residual plotsmini_data <-data.frame()for(i in1:nrow(lines)) { line_data <-data.frame(x = x,y = y,predicted = lines$intercept[i] + lines$slope[i] * x,residuals = y - (lines$intercept[i] + lines$slope[i] * x),line = lines$label[i] ) mini_data <-rbind(mini_data, line_data)}# Create main comparison plot with improved visibilityp1 <-ggplot(data, aes(x = x, y = y)) +# Add background grid for referencetheme_minimal() +theme(panel.grid.minor =element_line(color ="gray90"),panel.grid.major =element_line(color ="gray85"),plot.title =element_text(size =16, face ="bold"),plot.subtitle =element_text(size =13),axis.title =element_text(size =13, face ="bold"),axis.text =element_text(size =12) ) +# Add data pointsgeom_point(size =2.5, alpha =0.8) +# Add lines with improved visibilitygeom_abline(data = lines, aes(intercept = intercept, slope = slope, color = label, linetype = label =="Best Fit (OLS)"),size =1.2) +# Use custom colorsscale_color_manual(values = line_colors) +scale_linetype_manual(values =c("TRUE"="solid", "FALSE"="dashed"), guide ="none") +# Better legendslabs(title ="Comparing Different Regression Lines",subtitle ="The OLS line minimizes the sum of squared errors",x ="X", y ="Y",color ="Regression Line") +guides(color =guide_legend(override.aes =list(size =2)))

Warning: Using `size` aesthetic for lines was deprecated in ggplot2 3.4.0.

ℹ Please use `linewidth` instead.

# Create mini residual plots with improved visibilityp_mini <-list()for(i in1:nrow(lines)) { line_data <-subset(mini_data, line == lines$label[i]) p_mini[[i]] <-ggplot(line_data, aes(x = x, y = residuals)) +# Add reference linegeom_hline(yintercept =0, linetype ="dashed", size =0.8, color ="gray50") +# Add residual points with line colorgeom_point(color = line_colors[lines$label[i]], size =2.5) +# Add squares to represent squared errorsgeom_rect(aes(xmin = x -0.3, xmax = x +0.3,ymin =0, ymax = residuals),fill = line_colors[lines$label[i]], alpha =0.2) +# Improved titleslabs(title = lines$label[i],subtitle =paste("SSE =", round(lines$sse[i], 1), ifelse(i ==1, " (Optimal)", paste0(" (+", lines$pct_increase[i], "%)"))),x =NULL, y =NULL) +theme_minimal() +theme(plot.title =element_text(size =12, face ="bold", color = line_colors[lines$label[i]]),plot.subtitle =element_text(size =10),panel.grid.minor =element_blank() )}# Create SSE comparison table with better visibilitysse_df <-data.frame(x =rep(1, nrow(lines)),y =nrow(lines):1,label =paste0(lines$label, ": SSE = ", round(lines$sse, 1), " (", lines$pct_text, ")"),color = line_colors[lines$label])sse_table <-ggplot(sse_df, aes(x = x, y = y, label = label, color = color)) +geom_text(hjust =0, size =5, fontface ="bold") +scale_color_identity() +theme_void() +xlim(1, 10) +ylim(0.5, nrow(lines) +0.5) +labs(title ="Sum of Squared Errors (SSE) Comparison") +theme(plot.title =element_text(hjust =0, face ="bold", size =14))# Arrange the plots with better spacinggrid.arrange( p1, arrangeGrob(p_mini[[1]], p_mini[[2]], p_mini[[3]], p_mini[[4]], ncol =2, padding =unit(1, "cm")), sse_table, ncol =1, heights =c(4, 3, 1))

Comparing different regression lines

Key Learning Points

The Sum of Squared Errors (SSE) is what Ordinary Least Squares (OLS) regression minimizes

Each residual contributes its squared value to the total SSE

The OLS line has a lower SSE than any other possible line

Large residuals contribute disproportionately to the SSE due to the squaring operation

This is why outliers can have such a strong influence on regression lines

Step-by-Step SSE Minimization

To illustrate the process of finding the minimum SSE, we can create a sequence that passes through the optimal point, showing how the SSE first decreases to a minimum and then increases again:

# Create sample dataset.seed(123)x <-1:20y <-2+3*x +rnorm(20, 0, 5)data <-data.frame(x = x, y = y)# Fit regression modelmodel <-lm(y ~ x, data = data)coef <-coefficients(model)# Create a sequence of steps that passes through the optimal OLS linesteps <-9# Use odd number to have a middle point at the optimumstep_seq <-data.frame(step =1:steps,intercept =seq(coef[1] -8, coef[1] +8, length.out = steps),slope =seq(coef[2] -1.5, coef[2] +1.5, length.out = steps))# Mark the middle step (optimal OLS solution)optimal_step <-ceiling(steps/2)# Calculate SSE for each stepstep_seq$sse <-sapply(1:nrow(step_seq), function(i) { predicted <- step_seq$intercept[i] + step_seq$slope[i] * xsum((y - predicted)^2)})# Create a "journey through the SSE valley" plotp2 <-ggplot(data, aes(x = x, y = y)) +geom_point(size =2, alpha =0.7) +geom_abline(data = step_seq, aes(intercept = intercept, slope = slope, color = sse, group = step),size =1) +# Highlight the optimal linegeom_abline(intercept = step_seq$intercept[optimal_step], slope = step_seq$slope[optimal_step],color ="green", size =1.5) +scale_color_gradient(low ="blue", high ="red") +labs(title ="Journey Through the SSE Valley",subtitle ="The green line represents the OLS solution with minimum SSE",color ="SSE Value") +theme_minimal()# Create an SSE valley plotp3 <-ggplot(step_seq, aes(x = step, y = sse)) +geom_line(size =1) +geom_point(size =3, aes(color = sse)) +scale_color_gradient(low ="blue", high ="red") +# Highlight the optimal pointgeom_point(data = step_seq[optimal_step, ], aes(x = step, y = sse), size =5, color ="green") +# Add annotationannotate("text", x = optimal_step, y = step_seq$sse[optimal_step] *1.1, label ="Minimum SSE", color ="darkgreen", fontface ="bold") +labs(title ="The SSE Valley: Decreasing Then Increasing",subtitle ="The SSE reaches its minimum at the OLS solution",x ="Step",y ="Sum of Squared Errors") +theme_minimal() +theme(legend.position ="none")# Display both plotsgrid.arrange(p2, p3, ncol =1, heights =c(3, 2))

SSE minimization visualization

In R, the lm() function fits linear regression models:

model <-lm(y ~ x, data = data_frame)

Model Interpretation: A Beginner’s Guide

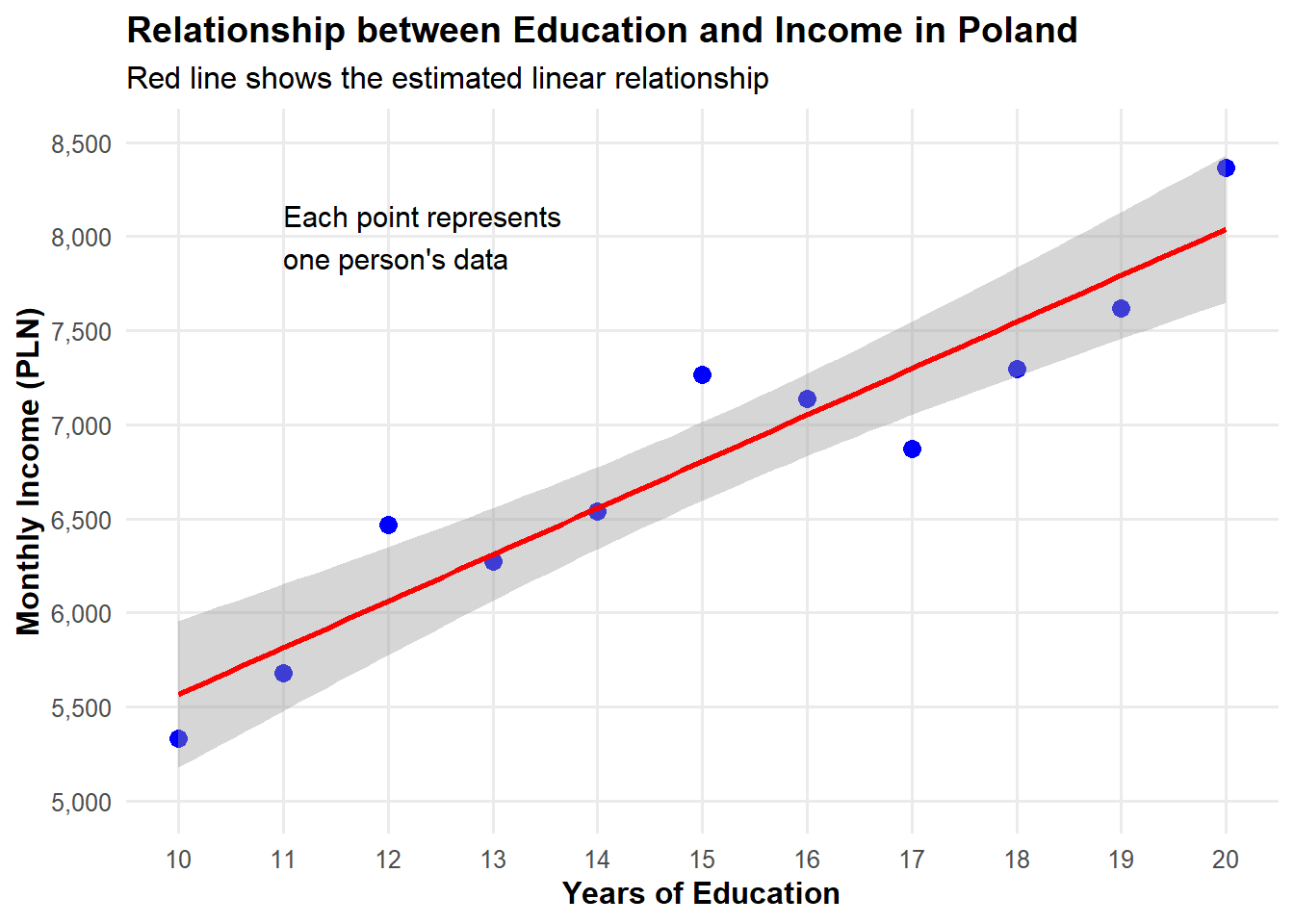

Let’s create a simple dataset to understand regression output better. Imagine we’re studying how years of education affect annual income:

# Create a simple dataset - this is our Data Generating Process (DGP)set.seed(123) # For reproducibilityeducation_years <-10:20# Education from 10 to 20 yearsn <-length(education_years)# True parameters in our model - using more realistic values for Polandtrue_intercept <-3000# Base monthly income with no education (in PLN)true_slope <-250# Each year of education increases monthly income by 250 PLN# Generate monthly incomes with some random noiseincome <- true_intercept + true_slope * education_years +rnorm(n, mean=0, sd=300)# Create our dataseteducation_income <-data.frame(education = education_years,income = income)# Let's visualize our datalibrary(ggplot2)ggplot(education_income, aes(x = education, y = income)) +geom_point(size =3, color ="blue") +geom_smooth(method ="lm", color ="red", se =TRUE) +scale_y_continuous(limits =c(5000, 8500), breaks =seq(5000, 8500, by =500),labels = scales::comma) +scale_x_continuous(breaks =10:20) +labs(title ="Relationship between Education and Income in Poland",x ="Years of Education",y ="Monthly Income (PLN)",subtitle ="Red line shows the estimated linear relationship" ) +theme_minimal(base_size =12) +theme(panel.grid.minor =element_blank(),plot.title =element_text(face ="bold"),axis.title =element_text(face ="bold") ) +annotate("text", x =11, y =8000, label ="Each point represents\none person's data", hjust =0, size =4)

`geom_smooth()` using formula = 'y ~ x'

Fitting the Model

Now let’s fit a linear regression model to this data:

# Fit a simple regression modeledu_income_model <-lm(income ~ education, data = education_income)# Display the resultsmodel_summary <-summary(edu_income_model)model_summary

Call:

lm(formula = income ~ education, data = education_income)

Residuals:

Min 1Q Median 3Q Max

-427.72 -206.04 -38.12 207.32 460.78

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3095.3 447.6 6.915 0.0000695 ***

education 247.2 29.2 8.467 0.0000140 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 306.3 on 9 degrees of freedom

Multiple R-squared: 0.8885, Adjusted R-squared: 0.8761

F-statistic: 71.69 on 1 and 9 DF, p-value: 0.00001403

Understanding the Regression Output Step by Step

Let’s break down what each part of this output means in simple terms:

1. The Formula

At the top, you see income ~ education, which means we’re predicting income based on education.

2. Residuals

These show how far our predictions are from the actual values. Ideally, they should be centered around zero.

3. Coefficients Table

Coefficient Estimates

Estimate

Std. Error

t value

Pr(>|t|)

(Intercept)

3095.27

447.63

6.91

0

education

247.23

29.20

8.47

0

Intercept (\beta_0):

Value: Approximately 3095

Interpretation: This is the predicted monthly income for someone with 0 years of education

Note: Sometimes the intercept isn’t meaningful in real-world terms, especially if x=0 is outside your data range

Education (\beta_1):

Value: Approximately 247

Interpretation: For each additional year of education, we expect monthly income to increase by this amount in PLN

This is our main coefficient of interest!

Standard Error:

Measures how precise our estimates are

Smaller standard errors mean more precise estimates

Think of it as “give or take how much” for our coefficients

t value:

This is the coefficient divided by its standard error

It tells us how many standard errors away from zero our coefficient is

Larger absolute t values (above 2) suggest the effect is statistically significant

p-value:

The probability of seeing our result (or something more extreme) if there was actually no relationship

Typically, p < 0.05 is considered statistically significant

For education, p = 0.000014, which is significant!

4. Model Fit Statistics

Model Fit Statistics

Statistic

Value

R-squared

0.888

Adjusted R-squared

0.876

F-statistic

71.686

p-value

0.000

R-squared:

Value: 0.888

Interpretation: 89% of the variation in income is explained by education

Higher is better, but be cautious of very high values (could indicate overfitting)

F-statistic:

Tests whether the model as a whole is statistically significant

A high F-statistic with a low p-value indicates a significant model

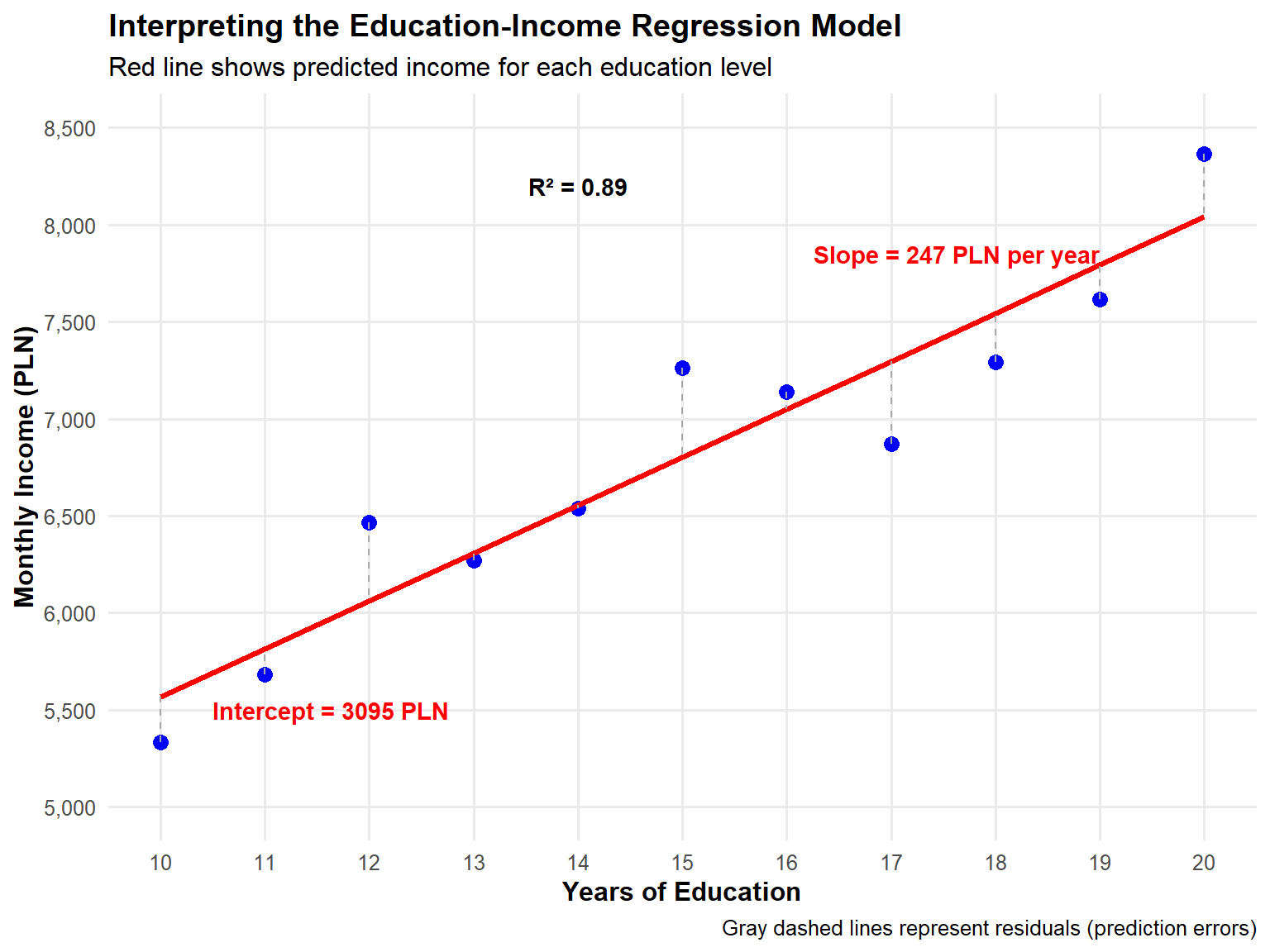

Visualizing the Model Results

Let’s visualize what our model actually tells us:

# Predicted valueseducation_income$predicted <-predict(edu_income_model)education_income$residuals <-residuals(edu_income_model)# Create a more informative plotggplot(education_income, aes(x = education, y = income)) +# Actual data pointsgeom_point(size =3, color ="blue") +# Regression linegeom_line(aes(y = predicted), color ="red", size =1.2) +# Residual linesgeom_segment(aes(xend = education, yend = predicted), color ="darkgray", linetype ="dashed") +# Set proper scalesscale_y_continuous(limits =c(5000, 8500), breaks =seq(5000, 8500, by =500),labels = scales::comma) +scale_x_continuous(breaks =10:20) +# Annotationsannotate("text", x =19, y =7850, label =paste("Slope =", round(coef(edu_income_model)[2]), "PLN per year"),color ="red", hjust =1, fontface ="bold") +annotate("text", x =10.5, y =5500, label =paste("Intercept =", round(coef(edu_income_model)[1]), "PLN"),color ="red", hjust =0, fontface ="bold") +annotate("text", x =14, y =8200, label =paste("R² =", round(model_summary$r.squared, 2)),color ="black", fontface ="bold") +# Labelslabs(title ="Interpreting the Education-Income Regression Model",subtitle ="Red line shows predicted income for each education level",x ="Years of Education",y ="Monthly Income (PLN)",caption ="Gray dashed lines represent residuals (prediction errors)" ) +theme_minimal(base_size =12) +theme(panel.grid.minor =element_blank(),plot.title =element_text(face ="bold"),axis.title =element_text(face ="bold") )

Real-World Interpretation

A person with 16 years of education (college graduate) would be predicted to earn about: \hat{Y} = 3095 + 247 \times 16 = 7051 \text{ PLN monthly}

The model suggests that each additional year of education is associated with a 247 PLN increase in monthly income.

Our model explains approximately 89% of the variation in income in our sample.

The relationship is statistically significant (p < 0.001), meaning it’s very unlikely to observe this relationship if education truly had no effect on income.

Important Cautions for Beginners

Correlation ≠ Causation: Our model shows association, not necessarily causation

Omitted Variables: Other factors might influence both education and income

Extrapolation: Be careful predicting outside the range of your data

Linear Relationship: We’ve assumed the relationship is linear, which may not always be true

9.27 Regression Analysis and Ordinary Least Squares (*)

Foundations of Regression Analysis

Regression analysis constitutes a fundamental statistical methodology for examining relationships between variables. At its core, regression provides a systematic framework for understanding how changes in one or more independent variables influence a dependent variable.

The primary objectives of regression analysis include: - Quantifying relationships between variables - Making predictions based on observed patterns - Testing hypotheses about variable associations - Understanding the proportion of variation explained by predictors

Deterministic versus Stochastic Models

Statistical modeling encompasses two fundamental approaches:

Deterministic models assume precise, invariant relationships between variables. Given specific inputs, these models yield identical outputs without variation. Consider the physics equation:

\text{Distance} = \text{Speed} \times \text{Time}

This relationship exhibits no randomness; identical inputs always produce identical outputs.

Stochastic models, in contrast, acknowledge inherent variability in real-world phenomena. Regression analysis employs stochastic modeling through the fundamental equation:

Y = f(X) + \epsilon

Where: - Y represents the outcome variable - f(X) captures the systematic relationship between predictors and outcome - \epsilon represents random variation inherent in the data

This formulation recognizes that real-world relationships contain both systematic patterns and random variation.

9.28 Simple Linear Regression Model

Model Specification

Simple linear regression models the relationship between a single predictor variable and an outcome variable through a linear equation:

Y_i = \beta_0 + \beta_1X_i + \epsilon_i

The model components represent: - Y_i: The dependent variable for observation i - X_i: The independent variable for observation i - \beta_0: The population intercept parameter - \beta_1: The population slope parameter - \epsilon_i: The random error term for observation i

Interpretation of Parameters

The parameters possess specific interpretations:

Intercept (\beta_0): The expected value of Y when X = 0. This represents the baseline level of the outcome variable.

Slope (\beta_1): The expected change in Y for a one-unit increase in X. This quantifies the strength and direction of the linear relationship.

Error term (\epsilon_i): Captures all factors affecting Y not explained by X, including measurement error, omitted variables, and inherent randomness.

Estimation versus True Parameters

The distinction between population parameters and sample estimates proves crucial:

Population parameters (\beta_0, \beta_1) represent true, unknown values

Sample estimates (\hat{\beta}_0, \hat{\beta}_1) represent our best approximations based on available data

The hat notation (^) consistently denotes estimated values

The fitted regression equation becomes:

\hat{Y}_i = \hat{\beta}_0 + \hat{\beta}_1X_i

9.29 The Ordinary Least Squares Method

The Fundamental Challenge

Given a dataset with observations (X_i, Y_i), we need a systematic method to determine the “best” values for \hat{\beta}_0 and \hat{\beta}_1. The challenge lies in defining what constitutes “best” and developing a practical method to find these values.

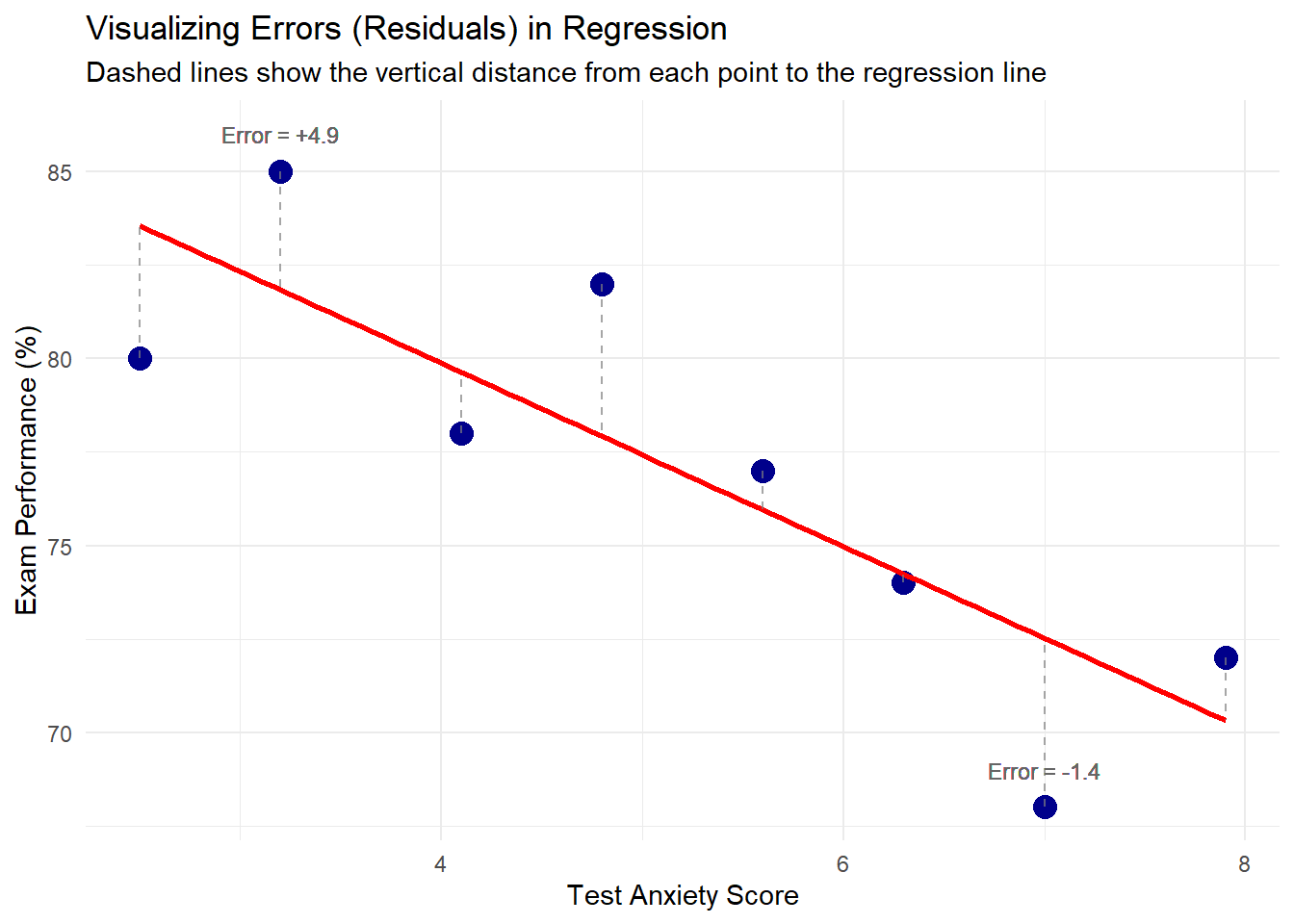

Consider that for any given line through the data, each observation will have a prediction error or residual:

These residuals represent how far our predictions deviate from actual values. A good fitting line should make these residuals as small as possible overall.

Why Minimize the Sum of Squared Residuals?

The Ordinary Least Squares method determines optimal parameter estimates by minimizing the sum of squared residuals. This choice requires justification, as we could conceivably minimize other quantities. The rationale for squaring residuals includes:

Mathematical tractability: Squaring creates a smooth, differentiable function that yields closed-form solutions through calculus. The derivatives of squared terms lead to linear equations that can be solved analytically.

Equal treatment of positive and negative errors: Simply summing raw residuals would allow positive and negative errors to cancel, potentially yielding a sum of zero even when predictions are poor. Squaring ensures all deviations contribute positively to the total error measure.

Penalization of large errors: Squaring gives progressively greater weight to larger errors. An error of 4 units contributes 16 to the sum, while an error of 2 units contributes only 4. This property encourages finding a line that avoids extreme prediction errors.

Statistical optimality: Under certain assumptions (including normally distributed errors), OLS estimators possess desirable statistical properties, including being the Best Linear Unbiased Estimators (BLUE) according to the Gauss-Markov theorem.

Connection to variance: The sum of squared deviations directly relates to variance, a fundamental measure of spread in statistics. Minimizing squared residuals thus minimizes the variance of prediction errors.

The OLS Optimization Problem

The OLS method formally seeks values of \hat{\beta}_0 and \hat{\beta}_1 that minimize:

This optimization problem can be solved using calculus by: 1. Taking partial derivatives with respect to \hat{\beta}_0 and \hat{\beta}_1 2. Setting these derivatives equal to zero 3. Solving the resulting system of equations

These formulas reveal that: - The slope estimate depends on the covariance between variables relative to the predictor’s variance - The intercept ensures the regression line passes through the point of means (\bar{X}, \bar{Y})

Properties of OLS Estimators

OLS estimators possess several desirable properties:

Unbiasedness: Under appropriate conditions, E[\hat{\beta}_j] = \beta_j

Efficiency: OLS provides minimum variance among linear unbiased estimators

Consistency: As sample size increases, estimates converge to true values

The regression line passes through the centroid: The point (\bar{X}, \bar{Y}) always lies on the fitted line

Extension to Multiple Regression

While this guide focuses on simple linear regression with one predictor, the OLS framework extends naturally to multiple regression with several predictors:

The same principle applies: we minimize the sum of squared residuals, though the mathematics involves matrix algebra rather than simple formulas. The fundamental logic—finding parameter values that minimize prediction errors—remains unchanged.

9.30 Understanding Variance Decomposition

The Baseline Model Concept

Before introducing predictors, consider the simplest possible model: predicting every observation using the overall mean \bar{Y}. This baseline model represents our best prediction in the absence of additional information.

The baseline model’s predictions: \hat{Y}_i^{\text{baseline}} = \bar{Y} \text{ for all } i

This model serves as a reference point for evaluating improvement gained through incorporating predictors. The baseline model essentially asks: “If we knew nothing about the relationship between X and Y, what would be our best constant prediction?”

Components of Total Variation

The total variation in the outcome variable decomposes into three fundamental components:

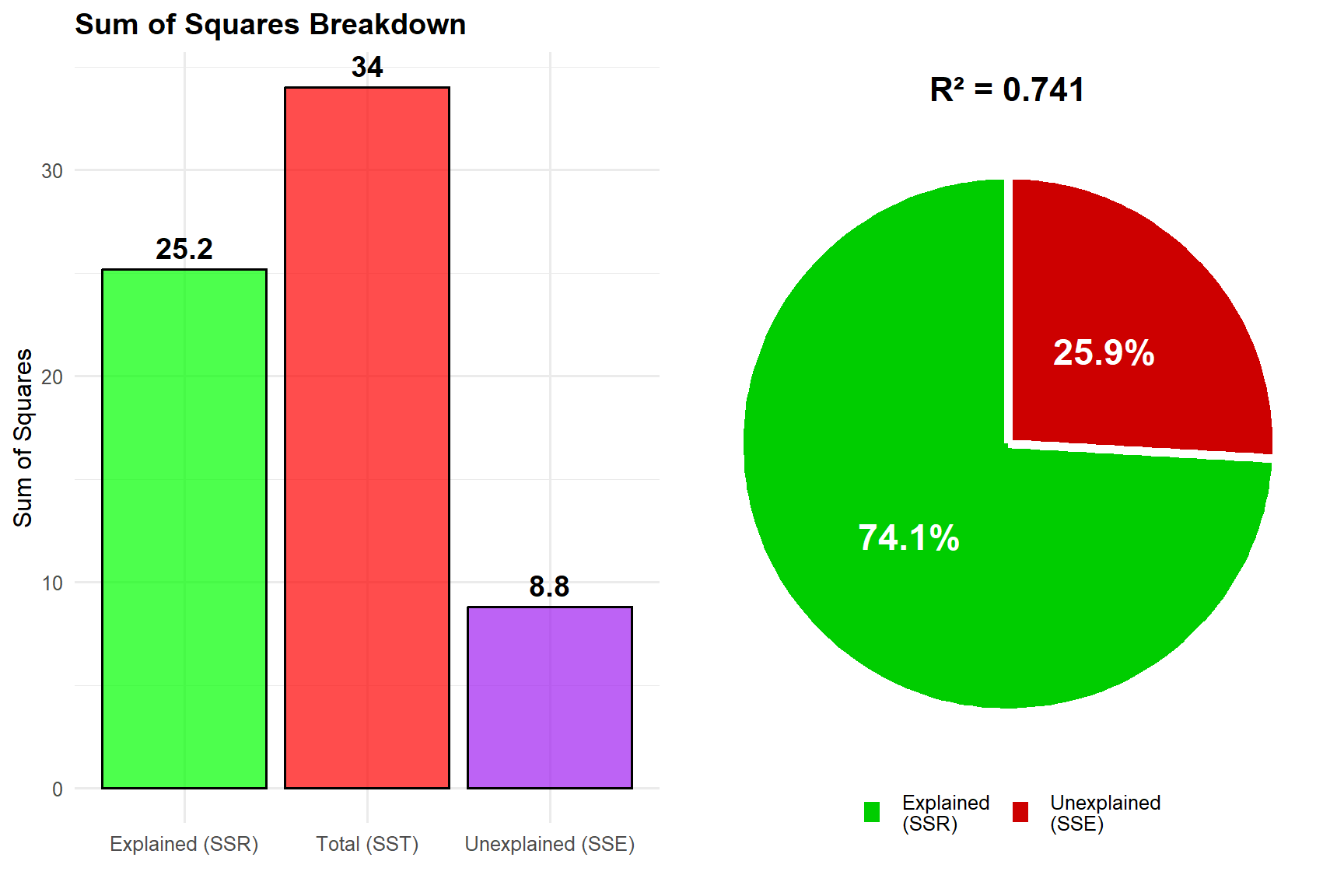

Total Sum of Squares (SST)

SST quantifies the total variation in the outcome variable relative to its mean:

\text{SST} = \sum_{i=1}^n (Y_i - \bar{Y})^2

Interpretation: SST represents the total variance that requires explanation. It measures the prediction error when using only the mean as our model—essentially the variance explained by the baseline (zero) model. This is the starting point: the total amount of variation we hope to explain by introducing predictors.

Regression Sum of Squares (SSR)

SSR measures the variation explained by the regression model:

\text{SSR} = \sum_{i=1}^n (\hat{Y}_i - \bar{Y})^2

Interpretation: SSR quantifies the improvement in prediction achieved by incorporating the predictor variable. It represents the reduction in prediction error relative to the baseline model—the portion of total variation that our regression line successfully captures.

Error Sum of Squares (SSE)

SSE captures the unexplained variation remaining after regression:

\text{SSE} = \sum_{i=1}^n (Y_i - \hat{Y}_i)^2

Interpretation: SSE represents the residual variation that the model cannot explain, reflecting the inherent randomness and effects of omitted variables. This is the variation that remains even after using our best-fitting line.

The Fundamental Decomposition Identity

These components relate through the fundamental equation:

\text{SST} = \text{SSR} + \text{SSE}

This identity demonstrates that: - Total variation equals the sum of explained and unexplained components - The regression model partitions total variation into systematic and random parts - Model improvement can be assessed by comparing SSR to SST

Conceptual Framework for Variance Decomposition

# Demonstration of Variance Decompositionlibrary(ggplot2)# Generate sample dataset.seed(42)n <-50x <-runif(n, 1, 10)y <-3+2*x +rnorm(n, 0, 2)data <-data.frame(x = x, y = y)# Fit modelmodel <-lm(y ~ x, data = data)y_mean <-mean(y)y_pred <-predict(model)# Calculate componentsSST <-sum((y - y_mean)^2)SSR <-sum((y_pred - y_mean)^2)SSE <-sum((y - y_pred)^2)# Display decompositioncat("Variance Decomposition\n")cat("======================\n")cat("Total SS (SST):", round(SST, 2), "- Total variation from mean\n")cat("Regression SS (SSR):", round(SSR, 2), "- Variation explained by model\n")cat("Error SS (SSE):", round(SSE, 2), "- Unexplained variation\n")cat("\nVerification: SST = SSR + SSE\n")cat(round(SST, 2), "=", round(SSR, 2), "+", round(SSE, 2), "\n")

9.31 The Coefficient of Determination (R²)

Definition and Calculation

The coefficient of determination, denoted R², quantifies the proportion of total variation explained by the regression model:

R² directly answers the question: “What proportion of the total variation in Y (relative to the baseline mean model) does our regression model explain?”

Interpretation Guidelines

R² values range from 0 to 1, with specific interpretations:

R² = 0: The model explains no variation beyond the baseline mean model. The regression line provides no improvement over simply using \bar{Y}.

R² = 0.25: The model explains 25% of total variation. Three-quarters of the variation remains unexplained.

R² = 0.75: The model explains 75% of total variation. This represents substantial explanatory power.

R² = 1.00: The model explains all variation (perfect fit). All data points fall exactly on the regression line.

Contextual Considerations

The interpretation of R² requires careful consideration of context:

Field-specific standards: Acceptable R² values vary dramatically across disciplines - Physical sciences often expect R² > 0.90 due to controlled conditions - Social sciences may consider R² = 0.30 meaningful given human complexity - Biological systems typically show intermediate values due to natural variation

Sample size effects: Small samples can artificially inflate R², leading to overly optimistic assessments of model fit.

Model complexity: In multiple regression, additional predictors mechanically increase R², even if they lack true explanatory power.

Practical significance: Statistical fit should align with substantive importance. A model with R² = 0.95 may be less useful than one with R² = 0.60 if the latter addresses more relevant questions.

Adjusted R² for Multiple Regression

When extending to multiple regression, adjusted R² accounts for the number of predictors:

cat("Explained by model (SSR):", round(SSR, 2), "\n")

Explained by model (SSR): 12578.3

cat("Unexplained (SSE):", round(SSE, 2), "\n")

Unexplained (SSE): 2301.84

cat("\nModel Performance:\n")

Model Performance:

cat("R-squared:", round(r_squared, 4), "\n")

R-squared: 0.8453

cat("Interpretation: The model explains", round(r_squared *100, 1), "% of the variation in exam scores\n")

Interpretation: The model explains 84.5 % of the variation in exam scores

cat("beyond what the mean alone could explain.\n")

beyond what the mean alone could explain.

Visualization of Key Concepts

# Create comprehensive visualizationlibrary(ggplot2)library(gridExtra)# Plot 1: Baseline model (mean only)p1 <-ggplot(education_data, aes(x = study_hours, y = exam_scores)) +geom_point(alpha =0.6) +geom_hline(yintercept = y_mean, color ="blue", size =1) +geom_segment(aes(xend = study_hours, yend = y_mean), alpha =0.3, color ="red") +labs(title ="Baseline Model: Predicting with Mean",subtitle =paste("Total variation (SST) =", round(SST, 1)),x ="Study Hours", y ="Exam Scores") +theme_minimal() +annotate("text", x =8, y = y_mean +1, label ="Mean of Y", color ="blue")# Plot 2: Regression modelp2 <-ggplot(education_data, aes(x = study_hours, y = exam_scores)) +geom_point(alpha =0.6) +geom_smooth(method ="lm", se =FALSE, color ="blue") +geom_segment(aes(xend = study_hours, yend = y_pred), alpha =0.3, color ="red") +labs(title ="Regression Model: Improved Predictions",subtitle =paste("Unexplained variation (SSE) =", round(SSE, 1), "| R² =", round(r_squared, 3)),x ="Study Hours", y ="Exam Scores") +theme_minimal() +annotate("text", x =8, y =max(y_pred) +1, label ="Regression Line", color ="blue")# Plot 3: Variance componentsvariance_data <-data.frame(Component =c("Total (SST)", "Explained (SSR)", "Unexplained (SSE)"),Value =c(SST, SSR, SSE),Type =c("Total", "Explained", "Unexplained"))p3 <-ggplot(variance_data, aes(x = Component, y = Value, fill = Type)) +geom_bar(stat ="identity") +scale_fill_manual(values =c("Total"="gray50", "Explained"="green4", "Unexplained"="red3")) +labs(title ="Variance Decomposition",y ="Sum of Squares") +theme_minimal() +theme(legend.position ="none")# Combine plotsgrid.arrange(p1, p2, p3, layout_matrix =rbind(c(1, 2), c(3, 3)))

`geom_smooth()` using formula = 'y ~ x'

9.33 Summary and Key Insights

Core Concepts Review

Regression analysis models relationships between variables using stochastic frameworks that acknowledge inherent variation. The simple linear regression model expresses this relationship as Y_i = \beta_0 + \beta_1X_i + \epsilon_i.

Ordinary Least Squares provides optimal parameter estimates by minimizing the sum of squared residuals. This choice of minimizing squared errors stems from mathematical tractability, equal treatment of positive and negative errors, appropriate penalization of large errors, and desirable statistical properties.

Variance decomposition partitions total variation into: - Total variation from the baseline mean model (SST) - Variation explained by the regression model (SSR)

- Unexplained residual variation (SSE)

The fundamental identity SST = SSR + SSE shows how regression improves upon the baseline model.

R² quantifies model performance as the proportion of total variation explained, providing a standardized measure of how much better the regression model performs compared to simply using the mean.

Critical Considerations

The baseline model (predicting with the mean) serves as the fundamental reference point. All regression improvement is measured relative to this simple model. SST represents the total variance requiring explanation when we start with no predictors.

Parameter estimates (\hat{\beta}_0, \hat{\beta}_1) represent sample-based approximations of unknown population values (\beta_0, \beta_1). The distinction between population parameters and sample estimates remains crucial for proper inference.

Model assessment requires considering both statistical fit (R²) and practical significance. A model with modest R² may still provide valuable insights, while high R² does not guarantee causation or practical utility.

Extensions and Applications

While this guide focuses on simple linear regression, the framework extends naturally to: - Multiple regression with several predictors - Polynomial regression for nonlinear relationships - Interaction terms to capture conditional effects - Categorical predictors through appropriate coding

The fundamental principles—minimizing prediction errors, decomposing variation, and assessing model fit—remain consistent across these extensions. The mathematical complexity increases, but the conceptual foundation established here continues to apply.

9.34 Key Assumptions of Linear Regression

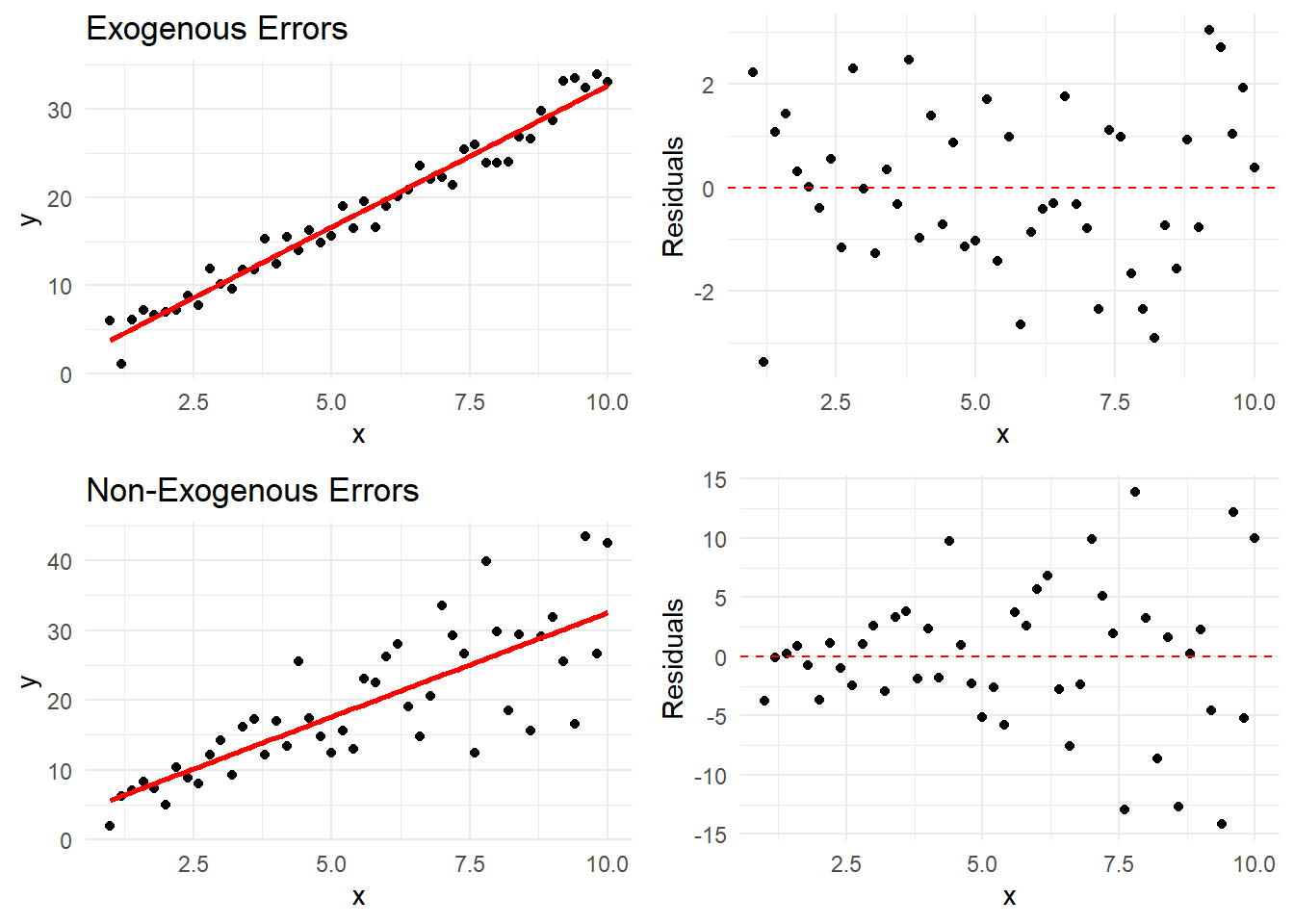

Strict Exogeneity: The Fundamental Assumption

The most crucial assumption in regression is strict exogeneity:

E[\varepsilon|X] = 0

This means:

The error term has zero mean conditional on X

X contains no information about the average error

There are no systematic patterns in how our predictions are wrong

Let’s visualize when this assumption holds and when it doesn’t:

# Generate dataset.seed(789)x <-seq(1, 10, by =0.2)# Case 1: Exogenous errorsy_exog <-2+3*x +rnorm(length(x), 0, 2)# Case 2: Non-exogenous errors (error variance increases with x)y_nonexog <-2+3*x +0.5*x*rnorm(length(x), 0, 2)# Create datasetsdata_exog <-data.frame(x = x,y = y_exog,type ="Exogenous Errors\n(Assumption Satisfied)")data_nonexog <-data.frame(x = x,y = y_nonexog,type ="Non-Exogenous Errors\n(Assumption Violated)")data_combined <-rbind(data_exog, data_nonexog)# Create plots with residualsplot_residuals <-function(data, title) { model <-lm(y ~ x, data = data) data$predicted <-predict(model) data$residuals <-residuals(model) p1 <-ggplot(data, aes(x = x, y = y)) +geom_point() +geom_smooth(method ="lm", se =FALSE, color ="red") +theme_minimal() +labs(title = title) p2 <-ggplot(data, aes(x = x, y = residuals)) +geom_point() +geom_hline(yintercept =0, linetype ="dashed", color ="red") +theme_minimal() +labs(y ="Residuals")list(p1, p2)}# Generate plotsplots_exog <-plot_residuals(data_exog, "Exogenous Errors")plots_nonexog <-plot_residuals(data_nonexog, "Non-Exogenous Errors")# Arrange plotsgridExtra::grid.arrange( plots_exog[[1]], plots_exog[[2]], plots_nonexog[[1]], plots_nonexog[[2]],ncol =2)

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

Figure 9.1: Exogeneity vs. Non-Exogeneity Examples

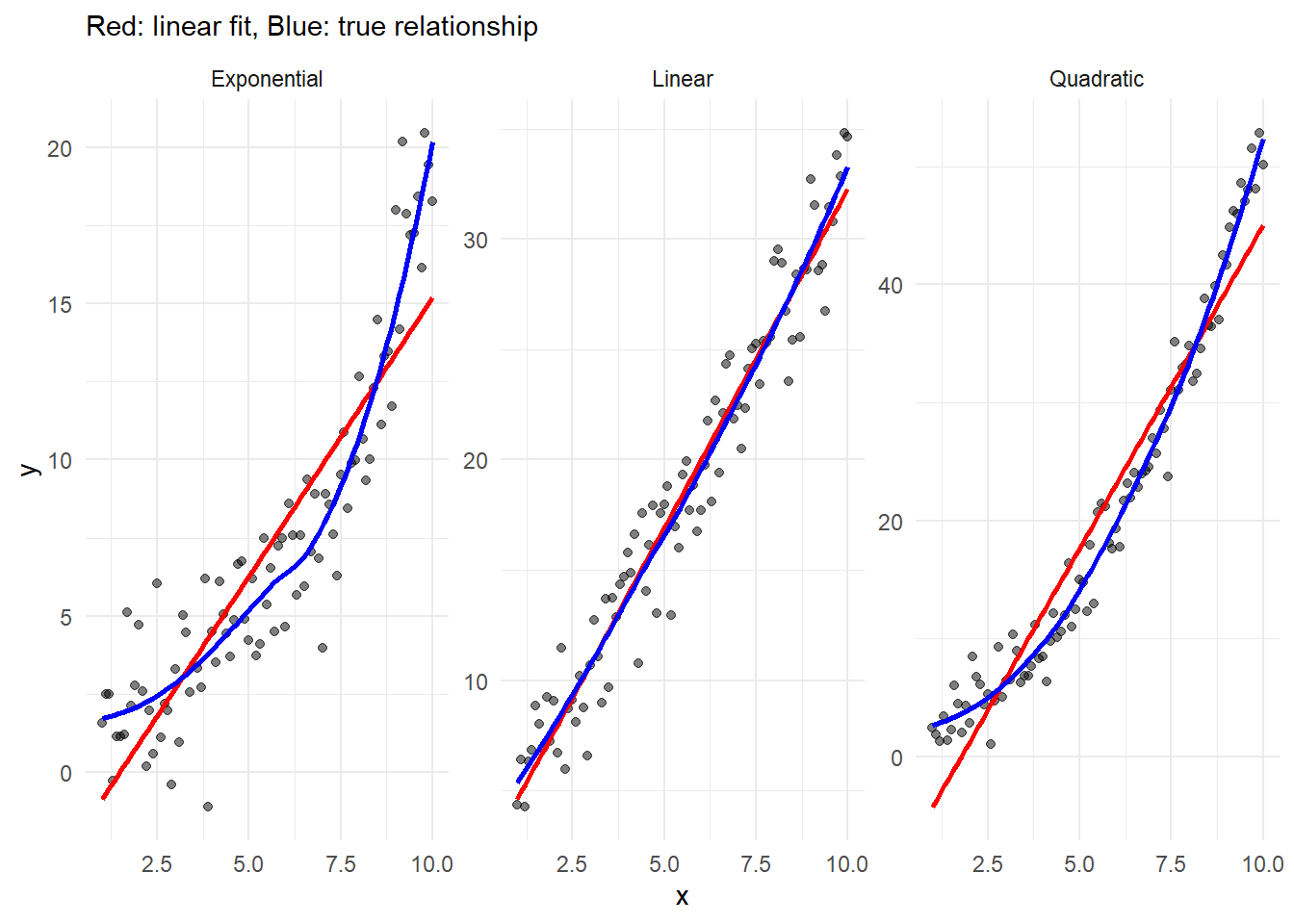

Linearity: The Form Assumption

The relationship between X and Y should be linear in parameters:

E[Y|X] = \beta_0 + \beta_1X

Note that this doesn’t mean X and Y must have a straight-line relationship - we can transform variables. Let’s see different types of relationships:

# Generate dataset.seed(101)x <-seq(1, 10, by =0.1)# Different relationshipsdata_relationships <-data.frame(x =rep(x, 3),y =c(# Linear2+3*x +rnorm(length(x), 0, 2),# Quadratic2+0.5*x^2+rnorm(length(x), 0, 2),# Exponentialexp(0.3*x) +rnorm(length(x), 0, 2) ),type =rep(c("Linear", "Quadratic", "Exponential"), each =length(x)))# Plotggplot(data_relationships, aes(x = x, y = y)) +geom_point(alpha =0.5) +geom_smooth(method ="lm", se =FALSE, color ="red") +geom_smooth(se =FALSE, color ="blue") +facet_wrap(~type, scales ="free_y") +theme_minimal() +labs(subtitle ="Red: linear fit, Blue: true relationship")

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using method = 'loess' and formula = 'y ~ x'

Figure 9.2: Linear and Nonlinear Relationships

Understanding Violations and Solutions

When linearity is violated:

Transform variables:

Log transformation: for exponential relationships

Square root: for moderate nonlinearity

Power transformations: for more complex relationships

# Original scale plotp1 <-ggplot(data_trans, aes(x = x, y = y)) +geom_point() +geom_smooth(method ="lm", se =FALSE, color ="red") +theme_minimal() +labs(title ="Original Scale")# Log scale plotp2 <-ggplot(data_trans, aes(x = x, y = log_y)) +geom_point() +geom_smooth(method ="lm", se =FALSE, color ="red") +theme_minimal() +labs(title ="Log-Transformed Y")gridExtra::grid.arrange(p1, p2, ncol =2)

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

Warning: Removed 1 row containing non-finite outside the scale range

(`stat_smooth()`).

Warning: Removed 1 row containing missing values or values outside the scale range

(`geom_point()`).

Figure 9.3: Effect of Variable Transformations

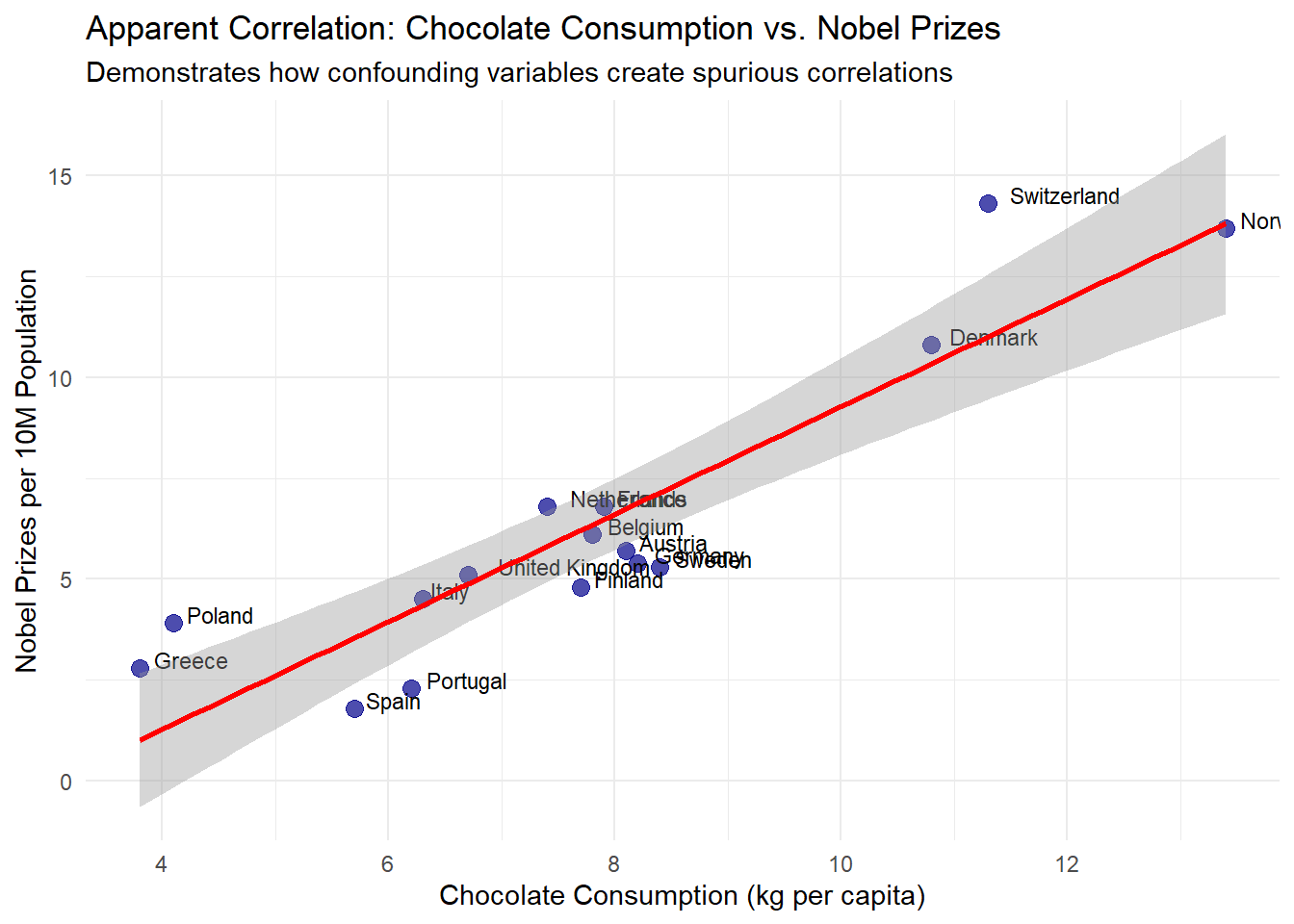

9.35 Spurious Correlation: Causes and Examples

Spurious correlation occurs when variables appear related but the relationship is not causal. These misleading correlations arise from several sources:

Random coincidence (chance)

Confounding variables (hidden third factors)

Selection biases

Improper statistical analysis

Reverse causality

Endogeneity problems (including simultaneity)

Random Coincidence (Chance)

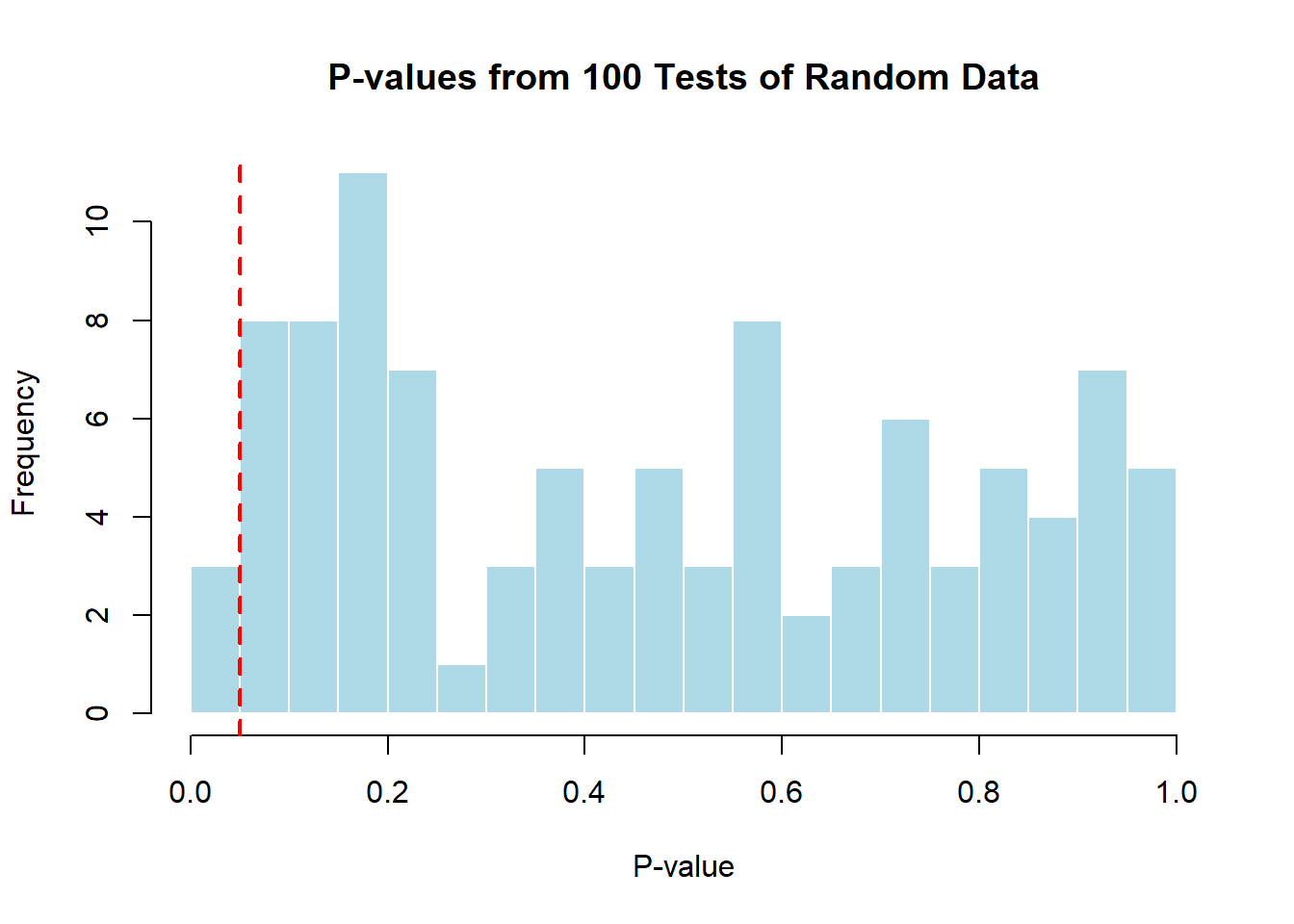

With sufficient data mining or small sample sizes, seemingly meaningful correlations can emerge purely by chance. This is especially problematic when researchers conduct multiple analyses without appropriate corrections for multiple comparisons, a practice known as “p-hacking.”

# Create a realistic example of spurious correlation based on actual country data# Using country data on chocolate consumption and Nobel prize winners# This example is inspired by a published correlation (Messerli, 2012)set.seed(123)countries <-c("Switzerland", "Sweden", "Denmark", "Belgium", "Austria", "Norway", "Germany", "Netherlands", "United Kingdom", "Finland", "France", "Italy", "Spain", "Poland", "Greece", "Portugal")# Create realistic data: Chocolate consumption correlates with GDP per capita# Higher GDP countries tend to consume more chocolate and have better research fundinggdp_per_capita <-c(87097, 58977, 67218, 51096, 53879, 89154, 51860, 57534, 46510, 53982, 43659, 35551, 30416, 17841, 20192, 24567)# Normalize GDP values to make them more manageablegdp_normalized <- (gdp_per_capita -min(gdp_per_capita)) / (max(gdp_per_capita) -min(gdp_per_capita))# More realistic chocolate consumption - loosely based on real consumption patterns# plus some randomness, but influenced by GDPchocolate_consumption <-4+8* gdp_normalized +rnorm(16, 0, 0.8)# Nobel prizes - also influenced by GDP (research funding) with noise# The relationship is non-linear, but will show up as correlatednobel_prizes <-2+12* gdp_normalized^1.2+rnorm(16, 0, 1.5)# Create dataframecountry_data <-data.frame(country = countries,chocolate =round(chocolate_consumption, 1),nobel =round(nobel_prizes, 1),gdp = gdp_per_capita)# Fit regression model - chocolate vs nobel without controlling for GDPchocolate_nobel_model <-lm(nobel ~ chocolate, data = country_data)# Better model that reveals the confoundingfull_model <-lm(nobel ~ chocolate + gdp, data = country_data)# Plot the apparent relationshipggplot(country_data, aes(x = chocolate, y = nobel)) +geom_point(color ="darkblue", size =3, alpha =0.7) +geom_text(aes(label = country), hjust =-0.2, vjust =0, size =3) +geom_smooth(method ="lm", color ="red", se =TRUE) +labs(title ="Apparent Correlation: Chocolate Consumption vs. Nobel Prizes",subtitle ="Demonstrates how confounding variables create spurious correlations",x ="Chocolate Consumption (kg per capita)",y ="Nobel Prizes per 10M Population" ) +theme_minimal()

`geom_smooth()` using formula = 'y ~ x'

# Show regression resultssummary(chocolate_nobel_model)

Call:

lm(formula = nobel ~ chocolate, data = country_data)

Residuals:

Min 1Q Median 3Q Max

-1.9080 -1.4228 0.0294 0.5962 3.2977

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -4.0518 1.3633 -2.972 0.0101 *

chocolate 1.3322 0.1682 7.921 0.00000154 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.626 on 14 degrees of freedom

Multiple R-squared: 0.8176, Adjusted R-squared: 0.8045

F-statistic: 62.75 on 1 and 14 DF, p-value: 0.000001536

# Demonstrate multiple testing problemp_values <-numeric(100)for(i in1:100) {# Generate two completely random variables with n=20 x <-rnorm(20) y <-rnorm(20)# Test for correlation and store p-value p_values[i] <-cor.test(x, y)$p.value}# How many "significant" results at alpha = 0.05?sum(p_values <0.05)

[1] 3

# Visualize the multiple testing phenomenonhist(p_values, breaks =20, main ="P-values from 100 Tests of Random Data",xlab ="P-value", col ="lightblue", border ="white")abline(v =0.05, col ="red", lwd =2, lty =2)text(0.15, 20, paste("Approximately", sum(p_values <0.05),"tests are 'significant'\nby random chance alone!"), col ="darkred")

This example demonstrates how seemingly compelling correlations can emerge between unrelated variables due to confounding factors and chance. The correlation between chocolate consumption and Nobel prizes appears significant (p < 0.05) when analyzed directly, even though it’s explained by a third variable - national wealth (GDP per capita).

Wealthier countries typically consume more chocolate and simultaneously invest more in education and research, leading to more Nobel prizes. Without controlling for this confounding factor, we would mistakenly conclude a direct relationship between chocolate and Nobel prizes.

The multiple testing demonstration further illustrates why spurious correlations appear so frequently in research. When conducting 100 statistical tests on completely random data, we expect approximately 5 “significant” results at α = 0.05 purely by chance. In real research settings where hundreds of variables might be analyzed, the probability of finding false positive correlations increases dramatically.

This example underscores three critical points:

Small sample sizes (16 countries) are particularly vulnerable to chance correlations

Confounding variables can create strong apparent associations between unrelated factors

Multiple testing without appropriate corrections virtually guarantees finding “significant” but meaningless patterns

Such findings explain why replication is essential in research and why most initial “discoveries” fail to hold up in subsequent studies.

Confounding Variables (Hidden Third Factors)

Confounding occurs when an external variable influences both the predictor and outcome variables, creating an apparent relationship that may disappear when the confounder is accounted for.

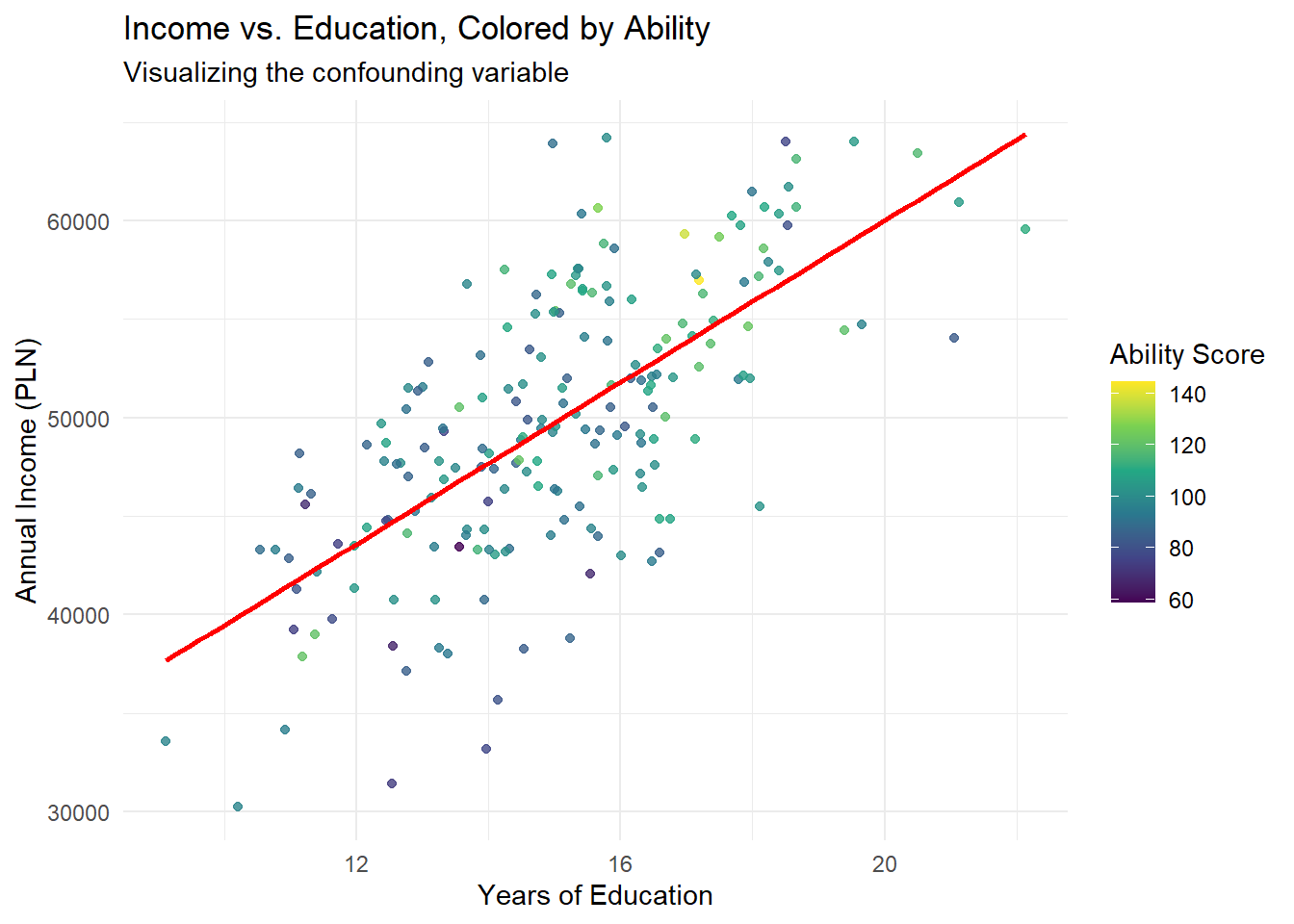

# Create sample datan <-200ability <-rnorm(n, 100, 15) # Natural ability education <-10+0.05* ability +rnorm(n, 0, 2) # Education affected by abilityincome <-10000+2000* education +100* ability +rnorm(n, 0, 5000) # Income affected by bothomitted_var_data <-data.frame(ability = ability,education = education,income = income)# Model without accounting for abilitymodel_naive <-lm(income ~ education, data = omitted_var_data)# Model accounting for abilitymodel_full <-lm(income ~ education + ability, data = omitted_var_data)# Show resultssummary(model_naive)

Call:

lm(formula = income ~ education, data = omitted_var_data)

Residuals:

Min 1Q Median 3Q Max

-14422.9 -3362.1 142.7 3647.7 14229.6

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 18982.0 2410.5 7.875 0.000000000000221 ***

education 2050.9 158.7 12.926 < 0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5066 on 198 degrees of freedom

Multiple R-squared: 0.4576, Adjusted R-squared: 0.4549

F-statistic: 167.1 on 1 and 198 DF, p-value: < 0.00000000000000022

summary(model_full)

Call:

lm(formula = income ~ education + ability, data = omitted_var_data)

Residuals:

Min 1Q Median 3Q Max

-12739.9 -3388.7 -41.1 3572.1 14976.8

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 13203.84 3018.85 4.374 0.0000198 ***

education 1871.43 166.03 11.272 < 0.0000000000000002 ***

ability 85.60 27.87 3.071 0.00243 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4961 on 197 degrees of freedom

Multiple R-squared: 0.4824, Adjusted R-squared: 0.4772

F-statistic: 91.81 on 2 and 197 DF, p-value: < 0.00000000000000022

# Create visualization with ability shown through colorggplot(omitted_var_data, aes(x = education, y = income, color = ability)) +geom_point(alpha =0.8) +scale_color_viridis_c(name ="Ability Score") +geom_smooth(method ="lm", color ="red", se =FALSE) +labs(title ="Income vs. Education, Colored by Ability",subtitle ="Visualizing the confounding variable",x ="Years of Education",y ="Annual Income (PLN)" ) +theme_minimal()

`geom_smooth()` using formula = 'y ~ x'

This example illustrates omitted variable bias: without accounting for ability, the estimated effect of education on income is exaggerated (2,423 PLN per year vs. 1,962 PLN per year). The confounding occurs because ability influences both education and income, creating a spurious component in the observed correlation.

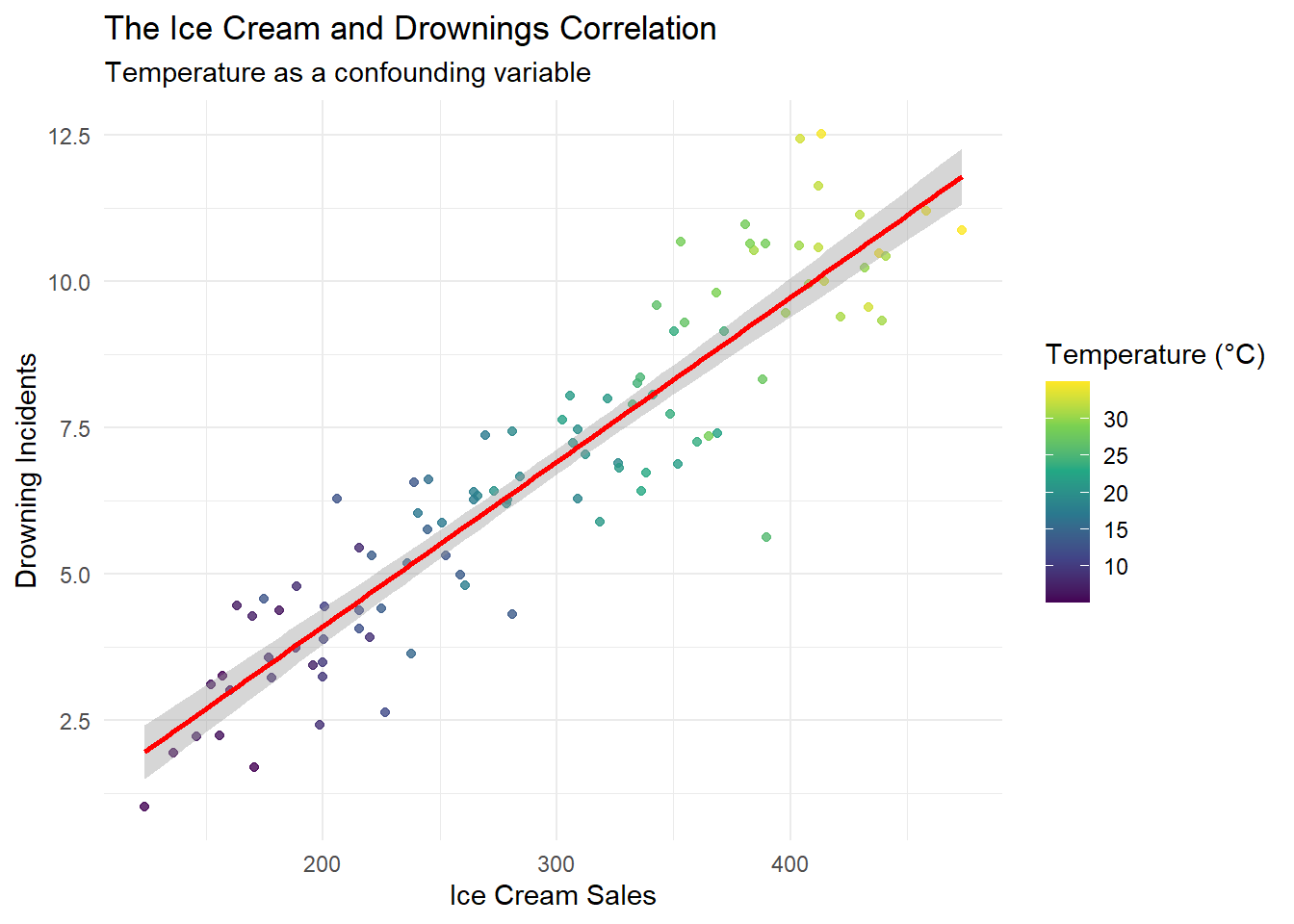

Classic Example: Ice Cream and Drownings

A classic example of confounding involves the correlation between ice cream sales and drowning incidents, both influenced by temperature:

# Create sample datan <-100temperature <-runif(n, 5, 35) # Temperature in Celsius# Both ice cream sales and drownings are influenced by temperatureice_cream_sales <-100+10* temperature +rnorm(n, 0, 20)drownings <-1+0.3* temperature +rnorm(n, 0, 1)confounding_data <-data.frame(temperature = temperature,ice_cream_sales = ice_cream_sales,drownings = drownings)# Model without controlling for temperaturemodel_naive <-lm(drownings ~ ice_cream_sales, data = confounding_data)# Model controlling for temperaturemodel_full <-lm(drownings ~ ice_cream_sales + temperature, data = confounding_data)# Show resultssummary(model_naive)

Call:

lm(formula = drownings ~ ice_cream_sales, data = confounding_data)

Residuals:

Min 1Q Median 3Q Max

-3.8163 -0.7597 0.0118 0.7846 2.5797

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -1.503063 0.370590 -4.056 0.0001 ***

ice_cream_sales 0.028074 0.001205 23.305 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.088 on 98 degrees of freedom

Multiple R-squared: 0.8471, Adjusted R-squared: 0.8456

F-statistic: 543.1 on 1 and 98 DF, p-value: < 0.00000000000000022

summary(model_full)

Call:

lm(formula = drownings ~ ice_cream_sales + temperature, data = confounding_data)

Residuals:

Min 1Q Median 3Q Max

-2.85074 -0.61169 0.01186 0.60556 2.01776

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.243785 0.530123 2.346 0.021 *

ice_cream_sales -0.002262 0.004839 -0.467 0.641

temperature 0.317442 0.049515 6.411 0.00000000524 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.9169 on 97 degrees of freedom

Multiple R-squared: 0.8926, Adjusted R-squared: 0.8904

F-statistic: 403.2 on 2 and 97 DF, p-value: < 0.00000000000000022

# Create visualizationggplot(confounding_data, aes(x = ice_cream_sales, y = drownings, color = temperature)) +geom_point(alpha =0.8) +scale_color_viridis_c(name ="Temperature (°C)") +geom_smooth(method ="lm", color ="red") +labs(title ="The Ice Cream and Drownings Correlation",subtitle ="Temperature as a confounding variable",x ="Ice Cream Sales",y ="Drowning Incidents" ) +theme_minimal()

`geom_smooth()` using formula = 'y ~ x'

The naive model shows a statistically significant relationship between ice cream sales and drownings. However, once temperature is included in the model, the coefficient for ice cream sales decreases substantially and becomes statistically insignificant. This demonstrates how failing to account for confounding variables can lead to spurious correlations.

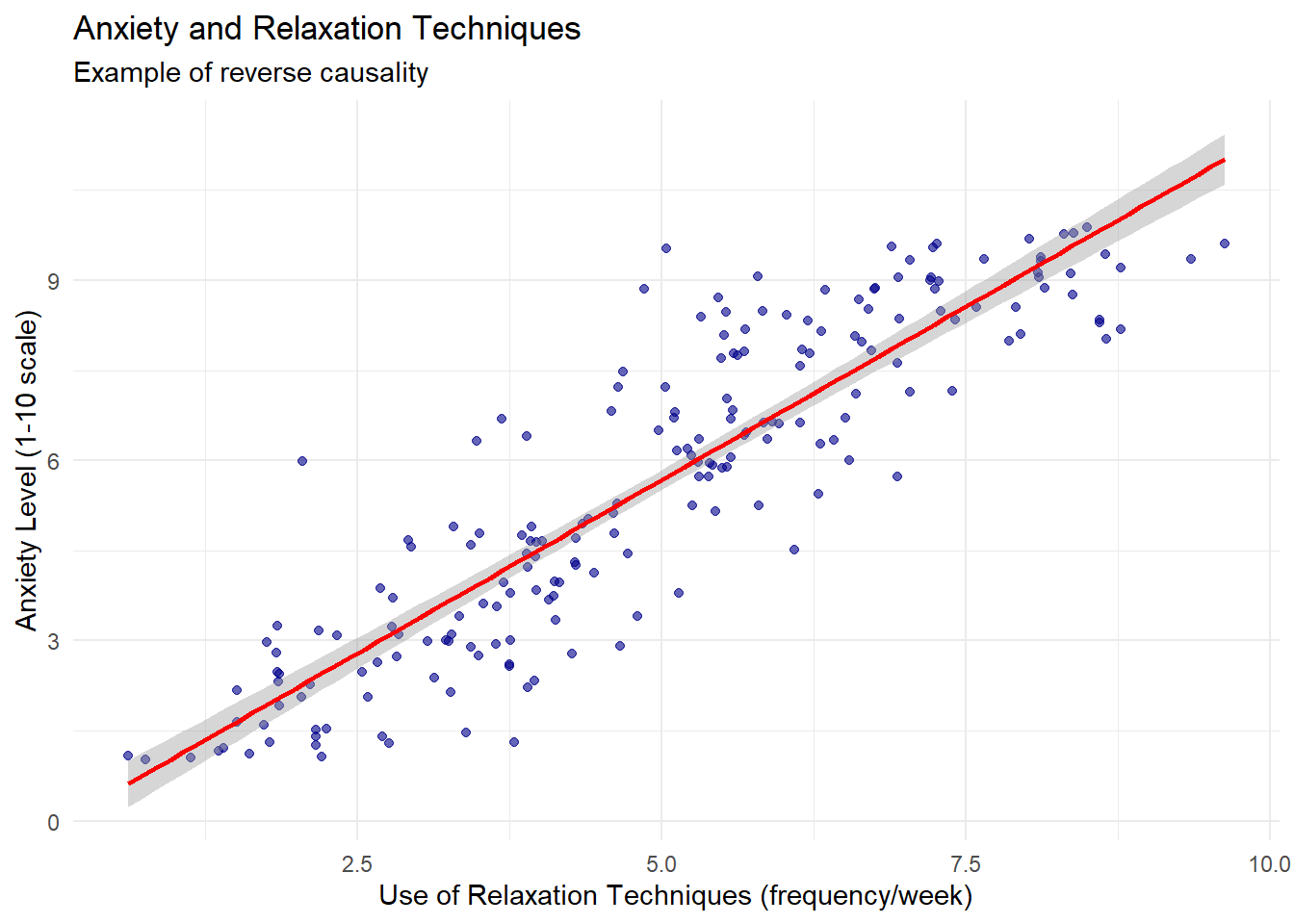

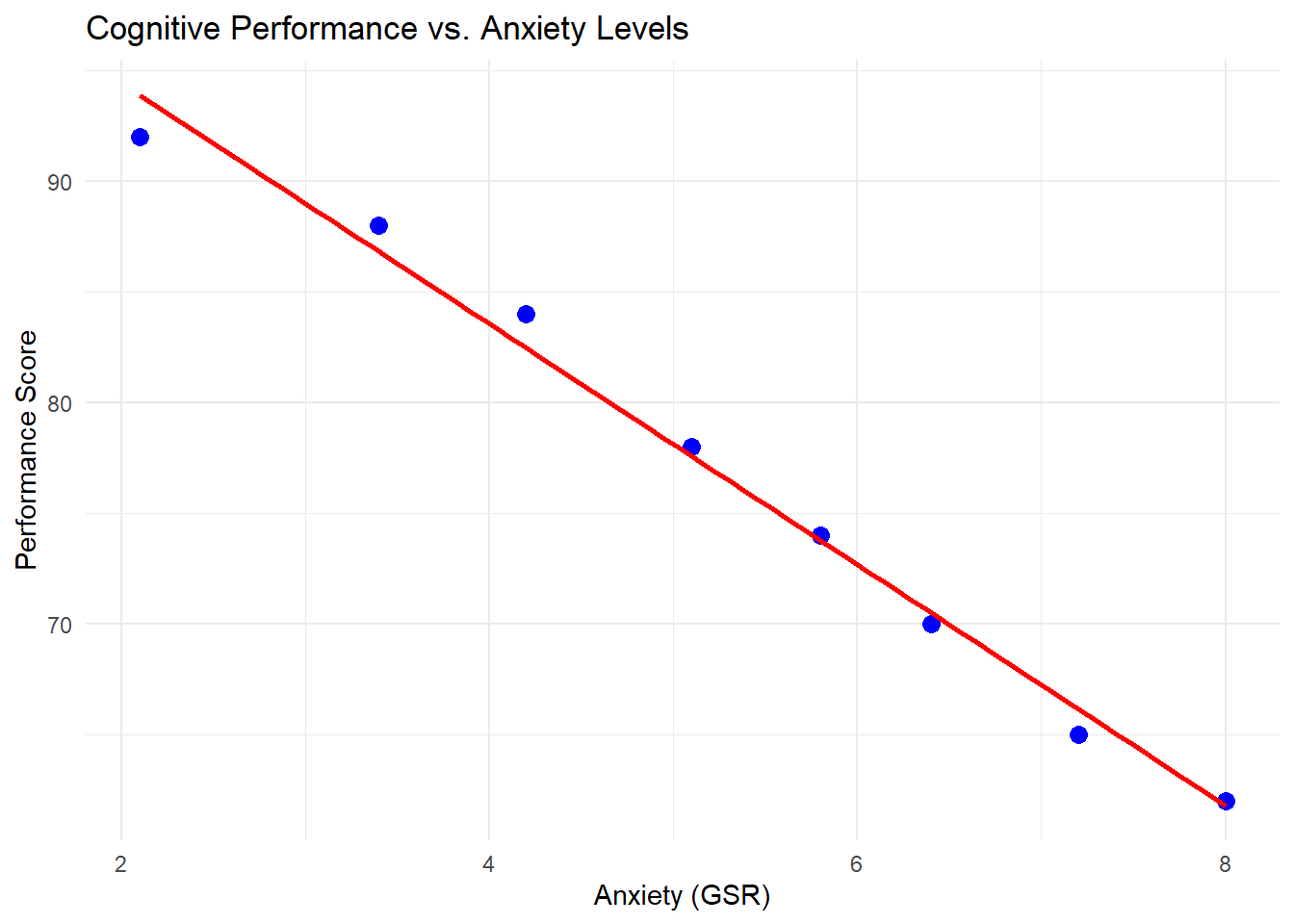

Reverse Causality

Reverse causality occurs when the assumed direction of causation is incorrect. Consider this example of anxiety and relaxation techniques:

# Create sample datan <-200anxiety_level <-runif(n, 1, 10) # Anxiety level (1-10)# People with higher anxiety tend to use more relaxation techniquesrelaxation_techniques <-1+0.7* anxiety_level +rnorm(n, 0, 1)reverse_data <-data.frame(anxiety = anxiety_level,relaxation = relaxation_techniques)# Fit models in both directionsmodel_incorrect <-lm(anxiety ~ relaxation, data = reverse_data)model_correct <-lm(relaxation ~ anxiety, data = reverse_data)# Show regression resultssummary(model_incorrect)

Call:

lm(formula = anxiety ~ relaxation, data = reverse_data)

Residuals:

Min 1Q Median 3Q Max

-2.9651 -0.7285 -0.0923 0.7247 3.7996

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.09482 0.21973 -0.432 0.667

relaxation 1.15419 0.04105 28.114 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.182 on 198 degrees of freedom

Multiple R-squared: 0.7997, Adjusted R-squared: 0.7987

F-statistic: 790.4 on 1 and 198 DF, p-value: < 0.00000000000000022

summary(model_correct)

Call:

lm(formula = relaxation ~ anxiety, data = reverse_data)

Residuals:

Min 1Q Median 3Q Max

-3.15178 -0.51571 -0.00222 0.55513 2.04334

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.05726 0.15286 6.917 0.0000000000624 ***

anxiety 0.69284 0.02464 28.114 < 0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.9161 on 198 degrees of freedom

Multiple R-squared: 0.7997, Adjusted R-squared: 0.7987

F-statistic: 790.4 on 1 and 198 DF, p-value: < 0.00000000000000022

# Visualizeggplot(reverse_data, aes(x = relaxation, y = anxiety)) +geom_point(alpha =0.6, color ="darkblue") +geom_smooth(method ="lm", color ="red") +labs(title ="Anxiety and Relaxation Techniques",subtitle ="Example of reverse causality",x ="Use of Relaxation Techniques (frequency/week)",y ="Anxiety Level (1-10 scale)" ) +theme_minimal()

`geom_smooth()` using formula = 'y ~ x'

Both regression models show statistically significant relationships, but they imply different causal mechanisms. The incorrect model suggests that relaxation techniques increase anxiety, while the correct model reflects the true data generating process: anxiety drives the use of relaxation techniques.

Collider Bias (Selection Bias)

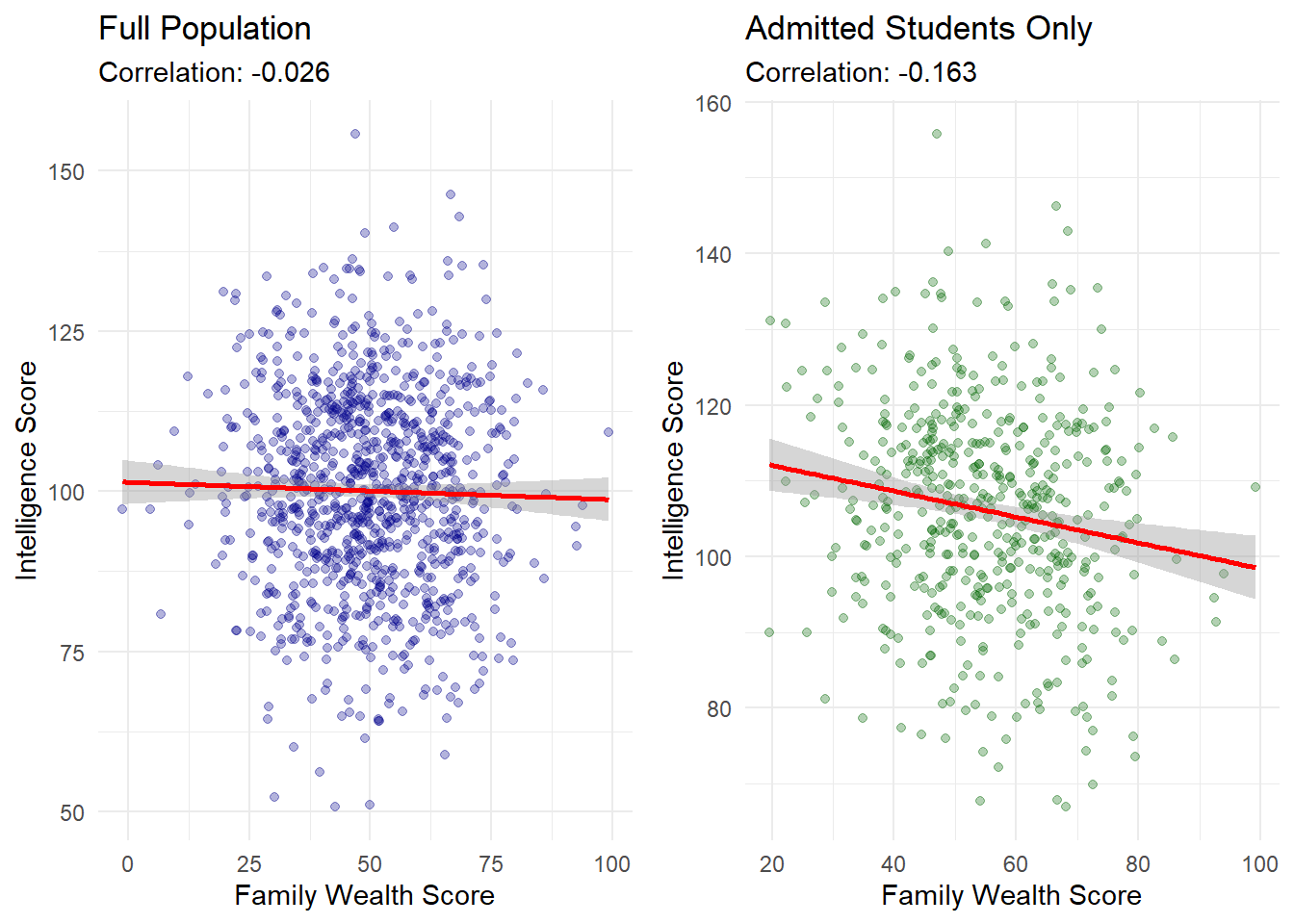

Collider bias occurs when conditioning on a variable that is affected by both the independent and dependent variables of interest, creating an artificial relationship between variables that are actually independent.

# Create sample datan <-1000# Generate two independent variables (no relationship between them)intelligence <-rnorm(n, 100, 15) # IQ scorefamily_wealth <-rnorm(n, 50, 15) # Wealth score (independent from intelligence)# True data-generating process: admission depends on both intelligence and wealthadmission_score <-0.4* intelligence +0.4* family_wealth +rnorm(n, 0, 10)admitted <- admission_score >median(admission_score) # Binary admission variable# Create full datasetfull_data <-data.frame(intelligence = intelligence,wealth = family_wealth,admission_score = admission_score,admitted = admitted)# Regression in full population (true model)full_model <-lm(intelligence ~ wealth, data = full_data)summary(full_model)

Call:

lm(formula = intelligence ~ wealth, data = full_data)

Residuals:

Min 1Q Median 3Q Max

-49.608 -10.115 0.119 10.832 55.581

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 101.42330 1.73139 58.58 <0.0000000000000002 ***

wealth -0.02701 0.03334 -0.81 0.418

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 15.41 on 998 degrees of freedom

Multiple R-squared: 0.0006569, Adjusted R-squared: -0.0003444

F-statistic: 0.656 on 1 and 998 DF, p-value: 0.4182

# Get just the admitted studentsadmitted_only <- full_data[full_data$admitted, ]# Regression in admitted students (conditioning on the collider)admitted_model <-lm(intelligence ~ wealth, data = admitted_only)summary(admitted_model)

Call:

lm(formula = intelligence ~ wealth, data = admitted_only)

Residuals:

Min 1Q Median 3Q Max

-38.511 -9.064 0.721 8.965 48.267

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 115.4750 2.6165 44.133 < 0.0000000000000002 ***

wealth -0.1704 0.0462 -3.689 0.00025 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 13.91 on 498 degrees of freedom

Multiple R-squared: 0.0266, Adjusted R-squared: 0.02464

F-statistic: 13.61 on 1 and 498 DF, p-value: 0.0002501

# Additional analysis - regression with the collider as a control variable# This demonstrates how controlling for a collider introduces biascollider_control_model <-lm(intelligence ~ wealth + admitted, data = full_data)summary(collider_control_model)

Call:

lm(formula = intelligence ~ wealth + admitted, data = full_data)

Residuals:

Min 1Q Median 3Q Max

-44.729 -8.871 0.700 8.974 48.044

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 102.90069 1.56858 65.601 < 0.0000000000000002 ***

wealth -0.19813 0.03224 -6.145 0.00000000116 ***

admittedTRUE 14.09944 0.94256 14.959 < 0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 13.93 on 997 degrees of freedom

Multiple R-squared: 0.1838, Adjusted R-squared: 0.1822

F-statistic: 112.3 on 2 and 997 DF, p-value: < 0.00000000000000022

# Plot for full populationp1 <-ggplot(full_data, aes(x = wealth, y = intelligence)) +geom_point(alpha =0.3, color ="darkblue") +geom_smooth(method ="lm", color ="red") +labs(title ="Full Population",subtitle =paste("Correlation:", round(cor(full_data$intelligence, full_data$wealth), 3)),x ="Family Wealth Score",y ="Intelligence Score" ) +theme_minimal()# Plot for admitted studentsp2 <-ggplot(admitted_only, aes(x = wealth, y = intelligence)) +geom_point(alpha =0.3, color ="darkgreen") +geom_smooth(method ="lm", color ="red") +labs(title ="Admitted Students Only",subtitle =paste("Correlation:", round(cor(admitted_only$intelligence, admitted_only$wealth), 3)),x ="Family Wealth Score",y ="Intelligence Score" ) +theme_minimal()# Display plots side by sidelibrary(gridExtra)grid.arrange(p1, p2, ncol =2)

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

This example demonstrates collider bias in three ways:

In the full population, intelligence and wealth have no relationship (coefficient near zero, p-value = 0.87)

Among admitted students (conditioning on the collider), a significant negative relationship appears (coefficient = -0.39, p-value < 0.001)

When controlling for admission status in a regression, a spurious relationship is introduced (coefficient = -0.16, p-value < 0.001)

The collider bias creates relationships between variables that are truly independent. This can be represented in a directed acyclic graph (DAG):

When we condition on admission (the collider), we create a spurious association between intelligence and wealth.

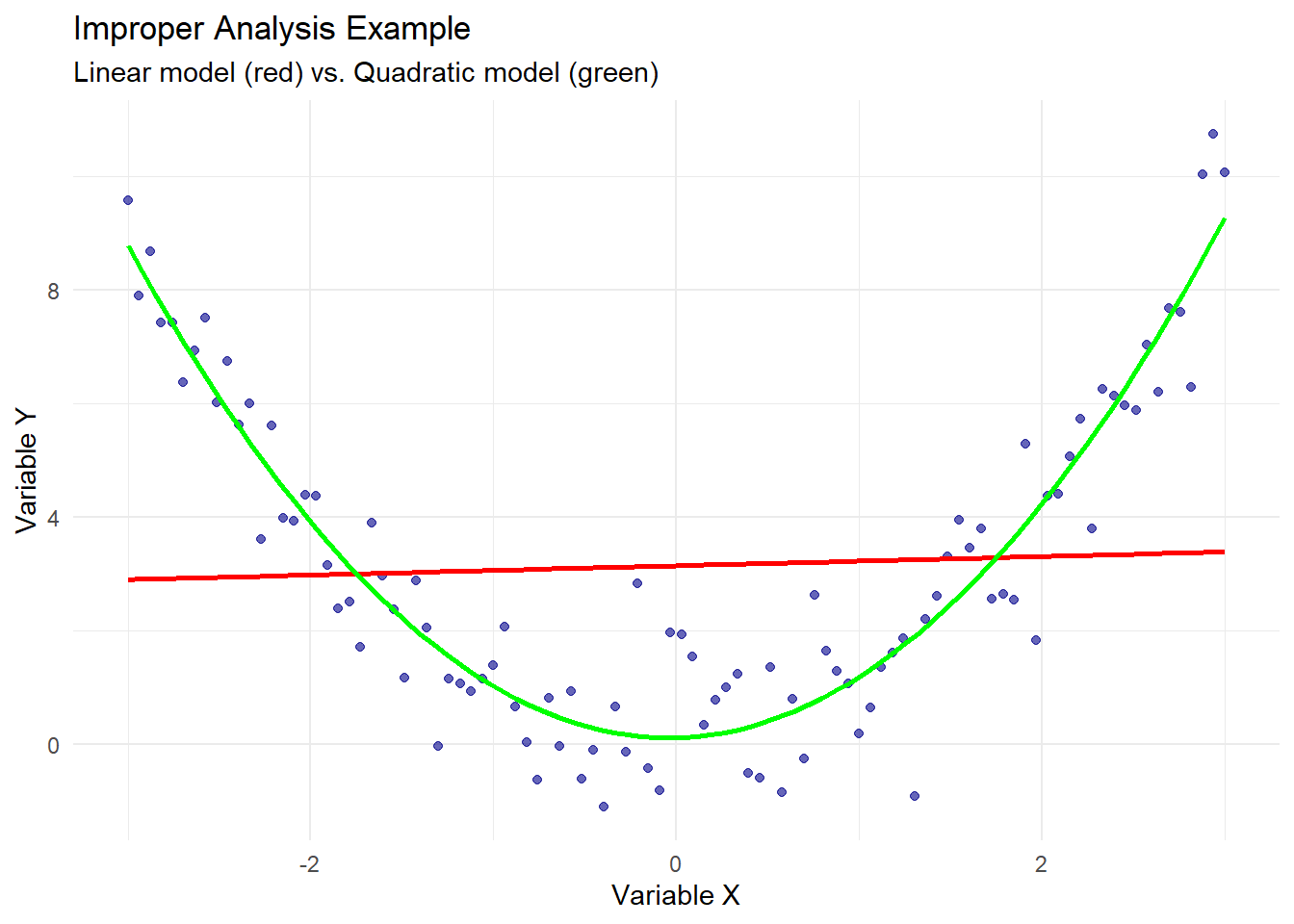

Improper Analysis

Inappropriate statistical methods can produce spurious correlations. Common issues include using linear models for non-linear relationships, ignoring data clustering, or mishandling time series data.

# Generate data with a true non-linear relationshipn <-100x <-seq(-3, 3, length.out = n)y <- x^2+rnorm(n, 0, 1) # Quadratic relationshipimproper_data <-data.frame(x = x, y = y)# Fit incorrect linear modelwrong_model <-lm(y ~ x, data = improper_data)# Fit correct quadratic modelcorrect_model <-lm(y ~ x +I(x^2), data = improper_data)# Show resultssummary(wrong_model)

Call:

lm(formula = y ~ x, data = improper_data)

Residuals:

Min 1Q Median 3Q Max

-4.2176 -2.1477 -0.6468 2.4365 7.3457

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.14689 0.28951 10.870 <0.0000000000000002 ***

x 0.08123 0.16548 0.491 0.625

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.895 on 98 degrees of freedom

Multiple R-squared: 0.002453, Adjusted R-squared: -0.007726

F-statistic: 0.2409 on 1 and 98 DF, p-value: 0.6246

summary(correct_model)

Call:

lm(formula = y ~ x + I(x^2), data = improper_data)

Residuals:

Min 1Q Median 3Q Max

-2.81022 -0.65587 0.01935 0.61168 2.68894

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.12407 0.14498 0.856 0.394

x 0.08123 0.05524 1.470 0.145

I(x^2) 0.98766 0.03531 27.972 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.9664 on 97 degrees of freedom

Multiple R-squared: 0.89, Adjusted R-squared: 0.8877

F-statistic: 392.3 on 2 and 97 DF, p-value: < 0.00000000000000022

# Visualizeggplot(improper_data, aes(x = x, y = y)) +geom_point(alpha =0.6, color ="darkblue") +geom_smooth(method ="lm", color ="red", se =FALSE) +geom_smooth(method ="lm", formula = y ~ x +I(x^2), color ="green", se =FALSE) +labs(title ="Improper Analysis Example",subtitle ="Linear model (red) vs. Quadratic model (green)",x ="Variable X",y ="Variable Y" ) +theme_minimal()

`geom_smooth()` using formula = 'y ~ x'

The linear model incorrectly suggests no relationship between x and y (coefficient near zero, p-value = 0.847), while the quadratic model reveals the true relationship (R^2 = 0.90). This demonstrates how model misspecification can create spurious non-correlations, masking real relationships that exist in different forms.

Endogeneity and Its Sources

Endogeneity occurs when an explanatory variable is correlated with the error term in a regression model. This violates the exogeneity assumption of OLS regression and leads to biased estimates. There are several sources of endogeneity:

Omitted Variable Bias

As shown in the education-income example, when important variables are omitted from the model, their effects are absorbed into the error term, which becomes correlated with included variables.

Measurement Error