Statistics is the science of learning from data under uncertainty.

Statistics is a way to learn about the world from data. It teaches how to collect data wisely, spot patterns, estimate population parameters, and make predictions—stating how wrong we might be.

Note

Statistics is the science of collecting, organizing, analyzing, interpreting, and presenting data. It encompasses both the methods for working with data and the theoretical foundations that justify these methods.

But statistics is more than just numbers and formulas—it’s a way of thinking about uncertainty and variation in the world around us.

What is Data?

Data: Information collected during research – this includes survey responses, experimental results, economic indicators, social media content, or any other measurable observations.

A data distribution describes how values spread across possible outcomes (what values and how often a variable takes). Distributions tell us what values are common, what values are rare, and what patterns exist in our data.

Demography is the scientific study of human populations, focusing on their size, structure, distribution, and changes over time. It’s essentially the statistical analysis of people - who they are, where they live, how many there are, and how these characteristics evolve.

Statistics and demography are interconnected disciplines that provide powerful tools for understanding populations, their characteristics, and the patterns that emerge from data.

Rounding and Scientific Notation

Main Rule: Unless otherwise specified, round the decimal parts of decimal numbers to at least 2 significant figures. In statistics, we often work with long decimal parts and very small numbers — don’t round excessively in intermediate steps, round at the end of calculations.

Rounding in Statistical Context

The decimal part consists of digits after the decimal point. In statistics, it’s particularly important to maintain appropriate precision:

Descriptive statistics:

Mean: \bar{x} = 15.847693... \rightarrow 15.85

Standard deviation: s = 2.7488... \rightarrow 2.75

Correlation coefficient: r = 0.78432... \rightarrow 0.78

Very small numbers (p-values, probabilities):

p = 0.000347... \rightarrow 0.00035 or 3.5 \times 10^{-4}

When in doubt: Better to keep an extra digit than to round too aggressively

What is Statistics For in Social and Political Science?

Statistics is essential in social and political science for several key purposes:

Understanding Social Phenomena: Measuring inequality, poverty, unemployment, political participation; describing demographic patterns and social trends; quantifying attitudes, beliefs, and behaviors in populations.

Testing Theories: Political scientists theorize about democracy, voting behavior, conflict, and institutions. Sociologists develop theories about social mobility, inequality, and group dynamics. Statistics allows us to test whether these theories match reality.

Causal Inference: Social scientists want to answer “why” questions—Does education increase income? Do democracies go to war less often? Does social media affect political polarization? Statistics helps separate causation from mere correlation.

Policy Evaluation: Assessing whether interventions work—Does a job training program reduce unemployment? Did election reform increase voter turnout? Are anti-poverty programs effective? Statistics provides tools to evaluate what works and what doesn’t.

Public Opinion Research: Election polls and forecasting; measuring public support for policies; understanding how opinions vary across demographic groups; tracking attitude changes over time.

Making Generalizations: We can’t survey everyone, so we sample and use statistics to make inferences about entire populations. A poll of 1,000 people can tell us about a nation of millions (with known uncertainty).

Dealing with Complexity: Human societies are messy—many factors influence outcomes simultaneously. Statistics helps us control for confounding variables, isolate specific effects, and make sense of multivariate relationships.

The Uniqueness of Social Sciences: Unlike natural sciences, social sciences study human behavior, which is highly variable and context-dependent. Statistics provides the tools to find patterns and draw conclusions despite this inherent uncertainty.

When working with data, statisticians use two different approaches: exploration and confirmation/verification (inferential statistics). First, we examine the data to understand its characteristics and identify patterns. Then, we use formal methods to test specific hypotheses and draw conclusions.

EDA vs. Inferential Statistics

Statistics can be viewed as two complementary phases:

Exploratory Data Analysis (EDA): combines descriptive statistics and visualization methods to explore data, uncover patterns, check assumptions, and generate hypotheses.

Inferential Statistics: uses probability models to test hypotheses and draw conclusions that generalize beyond the observed data.

Percent vs Percentage Points (pp)

When news reports say “unemployment decreased by 2,” do they mean 2 percentage points (pp) or 2 percent?

These are not the same:

2 pp (absolute change): e.g., 10% → 8% (−2 pp).

2% (relative change): multiply the old rate by 0.98; e.g., 10% → 9.8% (−0.2 pp).

Always ask:

What is the baseline (earlier rate)?

Is the change absolute (pp) or relative (%)?

Could this be sampling error / random variation?

How was unemployment measured (survey vs. administrative), when, and who’s included?

Rule of thumb

Use percentage points (pp) when comparing rates directly (unemployment, turnout).

Use percent (%) for relative changes (proportional to the starting value).

Tiny lookup table

Starting rate

“Down 2%” (relative)

“Down 2 pp” (absolute)

6%

6% × 0.98 = 5.88% (−0.12 pp)

4%

8%

8% × 0.98 = 7.84% (−0.16 pp)

6%

10%

10% × 0.98 = 9.8% (−0.2 pp)

8%

Uwaga (PL): 2% ≠ 2 punkty procentowe (pp).

1.2 Exploratory Data Analysis (EDA)

What is EDA? Exploratory Data Analysis is the initial step where we examine data systematically to understand its structure and characteristics. This phase does not involve formal hypothesis testing—it focuses on discovering what the data contains.

Why do we do EDA?

Find interesting patterns you didn’t expect

Spot mistakes or unusual values in your data

Get ideas about what questions to ask

Understand what your data looks like before doing formal tests (many statistical methods have specific requirements about the data to work properly. EDA helps check whether our data meets these requirements - e.g. 1) some tests require data to have a normal distribution (bell-shaped), 2) we need to verify that the relationship between variables is actually linear, or 3) check homogeneity of variance and find outliers)

The EDA Approach

When conducting EDA, we begin without predetermined hypotheses. Instead, we examine data from multiple perspectives to discover patterns and generate questions for further investigation.

Simple Tools for Exploring Data

1. Summary Numbers (Descriptive Statistics)

These are basic calculations that describe your data:

Finding the “Typical” Value:

Arithmetic Mean (Average): Add up all values and divide by how many you have. Example: If 5 students scored 70, 80, 85, 90, and 100 on a test, the average is 85.

Median (Middle): The value in the middle when you line up all numbers from smallest to largest. In our test example, the median is also 85.

Mode (Most Common): The value that appears most often. If ten families have 1, 2, 2, 2, 2, 3, 3, 3, 4, and 5 children, the mode is 2 children.

Understanding Spread:

Range: Just subtract the smallest number from the biggest. If students’ ages go from 18 to 24, the range is 6 years.

Standard Deviation: Shows how spread out your data is from the average. A small standard deviation means most values are close to the average; a large one means they’re more spread out.

2. Visual Exploration

Graphical methods help reveal patterns that numerical summaries alone might not show:

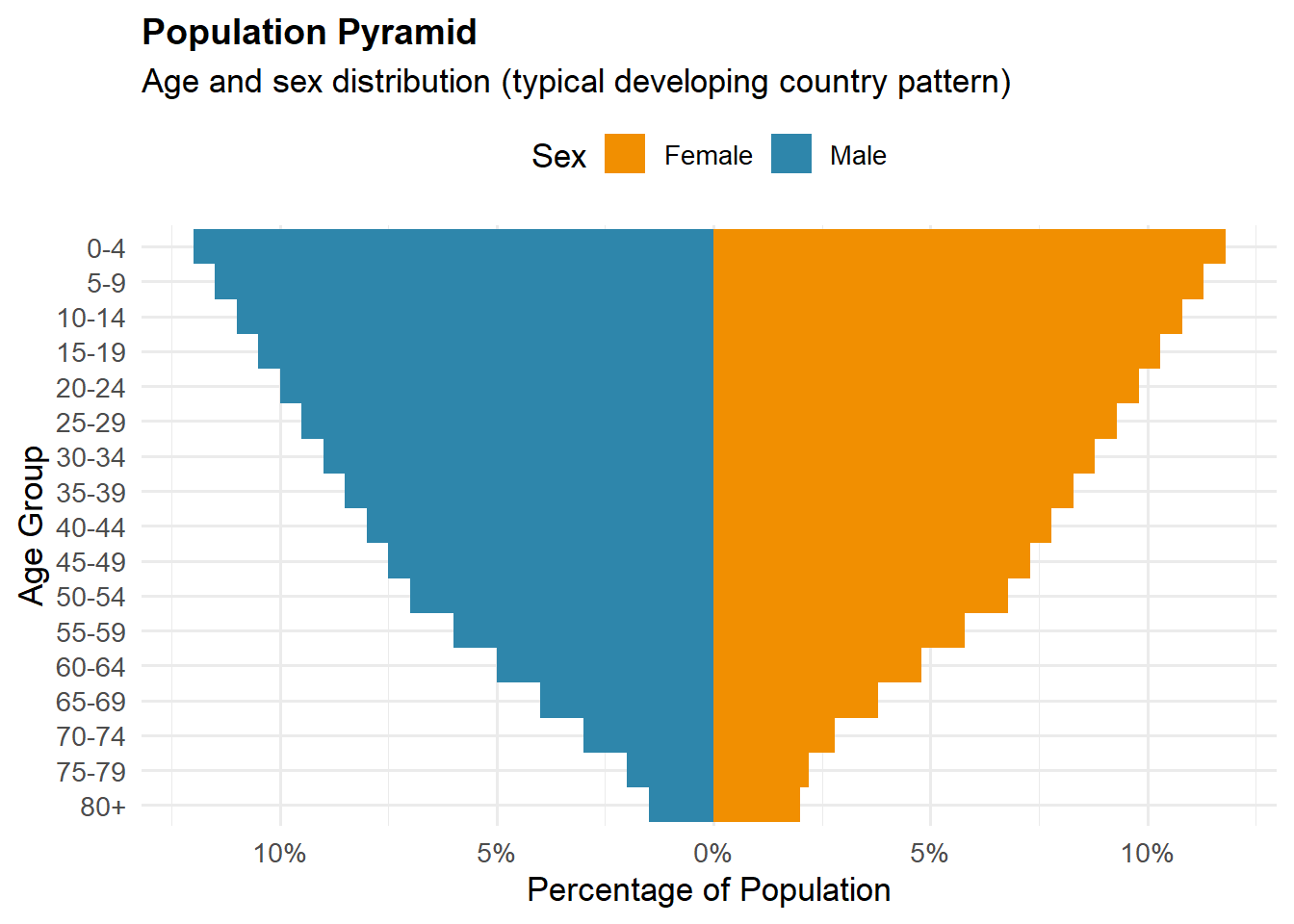

Population Pyramids: Show how many people are in each age group, split by males and females. Helps you see if a population is young or old.

Box Plots: Show the middle of your data and help spot unusual values

Scatter Plots: Display relationships between two variables (such as hours studied versus test scores)

Time (Series) Graphs: Show how something changes over time (like temperature throughout the year)

Histograms: A histogram is a graphical representation of data that shows the frequency distribution of a dataset. It consists of adjacent bars (with no gaps between them) where each bar represents a range of values (called a bin or class interval), and the height of the bar shows how many data points (what proportion of data points) fall within that range. Histograms are used to visualize the shape, spread, and central tendency of numerical data.

Do two variables move together? (When one goes up, does the other go up too?)

Can you draw a line (regression line) that roughly fits your data points?

Do you see any clear patterns or trends?

Using the Same Techniques for Different Purposes

Many statistical techniques serve both exploratory and confirmatory functions:

Exploring: We calculate correlations or fit regression lines to understand what relationships exist in the data. The focus is on discovering patterns.

Confirming: We apply statistical tests to determine whether observed patterns are statistically significant or could have occurred by chance. The focus is on formal hypothesis testing.

The same technique can serve different purposes depending on the research phase.

4. Good Questions to Ask While Exploring:

What does the shape of my data look like?

Are there any weird or unusual values?

Do I see any patterns?

Is any data missing?

Do different groups show different patterns?

1.3 Inferential Statistics

After exploring, you might want to make formal conclusions. Inferential statistics helps you do this.

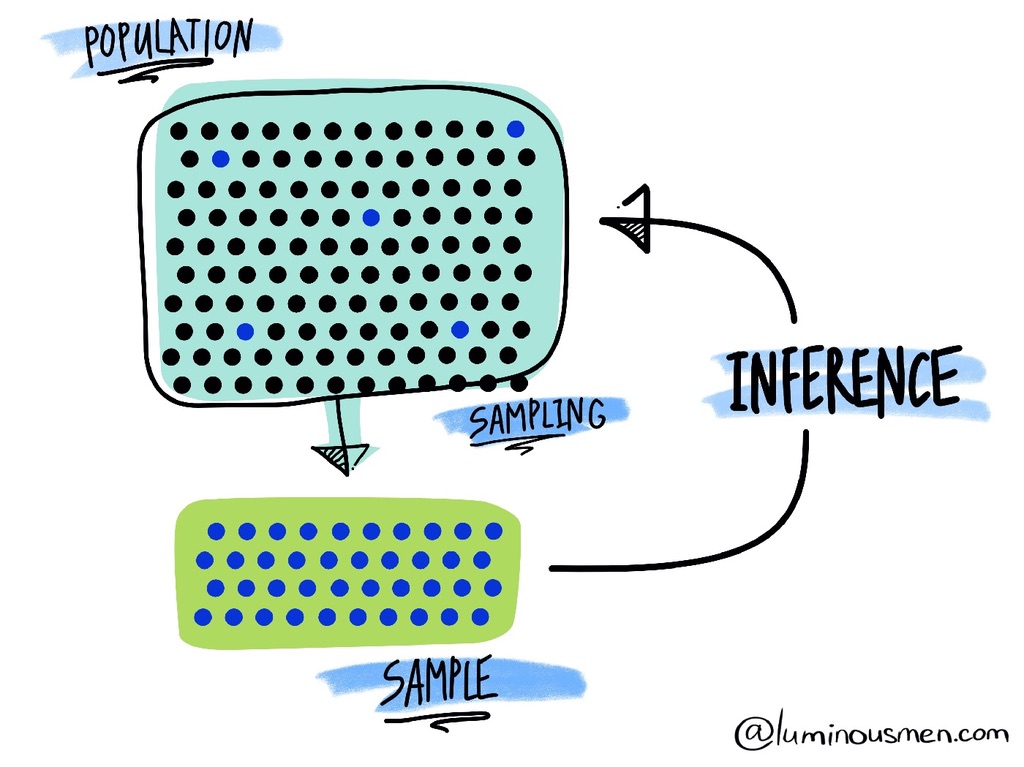

The Basic Idea: You have data from some people (a sample), but you want to know about everyone (the population). Inferential statistics helps you make educated guesses about the bigger group based on your smaller group.

Note

A random sample requires that each member has a known, non-zero chance of being selected, not necessarily an equal chance.

When every member has an equal chance of selection, that’s specifically called a simple random sample - which is the most basic type.

A Soup-Tasting Analogy

Consider a chef preparing soup for 100 people who needs to assess its flavor without consuming the entire batch:

Population: The entire pot of soup (100 servings) Sample: A single spoonful for tasting Population Parameter: The true average saltiness of the complete pot (unknown) Sample Statistic: The saltiness level detected in the spoonful (observable, a point estimate) Statistical Inference: Using the spoonful’s characteristics to draw conclusions about the entire pot

Key points

1. Random sampling is essential. The cook should stir thoroughly or sample from random locations. Skimming only the surface can miss seasonings that settled to the bottom, introducing systematic bias.

2. Sample size drives precision. A larger ladle — or more spoonfuls (larger n) — reduces random error and gives a more stable estimate of the “average taste,” though cost and time limit how much you can increase n.

3. Uncertainty is unavoidable. Even with proper sampling, a single spoonful may not perfectly represent the whole pot; there is always random variability.

4. Systematic bias undermines inference. If someone secretly adds salt only where you sample, conclusions about the whole pot will be distorted — a classic case of sampling bias.

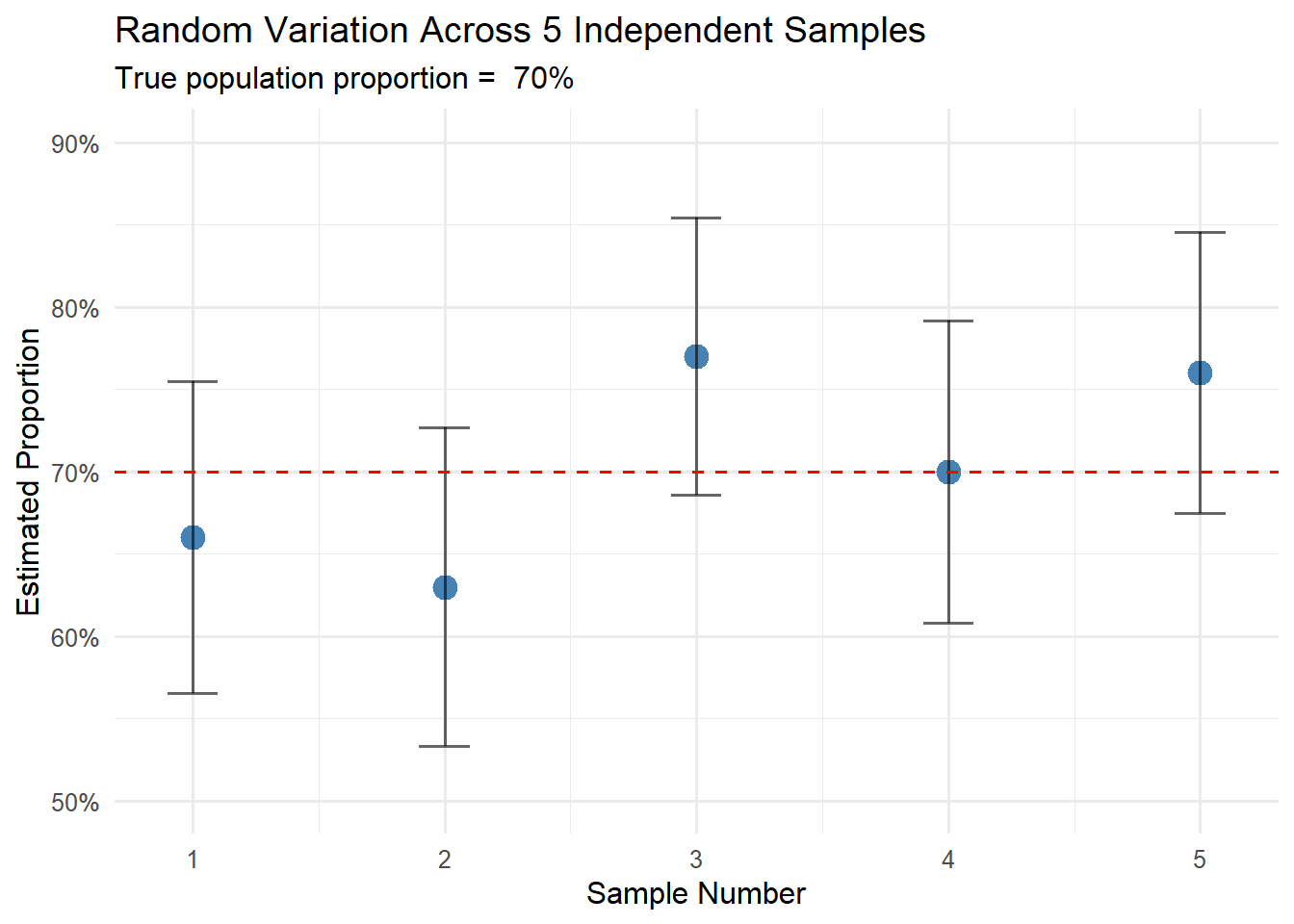

5. One sample is limited. A single taste can tell you the average saltiness, but not how much it varies across the pot. To assess variability, you need multiple independent samples.

Note: Increasing n improves precision (less noise) but does not remove bias; eliminating bias requires fixing the sampling design.

This analogy captures the essence of statistical reasoning: using carefully selected samples to learn about larger populations while explicitly acknowledging and quantifying the inherent uncertainty in this process.

Statistical Thinking

Key concepts (at a glance)

Pipeline:Research question → Estimand (population quantity) → Parameter (true, unknown value) → Estimator (sample rule/statistic; random) → Estimate (the single number from your data)

What we want to know:

Estimand — the population quantity we aim to learn (the formal target), not the sentence itself. Example: “Population mean age at first birth in Poland in 2023.”

Parameter(\theta) — the true but unknown value of that estimand in the population (fixed, not random). Example: The true mean \mu (e.g., \mu=29.4 years).

How we estimate (3 steps):

Sample statistic — any function of the sample (a rule), e.g. \displaystyle \bar{X}=\frac{1}{n}\sum_{i=1}^n X_i

Estimator — that statistic chosen to estimate a specific parameter (depends on a random sample, so it’s random). Example: Use \bar{X} as an estimator of \mu.

Estimate(\hat\theta) — the numerical result after applying the estimator to your observed data (x_1,\dots,x_n). Example:\hat\mu=\bar{x}=29.1 years.

Analogy:

Statistic = tool → Estimator = tool chosen for a goal → Estimate = the finished output (your concrete result)

Common estimators

Target parameter (goal)

Estimator (statistic)

Formula

Note

Population mean \mu

Sample mean

\bar X=\frac{1}{n}\sum_{i=1}^n X_i

Unbiased estimator. The estimator \bar X is a random variable; a specific calculated value (e.g., \bar x = 5.2) is called an estimate.

Population proportion p

Sample proportion

\hat p=\frac{K}{n} where K=\sum_{i=1}^n Y_i for Y_i\in\{0,1\}

Equivalent to \bar Y when encoding outcomes as 0/1. Here K counts the number of successes in n trials.

Population variance \sigma^2

Sample variance

s^2=\frac{1}{n-1}\sum_{i=1}^n (X_i-\bar X)^2

The n-1 divisor (Bessel’s correction) makes this unbiased for \sigma^2. Using n would give a biased estimator.

Every estimator is a statistic, but not every statistic is an estimator — until you tie it to a target (an estimand), it’s “just” a statistic.

How do we assess if an estimator (“method”) is good?

Bias — does our method give true results “on average”?

Imagine we want to know the average height of adult Poles (true value: 172 cm). We draw 100 different samples of 500 people each and calculate the mean for each one.

Unbiased estimator: Those 100 means will differ (169 cm, 173 cm, 171 cm…), but their average will be close to 172 cm. Sometimes we overestimate, sometimes underestimate, but there’s no systematic error.

Biased estimator: If we accidentally always excluded people over 180 cm, all our 100 means would be too low (e.g., oscillating around 168 cm). That’s systematic bias.

Variance — how much do results differ between samples?

We have two methods for estimating the same parameter. Both give good results “on average,” but:

Method A: from 10 samples we get: 171, 172, 173, 171, 172, 173, 172, 171, 173, 172 cm

Method B: from 10 samples we get: 165, 179, 168, 176, 171, 174, 169, 175, 167, 176 cm

Method A has lower variance — results are more concentrated, predictable. In practice, you prefer Method A because you can be more confident in a single result.

Key principle: Larger sample = lower variance. With a sample of 100 people, the mean will “jump around” more than with a sample of 1,000 people.

Mean Squared Error (MSE) — what matters more: unbiasedness or stability?

Sometimes we face a dilemma:

Estimator A: Unbiased (average 172 cm), but very unstable (results from 160 to 184 cm)

Estimator B: Slightly biased (average 171 cm instead of 172 cm), but very stable (results from 169 to 173 cm)

MSE says: Estimator B is better — a small systematic underestimation of 1 cm is less problematic than the huge spread of results in Estimator A.

Efficiency — which unbiased estimator to choose?

You have data on incomes of 500 people. You want to know the “typical” income. Two options:

Arithmetic mean: typically gives results in the range 4,800–5,200 PLN

Median: gives results in the range 4,500–5,500 PLN

If both methods are unbiased, choose the one with smaller spread (the mean is more efficient for normally distributed data).

Example of Statistical Thinking

Your university is considering keeping the library open 24/7. The administration needs to know: What proportion of students support this change?

Note

Ideal world: Ask all 20,000 students → Get the exact answer (\theta parameter) Real world: Survey 100 students → Get an estimate (\hat{\theta}) with uncertainty

Bias vs. Random Error

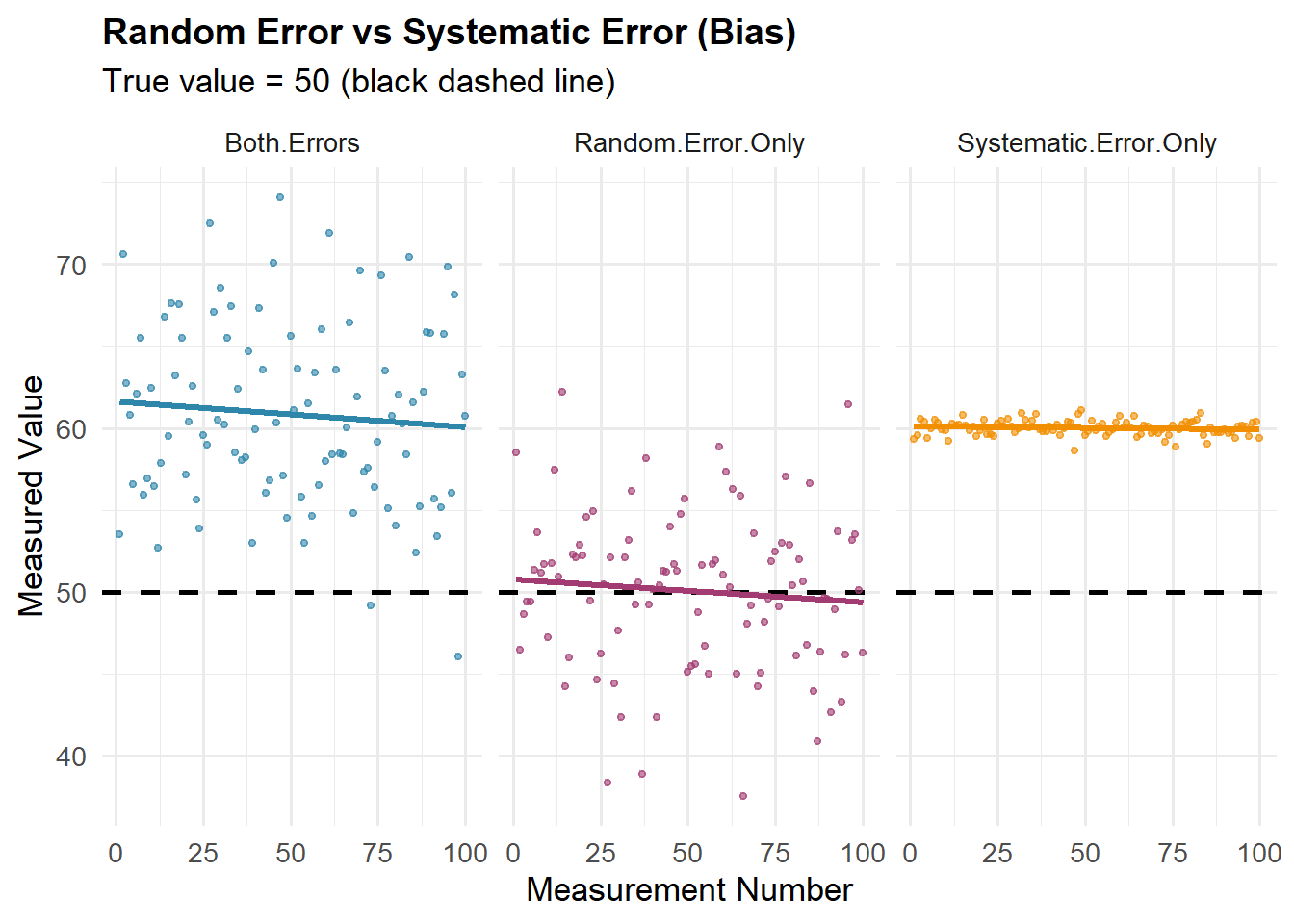

Statistical (prediction) error can be decomposed into two main components: bias (systematic error) and random error (unpredictable variation).

Bias is like a miscalibrated scale that consistently reads 2 kg too high—every measurement is wrong in the same direction. It’s systematic error.

Random error is the unpredictable variation in your observations, like:

A dart player aiming at the bullseye—each throw lands in a slightly different spot due to hand tremor, air currents, tiny muscle variations

Measuring someone’s height multiple times and getting 174.8 cm, 175.0 cm, 175.3 cm—small fluctuations from posture changes, breathing, how you read the scale, and natural body variations

A weather model that’s sometimes 2°C too high, sometimes 1°C too low, sometimes spot on

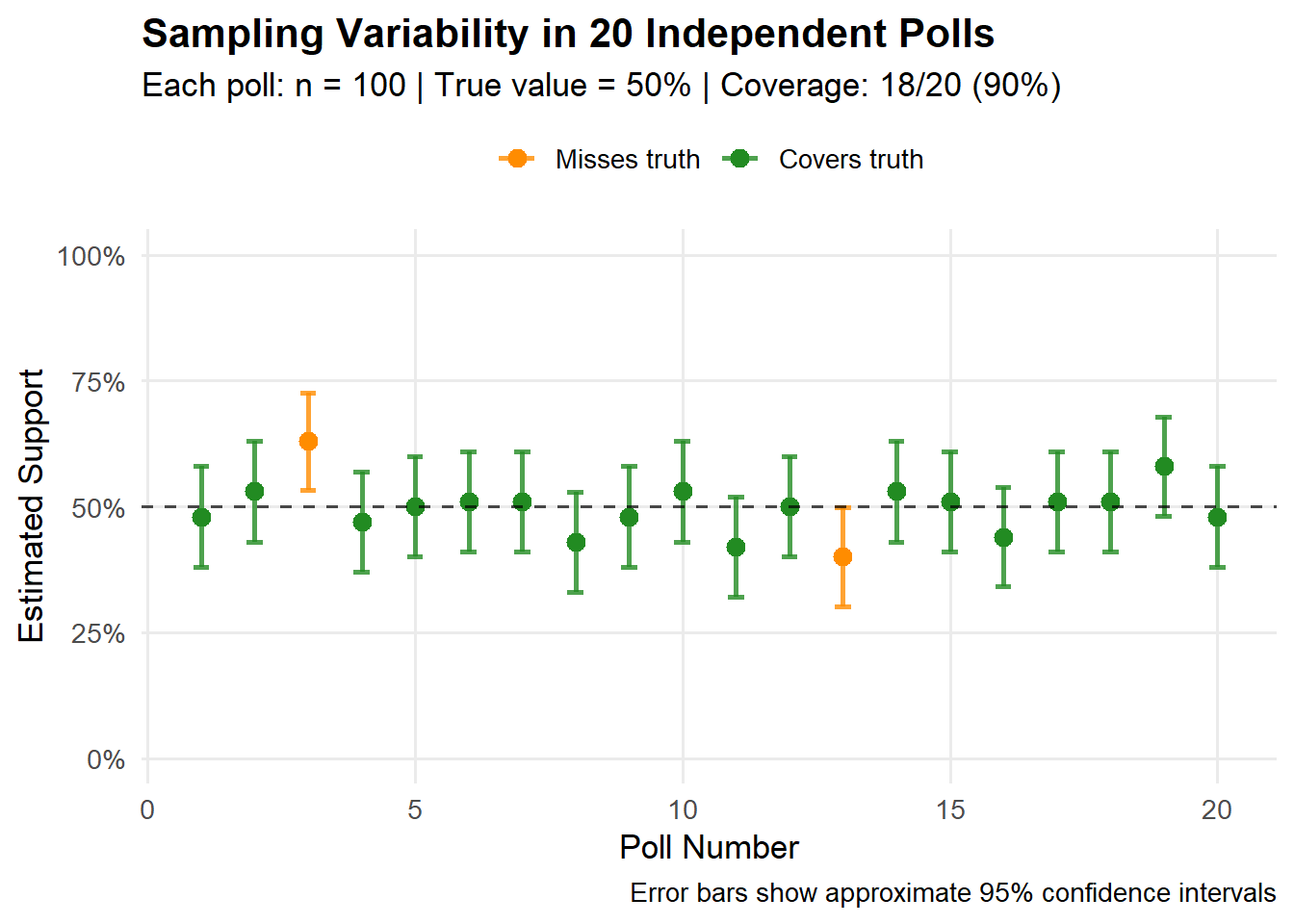

Opinion polls showing 52%, 49%, 51% support across different surveys—each random sample gives slightly different results, but they cluster around the true value

Random error is measured by variance—the average squared deviation of observations from their mean. It quantifies how much your data points (predictions) scatter.

Random error is like asking 5 friends to estimate how many jellybeans are in a jar—they’ll all give different answers just due to chance, but those differences scatter randomly around the truth rather than all being wrong in the same direction.

Polling example: Bias is like polling only at the gym at 6am—you’ll always get more health-conscious, early-rising, employed people and always miss night-shift workers, people with young kids, etc. The poll is broken in a predictable way. Or: only counting responses from people who actually answer unknown phone calls—you’ll systematically miss everyone (especially younger people) who screens their calls.

Key difference: Averaging more observations reduces random error but never fixes bias. You can’t average your way out of a miscalibrated scale—or a biased sampling method!

Two Approaches to the Same Data

Imagine you survey 100 random students and find that 60 support the 24/7 library hours.

❌ Without Statistical Thinking

“60 out of 100 students said yes.”

Conclusion: “Exactly 60% of all students support it.”

Decision: “Since it’s over 50%, we have clear majority support.”

Problem: Ignores that a different sample might give 55% or 65%

✅ With Statistical Thinking

“60 out of 100 students said yes.”

Conclusion: “We estimate 60% support, with a margin of error of ±10 pp.”

Decision: “True support is likely between 50% and 70%—we need more data to be certain of majority support.”

Advantage: Acknowledges uncertainty and informs better decisions

How sample size affects precision:

Sample Size

Observed Result

Margin of Error

(95%) Range of Plausible Values

Interpretation

n = 100

60%

±10 pp

50% to 70%

Uncertain about majority

n = 400

60%

±5 pp

55% to 65%

Likely majority support

n = 1,000

60%

±3 pp

57% to 63%

Clear majority support

n = 1,600

60%

±2.5 pp

57.5% to 62.5%

Strong majority support

n = 10,000

60%

±1 pp

59% to 61%

Very precise estimate

The Diminishing Returns Principle: Notice that quadrupling the sample size from 100 to 400 cuts the margin of error in half, but increasing from 1,600 to 10,000 (a 6.25× increase) only reduces it by 1.5 percentage points. To halve your margin of error, you must quadruple your sample size.

This is why most polls stop around 1,000–1,500 respondents—the gains in precision beyond that point rarely justify the additional cost and effort.

Sample Size and Uncertainty (Random Error)

Suppose we take a random sample of n=1000 voters and observe \hat p = 0.55 (e.g., 55% support for a candidate in upcoming elections—550 out of 1,000 respondents). Then:

Our best single-number estimate (point estimate) of the population proportion is \hat p = 0.55.

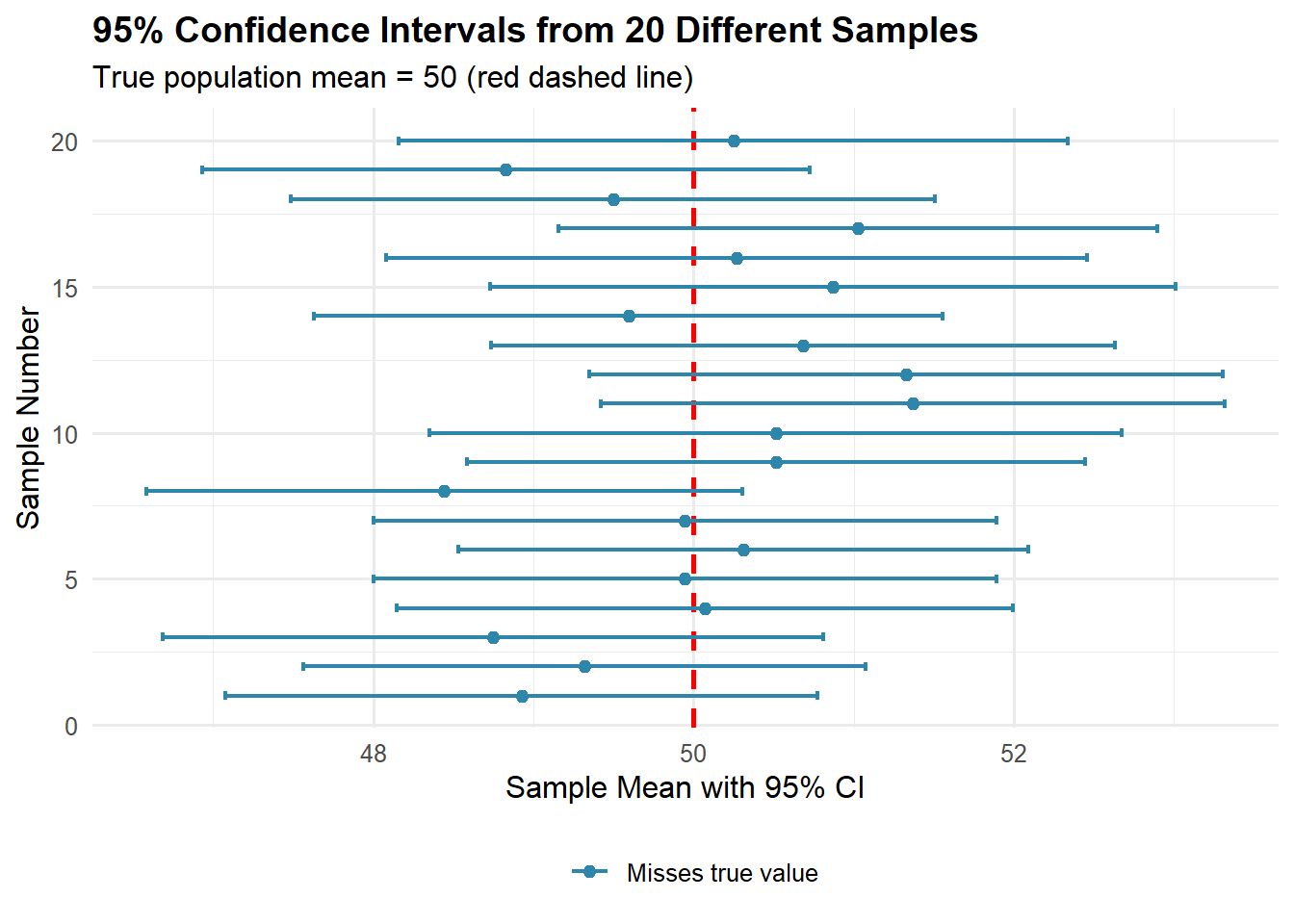

A typical “range of plausible values” (at the 95\% confidence level) around \hat p can be approximated by \hat p \pm \text{Margin of Error}, i.e.,

\hat p \;\pm\; 2\sqrt{\frac{\hat p(1-\hat p)}{n}}

\;=\;

0.55 \;\pm\; 2\sqrt{\frac{0.55\cdot 0.45}{1000}}

\approx

0.55 \pm 0.031,

giving roughly (interval estimate) 52\% to 58\% (approximately \pm 3.1 percentage points).

Note: The factor of 2 is a convenient rounding of 1.96, the critical value from the standard normal distribution for 95% confidence.

The width of this interval shrinks predictably with sample size:

\text{Margin of Error} \;\propto\; \frac{1}{\sqrt{n}}.

For example, increasing n from 1,000 to 4,000 cuts the margin of error approximately in half (from \pm 3.1\% to \pm 1.6\%).

Note

Fundamental Principle: Statistics does not eliminate uncertainty—it helps us measure, manage, and communicate it effectively.

Historical Example: the 1936 Literary Digest Poll

In 1936, Literary Digest ran one of the largest opinion polls ever — about 2.4 million mailed responses — yet it completely misjudged the U.S. presidential election.

Candidate

Prediction

Actual result

Error

Landon

57%

36.5%

≈20 pp

Roosevelt

43%

60.8%

≈18 pp

What went wrong?

Even with millions of responses, the poll was badly biased — not random, but systematic.

Systematic vs. Random Error

Imagine a bathroom scale that adds +2.3 kg to everyone’s weight:

Random error (no bias): Each time you step on, your balance shifts a little. Readings jump around your true weight — say 68.0–68.5 kg. Averaging them gives the right result (≈68 kg). More readings reduce the scatter.

Systematic error (bias): The scale’s zero point is wrong. Every reading shows +2.3 kg too much. Weigh yourself once: 70.3 kg. Weigh yourself 1,000 times: still ~70.3 kg — precisely wrong.

That was Literary Digest’s problem: a miscalibrated “instrument” for measuring public opinion. Millions of biased responses only produced false confidence.

Where did the bias come from?

Two biases both worked in favor of Alf Landon:

Coverage (selection) bias — who could be contacted

The poll used telephone books, car registration lists, and magazine subscribers.

During the Great Depression, these lists mostly included wealthier Americans, who leaned Republican.

Result: systematic underrepresentation of poorer, pro-Roosevelt voters.

Nonresponse bias — who chose to reply

Only about one in four people (≈24%) who were contacted returned their ballot.

Those who responded were more politically active and more likely to oppose Roosevelt.

Together, these created a huge systematic bias that no large sample could fix.

Why sample size couldn’t save the poll

Taking 2.4 million responses from a biased list is like weighing an entire country on a faulty scale.

The maximum possible (worst case scenario) margin of error (for the 95\% confidence level) for a given sample size (if it had been a true random sample) would have been: \text{MoE}_{95\%} \approx 1.96\sqrt{\frac{0.25}{2{,}400{,}000}} \approx \pm 0.06 \text{ percentage points} — tiny.

That formula only captures random error, not bias.

The real error was about ±18–20 percentage points — hundreds of times larger.

Lesson:Precision without representativeness is useless. A huge biased sample can be worse than a small, carefully chosen one.

Modern Polling: Smaller but Smarter

The Literary Digest disaster transformed polling practice:

Probability sampling: every voter has a known, non-zero chance of selection.

Weighting: adjust for groups that reply too often or too rarely.

Total survey error mindset: consider coverage, nonresponse, measurement, and processing errors — not just sampling error.

Bottom line:How you sample matters far more than how many you sample.

1.4 Understanding Randomness

A random experiment is any process whose result cannot be predicted with certainty, such as tossing a coin or rolling a die.

An outcome is a single possible result of that experiment—for example, getting “heads” or rolling a “5”.

Sample space is the set of all possible outcomes of a random experiment. It is typically denoted by the symbol S or Ω (omega).

An event is a set of one or more outcomes that we’re interested in; it could be a simple event (like rolling exactly a 3) or a compound event (like rolling an even number, which includes the outcomes 2, 4, and 6).

Probability is a way of measuring how likely something is to happen. It’s a number between 0 and 1 (or 0% and 100%) that represents the chance of an event occurring.

A probability distribution is a mathematical function/rule that describes the likelihood of different possible outcomes in a random experiment.

If something has a probability of 0, it’s impossible - it will never happen. If something has a probability of 1, it’s certain - it will definitely happen. Most things fall somewhere in between.

For example, when you flip a fair coin, there’s a 0.5 (or 50%) probability it will land on heads, because there are two equally likely outcomes and heads is one of them.

Probability helps us make sense of uncertainty and randomness in the world.

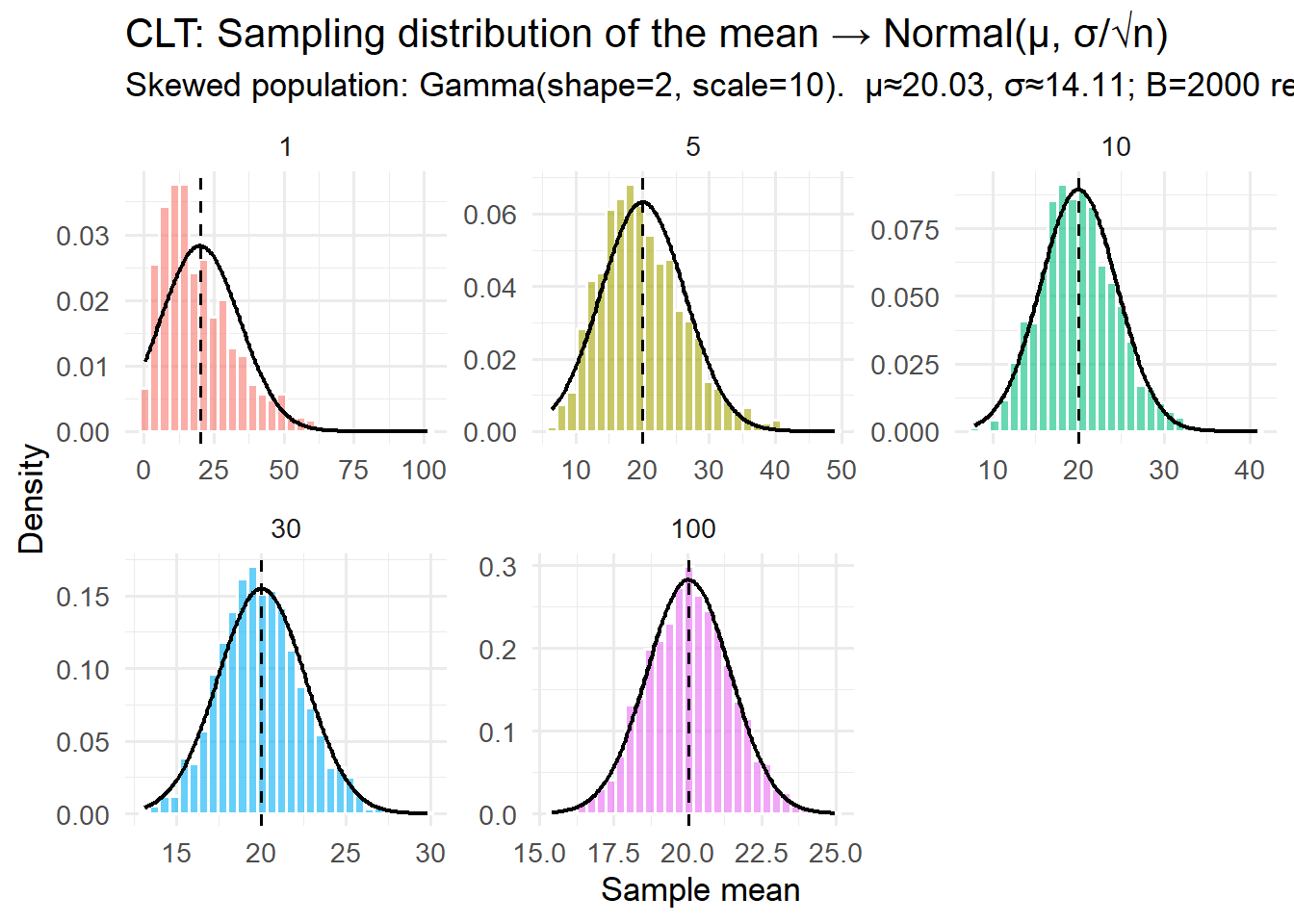

In statistics, randomness is an orderly way to describe uncertainty. While each individual outcome is unpredictable, stable patterns (more formally, empirical distributions of outcomes converge to probability distributions) emerge over many repetitions.

Example: Flip a fair coin:

Single flip: Completely unpredictable—you can’t know if it’ll be heads or tails

100 flips: You’ll get close to 50% heads (maybe 48 or 53)

10,000 flips: Almost certainly very close to 50% heads (perhaps 49.8%)

The same applies to dice: you can’t predict your next roll, but roll 600 times and each number (1-6) will appear close to 100 times. This predictable long-run behavior from unpredictable individual events is the essence of statistical randomness.

Types of Randomness

Epistemic vs. Ontological Randomness:

Epistemic randomness (due to incomplete knowledge): We treat an outcome as random because not all determinants are observed or conditions are not controlled. The system itself is deterministic—it follows fixed rules—but we lack the information needed to predict the outcome.

Coin toss: The trajectory of the coin is governed entirely by classical mechanics. If we knew the exact initial position, force, angular momentum, air resistance, and surface properties, we could theoretically predict whether it lands on heads or tails. The “randomness” exists only because we cannot measure these conditions with sufficient precision.

Poll responses: An individual’s answer to a survey question is determined by their beliefs, experiences, and context, but we don’t have access to this complete psychological state, so we model it as random.

Measurement error: Limited instrument precision means the “true” value exists, but we observe it with uncertainty.

Ontological randomness (intrinsic indeterminacy): Even complete knowledge of all conditions does not remove outcome uncertainty. The randomness is fundamental to the nature of reality itself, not just a gap in our knowledge.

Radioactive decay: The exact moment when a particular atom will decay is fundamentally unpredictable, even in principle. Quantum mechanics tells us only the probability distribution, not the precise timing.

Quantum measurements: The outcome of measuring a quantum particle’s position or spin is inherently probabilistic, not determined by hidden variables we simply haven’t discovered yet.

The Coin Toss Paradox

While we treat coin tosses as producing 50-50 random outcomes, research by mathematician Persi Diaconis has shown that with a mechanical coin-flipping machine that precisely controls initial conditions, you can reliably bias the outcome toward a chosen side. This confirms that coin tosses are epistemically, not ontologically, random—the apparent randomness comes from our inability to control and measure conditions, not from any fundamental indeterminacy in physics.

Related Concepts

Randomness vs. Haphazardness: Statistical randomness has mathematical structure and follows probability laws—it’s orderly uncertainty. Haphazardness suggests complete disorder without underlying patterns or rules.

Deterministic Chaos: The middle ground between perfect predictability and randomness. Chaos refers to deterministic systems (following fixed, known rules) that exhibit extreme sensitivity to initial conditions, making long-term prediction impossible in practice.

Think of chaos like a pinball machine, with the butterfly effect:

You know all the rules perfectly—the physics of collisions, friction, gravity

The system is completely deterministic: release the ball from exactly the same spot with exactly the same force, and you’ll get exactly the same result every time

But: A difference of 0.01 millimeters in starting position leads to the ball hitting different bumpers, which compounds with each collision until the final outcome is completely different

This is the butterfly effect: tiny perturbations in initial conditions grow exponentially over time

Classic examples of deterministic chaos:

Weather systems: Edward Lorenz discovered that atmospheric models are so sensitive that a butterfly flapping its wings in Brazil could theoretically alter whether a tornado forms in Texas weeks later. This is why weather forecasts are reliable for days but not months.

Planetary orbits: While stable on human timescales, the solar system’s dynamics are chaotic over millions of years. We cannot predict the exact position of planets in the distant future, even though we know the gravitational laws perfectly.

Double pendulum: Release it from a slightly different angle, and after a few swings, the motion becomes completely different.

Chaos vs. Epistemic Randomness—A Critical Distinction:

Both involve unpredictability due to limited knowledge, but they differ in a crucial way:

Aspect

Epistemic Randomness

Deterministic Chaos

Rules known?

Often yes

Yes, completely

Current state known?

No (or imprecisely)

No (or imprecisely)

What causes unpredictability?

Missing information about the current state

Exponential amplification of tiny measurement errors

Can perfect info help?

Yes—learning the state eliminates uncertainty

Only in the short term—errors accumulate again

Example to clarify:

Epistemic randomness (card face-down): The card is already the 7 of hearts. It’s not changing or evolving. You just don’t know which card it is yet. Flip it over, and the uncertainty vanishes completely and permanently.

Chaos (weather in 3 weeks): Even if you measure current atmospheric conditions to extraordinary precision, tiny errors (measurement at 6 decimal places instead of 20) compound over time. You might predict well for 5 days, but by week 3, your forecast is useless—not because you don’t know the physics, but because the system amplifies microscopic uncertainties.

Key Insight

Chaos is deterministic yet unpredictable. Epistemic randomness is deterministic yet unknown. Ontological randomness is fundamentally indeterministic. Statistical practice treats all three as “random,” but understanding the source of unpredictability helps us know when more information could help (epistemic), when it helps temporarily but not long-term (chaos), and when it cannot help at all (ontological).

Entropy: A measure of disorder or uncertainty in a system. High entropy means high unpredictability or many possible microstates; low entropy means high order and low uncertainty. In information theory and statistics, entropy quantifies the amount of uncertainty in a probability distribution—more spread out distributions have higher entropy.

1.5 Populations and Samples

Understanding the distinction between populations and samples is crucial for proper statistical analysis.

Population

A population is the complete set of individuals, objects, or measurements about which we wish to draw conclusions. The key word here is “complete”—a population includes every single member of the group we’re studying.

Examples of Populations in Demography:

All residents of India as of January 1, 2024: This includes every person living in India on that specific date—approximately 1.4 billion people.

All births in Sweden during 2023: Every baby born within Swedish borders during that calendar year—roughly 100,000 births.

All households in Tokyo: Every residential unit where people live, cook, and sleep separately from others—about 7 million households.

All deaths from COVID-19 worldwide in 2020: Every death where COVID-19 was listed as a cause—several million deaths.

Populations can be:

Finite: Having a countable number of members (all current U.S. citizens, all Polish municipalities in 2024)

Infinite: Theoretical or uncountably large (all possible future births, all possible coin tosses or dice flips)

Fixed: Defined at a specific point in time (all residents on census day)

Dynamic: Changing over time (the population of a city that experiences births, deaths, and migration daily)

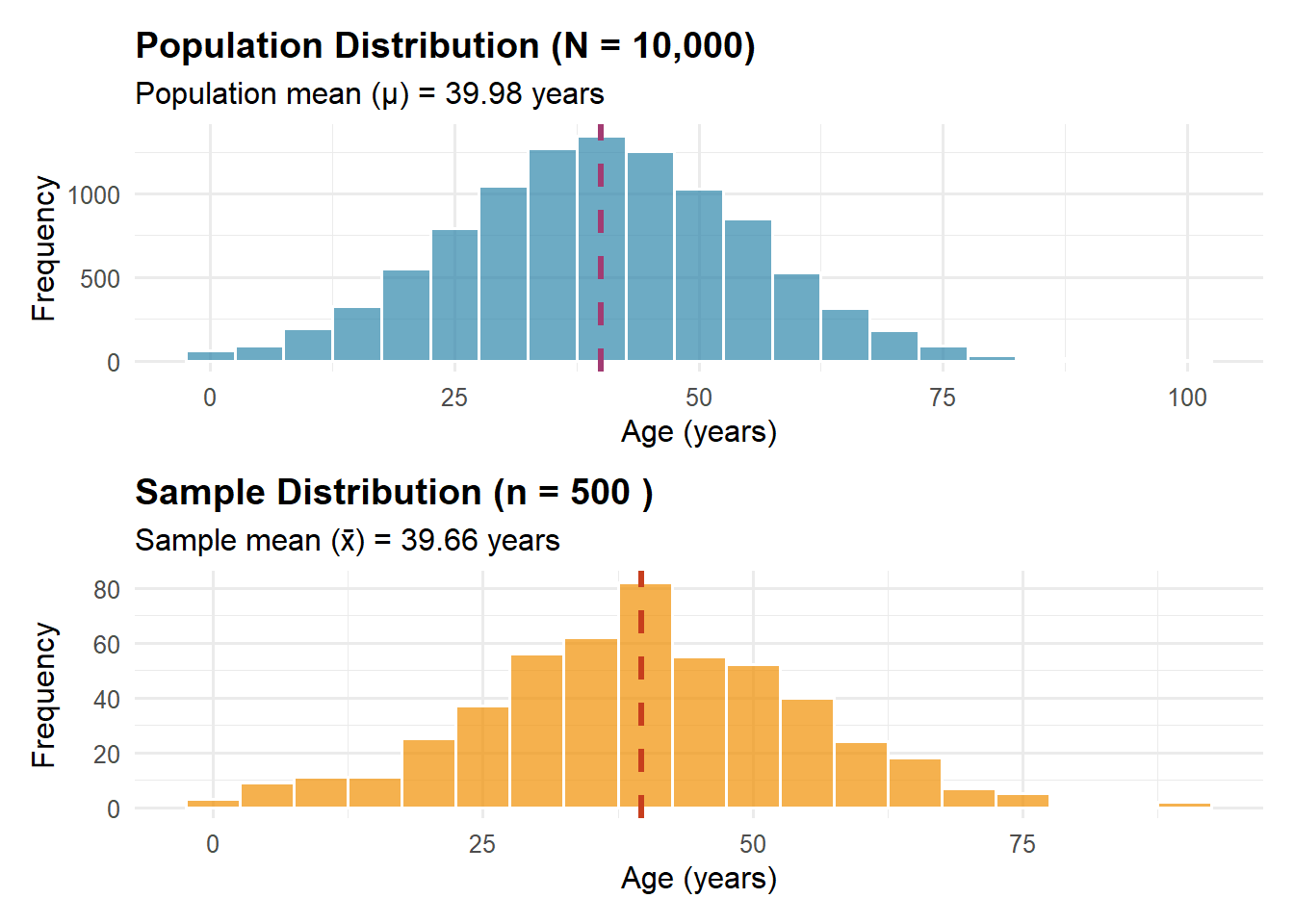

Sample

A sample is a subset of the population that is actually observed or measured. We study samples because examining entire populations is often impossible, impractical, or unnecessary.

Why We Use Samples:

Practical Impossibility: Imagine testing every person in China for a disease. By the time you finished testing 1.4 billion people, the disease situation would have changed completely, and some people tested early would need retesting.

Cost Considerations: The 2020 U.S. Census cost approximately $16 billion. Conducting such complete enumerations frequently would be prohibitively expensive. A well-designed sample survey can provide accurate estimates at a fraction of the cost.

Time Constraints: Policy makers often need information quickly. A sample survey of 10,000 people can be completed in weeks, while a census takes years to plan, execute, and process.

Destructive Measurement: Some measurements destroy what’s being measured. Testing the lifespan of light bulbs or the breaking point of materials requires using samples.

Greater Accuracy: Surprisingly, samples can sometimes be more accurate than complete enumerations. With a sample, you can afford better training for interviewers, more careful data collection, and more thorough quality checks.

Example of Sample vs. Population:

Let’s say we want to know the average household size in New York City:

Population: All 3.2 million households in NYC

Census approach: Attempt to contact every household (expensive, time-consuming, some will be missed)

Sample approach: Randomly select 5,000 households, carefully measure their sizes, and use this to estimate the average for all households

Result: The sample might find an average of 2.43 people per household with a margin of error of ±0.05, meaning we’re confident the true population average is between 2.38 and 2.48

Overview of Sampling Methods

Sampling involves selecting a subset of the population to estimate its characteristics. The sampling frame (list from which we sample) should ideally contain each member exactly once. Frame problems: undercoverage, overcoverage, duplication, and clustering.

Probability Sampling (Statistical Inference Possible)

Simple Random Sampling (SRS): Every possible sample of size n has equal probability of selection (sampling without replacement). Gold standard of probability methods.

Formal definition: Each of the \binom{N}{n} possible samples has probability \frac{1}{\binom{N}{n}}.

Inclusion probability for a unit:

Question: In how many samples does a specific person (e.g., student John) appear?

If John is already in the sample (that’s fixed), we need to select n-1 more people from the remaining N-1 people (everyone except John).

Number of samples containing John: \binom{N-1}{n-1}

Probability:

P(\text{John in sample}) = \frac{\text{samples with John}}{\text{all samples}} = \frac{\binom{N-1}{n-1}}{\binom{N}{n}} = \frac{n}{N}

Numerical example: N=5 people {A,B,C,D,E}, we sample n=3. All samples: \binom{5}{3}=10. Samples with person A: {ABC, ABD, ABE, ACD, ACE, ADE} = \binom{4}{2}=6 samples. Probability: 6/10 = 3/5 = n/N ✓

Systematic Sampling: Selection of every k-th element, where k = N/n. Simple to implement, but beware of hidden periodicity in the frame (e.g., list ordered by patterns).

Systematic Sampling: Selection of every k-th element, where k = N/n (sampling interval).

How it works: Randomly select a starting point r from \{1, 2, ..., k\}, then select: r, r+k, r+2k, r+3k, ...

Example: N=1000, n=100, so k=10. If r=7, we select: 7, 17, 27, 37, …, 997.

Advantages: Very simple, ensures even coverage of the population.

Periodicity problem: If the list has a pattern repeating every k elements, the sample can be severely biased.

Example (bad): Apartment list: 101, 102, 103, 104 (corner), 201, 202, 203, 204 (corner), … If k=4, we might sample only corner apartments!

Example (bad): Daily production data with 7-day cycle. If k=7, we might sample only Mondays.

Example (good): Alphabetical list of surnames - usually no periodicity.

Cluster Sampling: Selection of entire groups (clusters) instead of individual units. Cost-effective for geographically dispersed populations (e.g., sampling schools instead of students), but typically less precise than SRS (design effect: DEFF = Variance(cluster)/Variance(SRS)). Can be single- or multi-stage.

Convenience Sampling: Selection based on ease of access (e.g., passersby in city center). Useful in pilot/exploratory studies, but likely serious selection bias.

Purposive/Judgmental Sampling: Deliberate selection of typical, extreme, or information-rich cases. Valuable in qualitative research and studying rare populations.

Quota Sampling: Matching population proportions (e.g., 50% women), but without random selection. Quick and inexpensive, but hidden selection bias and no ability to calculate sampling error.

Snowball Sampling: Participants recruit others from their networks. Essential for hard-to-reach populations (drug users, undocumented immigrants), but biased toward well-connected individuals.

Fundamental Principle: Probability sampling enables valid statistical inference and calculation of sampling error; non-probability methods may be necessary for practical or ethical reasons, but limit the ability to generalize results to the entire population.

1.6 Superpopulation and Data Generating Process (DGP) (*)

Superpopulation

A superpopulation is a theoretical infinite population from which your finite population is considered to be one random sample.

Think of it in three levels:

Superpopulation: An infinite collection of possible values (theoretical)

Finite population: The actual population you could theoretically census (e.g., all 50 US states, all 10,000 firms in an industry)

Sample: The subset you actually observe (e.g., 30 states, 500 firms)

Why do we need this concept?

Consider the 50 US states. You might measure unemployment rate for all 50 states—a complete census, no sampling needed. But you still want to:

Test if unemployment is related to education levels

Predict next year’s unemployment rates

Determine if differences between states are “statistically significant”

Without the superpopulation concept, you’re stuck—you have all the data, so what’s left to infer? The answer: treat this year’s 50 values as one draw from an infinite superpopulation of possible values that could occur under similar conditions.

Mathematical representation:

Finite population value: Y_i (state i’s unemployment rate)

Your model is simpler than reality. You’re missing variables (sleep, stress, breakfast), so your estimates might be biased. The u_i term captures everything you missed.

Key insight: We never know the true DGP. Our statistical models are always approximations, trying to capture the most important parts of the unknown, complex truth.

Two Approaches to Statistical Inference

When analyzing data, especially from surveys or samples, we can take two philosophical approaches:

1. Design-Based Inference

Philosophy: The population values are fixed numbers. Randomness comes ONLY from which units we happened to sample.

Focus: How we selected the sample (simple random, stratified, cluster sampling, etc.)

Example: The mean income of California counties is a fixed number. We sample 10 counties. Our uncertainty comes from which 10 we randomly selected.

No models needed: We don’t assume anything about the population values’ distribution

2. Model-Based Inference

Philosophy: The population values themselves are realizations from some probability model (superpopulation)

Focus: The statistical model generating the population values

Example: Each California county’s income is drawn from: Y_i = \mu + \epsilon_i where \epsilon_i \sim N(0, \sigma^2)

Models required: We make assumptions about how the data were generated

Which is better?

Large populations, good random samples: Design-based works well

Small populations (like 50 states): Model-based often necessary

Complete enumeration: Only model-based allows inference

Modern practice: Often combines both approaches

Practical Example: Analyzing State Education Spending

Suppose you collect education spending per pupil for all 50 US states.

Without superpopulation thinking:

You have all 50 values—that’s it

The mean is the mean, no uncertainty

You can’t test hypotheses or make predictions

With superpopulation thinking:

This year’s 50 values are one realization from a superpopulation

Test if spending relates to state income (\beta \neq 0?)

Predict next year’s values

Calculate confidence intervals

The key insight: Even with complete data, the superpopulation framework enables statistical inference by treating observed values as one possible outcome from an underlying stochastic process.

Summary

Superpopulation: Treats your finite population as one draw from an infinite possibility space—essential when your finite population is small or completely observed

DGP: The true (unknown) process creating your data—your models try to approximate it

1.7 Understanding Data, Data Distributions, and Data Typologies

What is Data?

Data is a collection of facts, observations, or measurements that we gather to answer questions or understand phenomena. In statistics and data analysis, data represents information in a structured format that can be analyzed.

Data Points

A data point is a single observation or measurement in a dataset. For example, if we measure the height of 5 students, each individual height measurement is a data point.

Variables

A variable is a characteristic or attribute that can take different values across observations. Variables can be:

Categorical (e.g., color, gender, country)

Numerical (e.g., age, temperature, income)

Data Distribution

Data distribution describes what values a variable takes and how often each value occurs in the dataset. Understanding distribution helps us see patterns, central tendencies, and variability in our data.

Frequency Distribution Tables

A frequency distribution table organizes data by showing each unique value (or range of values) and the number of times it appears:

Value

Frequency

Relative Frequency

A

15

0.30 (30%)

B

25

0.50 (50%)

C

10

0.20 (20%)

Total

50

1.00 (100%)

This table allows us to quickly see which values are most common and understand the overall distribution pattern.

Understanding Different Types of Data Structures (Data Sets) and Their Formats

Cross-sectional Data

Observations for variables (columns in a database) collected at a single point in time across multiple entities/individuals:

Individual

Age

Income

Education

1

25

50000

Bachelor’s

2

35

75000

Master’s

3

45

90000

PhD

Time Series Data

Observations of a single entity tracked over multiple time points:

Year

GDP (in billions)

Unemployment Rate

2018

20,580

3.9%

2019

21,433

3.7%

2020

20,933

8.1%

Panel Data (Longitudinal Data)

Observations of multiple entities tracked over time:

Country

Year

GDP per capita

Life Expectancy

USA

2018

62,794

78.7

USA

2019

65,118

78.8

Canada

2018

46,194

81.9

Canada

2019

46,194

82.0

Time-series Cross-sectional (TSCS) Data

A special case of panel data where:

Number of time points > Number of entities

Similar structure to panel data but with emphasis on temporal depth

Common in political science and economics research

Data Formats

Wide Format

Each row represents an entity; columns represent variables/time points:

Country

GDP_2018

GDP_2019

LE_2018

LE_2019

USA

62,794

65,118

78.7

78.8

Canada

46,194

46,194

81.9

82.0

Long Format

Each row represents a unique entity-time-variable combination:

Country

Year

Variable

Value

USA

2018

GDP per capita

62,794

USA

2019

GDP per capita

65,118

USA

2018

Life Expectancy

78.7

USA

2019

Life Expectancy

78.8

Canada

2018

GDP per capita

46,194

Canada

2019

GDP per capita

46,194

Canada

2018

Life Expectancy

81.9

Canada

2019

Life Expectancy

82.0

Note: Long format is generally preferred for:

Data manipulation in R and Python

Statistical analysis

Data visualization

Understanding data types and distributions is fundamental to choosing appropriate analyses and interpreting results correctly.

Types of Data

Data consists of collected observations or measurements. The type of data determines what mathematical operations (e.g. multiplication) are meaningful and what statistical methods apply.

Quantitative Data

Continuous Data can take any value within a range:

Examples:

Age: Can be 25.5 years, 25.51 years, 25.514 years (precision limited only by measurement)

Body Mass Index: 23.7 kg/m²

Fertility Rate: 1.73 children per woman

Population Density: 4,521.3 people per km²

Voter turnout: 60%

Properties:

Can perform all arithmetic operations

Can calculate means, standard deviations

Discrete Data can only take specific values:

Examples:

Number of Children: 0, 1, 2, 3… (can’t have 2.5 children)

Number of Marriages: 0, 1, 2, 3…

Household Size: 1, 2, 3, 4… people

Number of Doctor Visits: 0, 1, 2, 3… per year

Electoral District Magnitude: 1, 2, 3, …

Qualitative/Categorical Data

Nominal Data represents categories with no inherent order:

The Challenge: Intervals between categories aren’t necessarily equal. The “distance” from Poor to Fair health may not equal the distance from Good to Excellent.

Frequency, Relative Frequency, and Density

When we analyze data, we’re often interested in how many times each value (or range of values) appears. This leads us to three related concepts:

(Absolute) Frequency is simply the count of how many times a particular value or category occurs in your data. If 15 students scored between 70-80 points on an exam, the frequency for that range is 15.

Relative frequency expresses frequency as a proportion or percentage of the total. It answers the question: “What fraction of all observations fall into this category?” Relative frequency is calculated as:

\text{Relative Frequency} = \frac{\text{Frequency}}{\text{Total Number of Observations}}

If 15 out of 100 students scored 70-80 points, the relative frequency is 15/100 = 0.15 or 15%. Relative frequencies always sum to 1 (or 100%), making them useful for comparing distributions with different sample sizes.

Tip

The probability of an event is a number between 0 and 1; the larger the probability, the more likely an event is to occur.

Density (probability per unit length) measures how concentrated observations are per unit of measurement. When grouping continuous data (like time or unemployment rate) into intervals of different widths, we need density to ensure fair comparison—wider intervals naturally contain more observations simply because they’re wider, not because values are more concentrated there. Density is calculated as:

This standardization allows fair comparison between intervals—wider intervals don’t appear artificially more important just because they’re wider.

Density is particularly important for continuous variables because it ensures that the total area under the distribution equals 1, which allows us to interpret areas as probabilities.

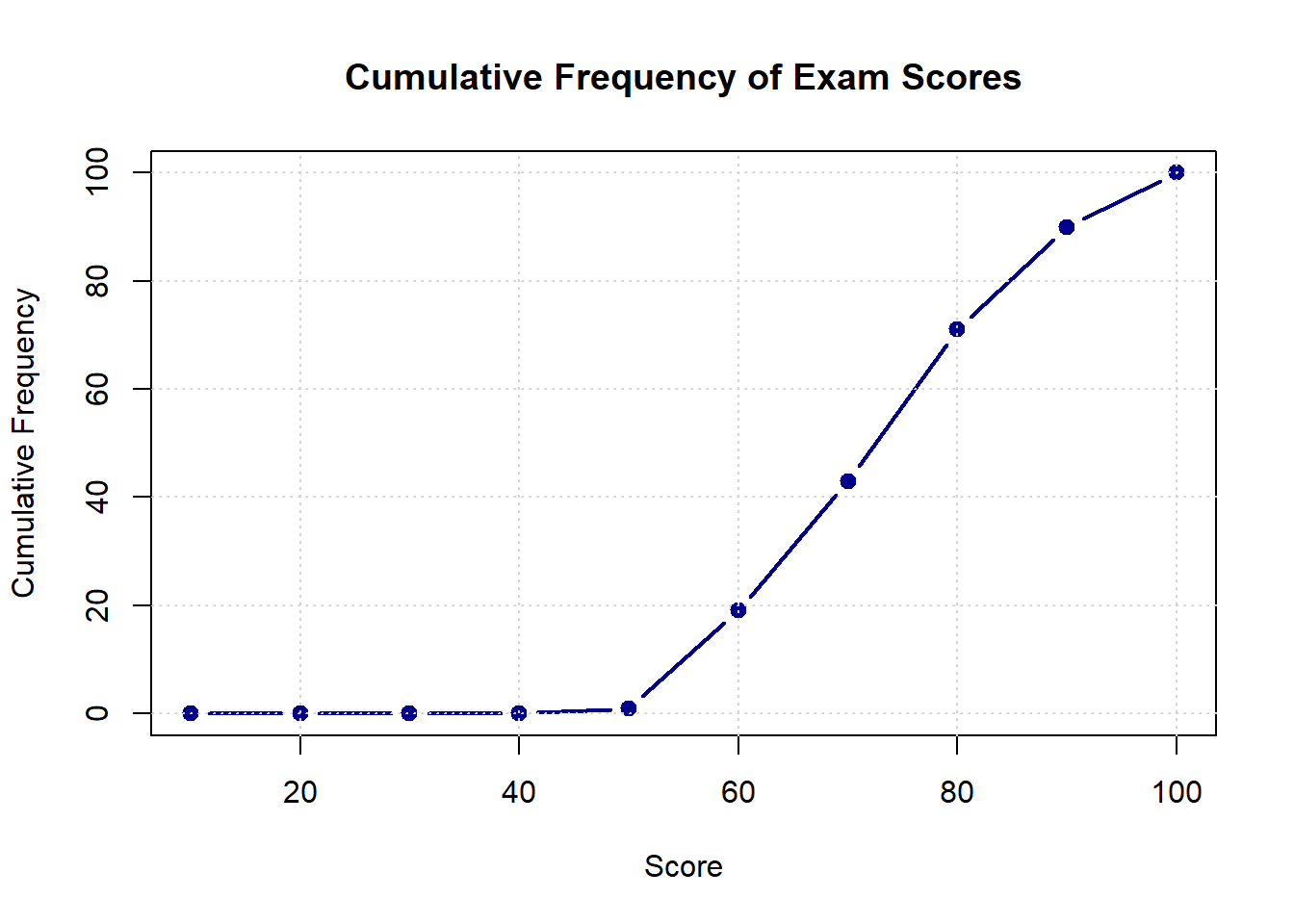

Cumulative frequency tells us how many observations fall at or below a certain value.

Instead of asking “how many observations are in this category?”, cumulative frequency answers “how many observations are in this category or any category below it?” It’s calculated by adding up all frequencies from the lowest value up to and including the current value.

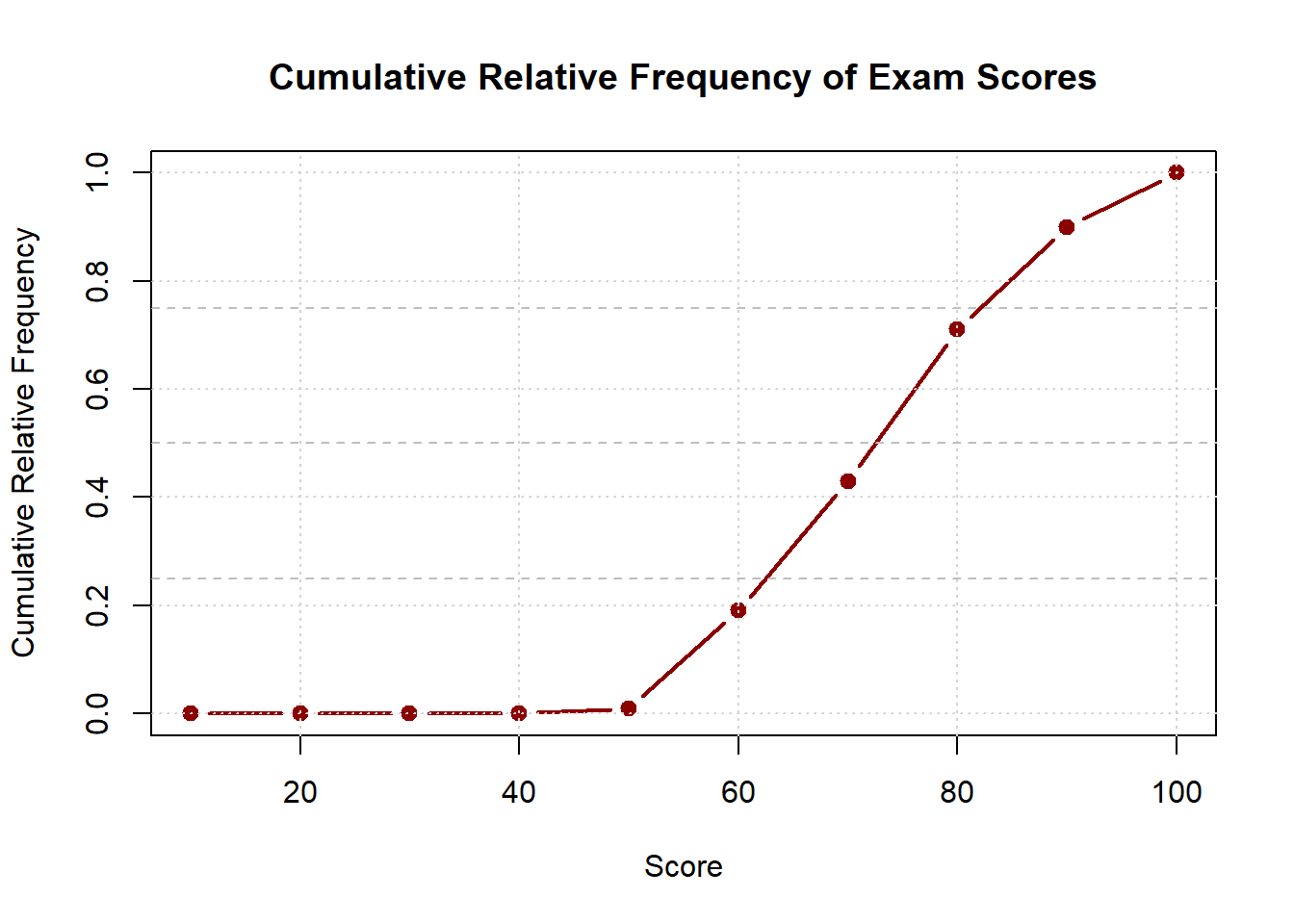

Similarly, cumulative relative frequency expresses this as a proportion of the total, answering “what percentage of observations fall at or below this value?” For example, if the cumulative relative frequency at score 70 is 0.40, this means 40% of students scored 70 or below.

Distribution Tables

A frequency distribution table organizes data by showing how observations are distributed across different values or intervals. Here’s an example with exam scores:

Score Range

Frequency

Relative Frequency

Cumulative Frequency

Cumulative Relative Frequency

Density

0-50

10

0.10

10

0.10

0.002

50-70

30

0.30

40

0.40

0.015

70-90

45

0.45

85

0.85

0.0225

90-100

15

0.15

100

1.00

0.015

Total

100

1.00

-

-

-

This table reveals that most students scored in the 70-90 range, while very few scored below 50 or above 90. The cumulative columns show us that 40% of students scored below 70, and 85% scored below 90. Such tables are invaluable for getting a quick overview of your data before conducting more complex analyses.

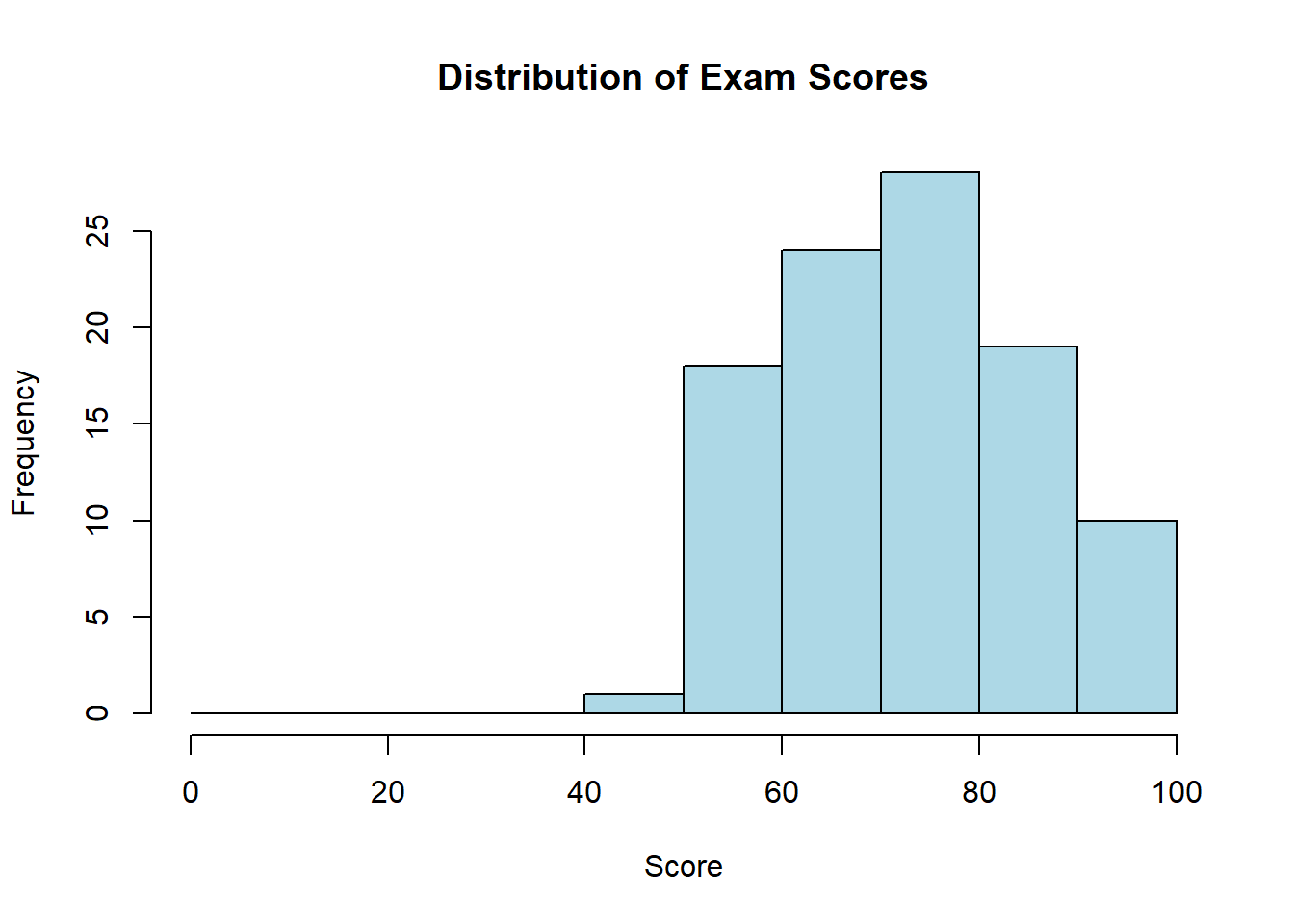

Visualizing Distributions: Histograms

A histogram is a graphical representation of a frequency distribution. It displays data using bars where:

The x-axis shows the values or intervals (bins)

The y-axis can show frequency, relative frequency, or density

The height of each bar represents the count, proportion, or density for that interval

Bars touch each other (no gaps) for continuous variables

Choosing bin widths: The number and width of bins significantly affects how your histogram looks. Too few bins hide important patterns, while too many bins create “noise” and make patterns hard to see.

In statistics, noise is unwanted random variation that obscures the pattern we’re trying to find. Think of it like static on a radio—it makes the music (the “signal”) harder to hear. In data, noise comes from measurement errors, random fluctuations, or the inherent variability in what we’re studying. Noise is random variation in data that hides the real patterns we want to see, similar to how background noise makes conversation difficult to hear.

Several approaches help determine appropriate bin widths (*):

Sturges’ rule: Use k = 1 + \log_2(n) bins, where n is the sample size. This works well for roughly symmetric distributions.

Square root rule: Use k = \sqrt{n} bins. A simple, reasonable default for many situations.

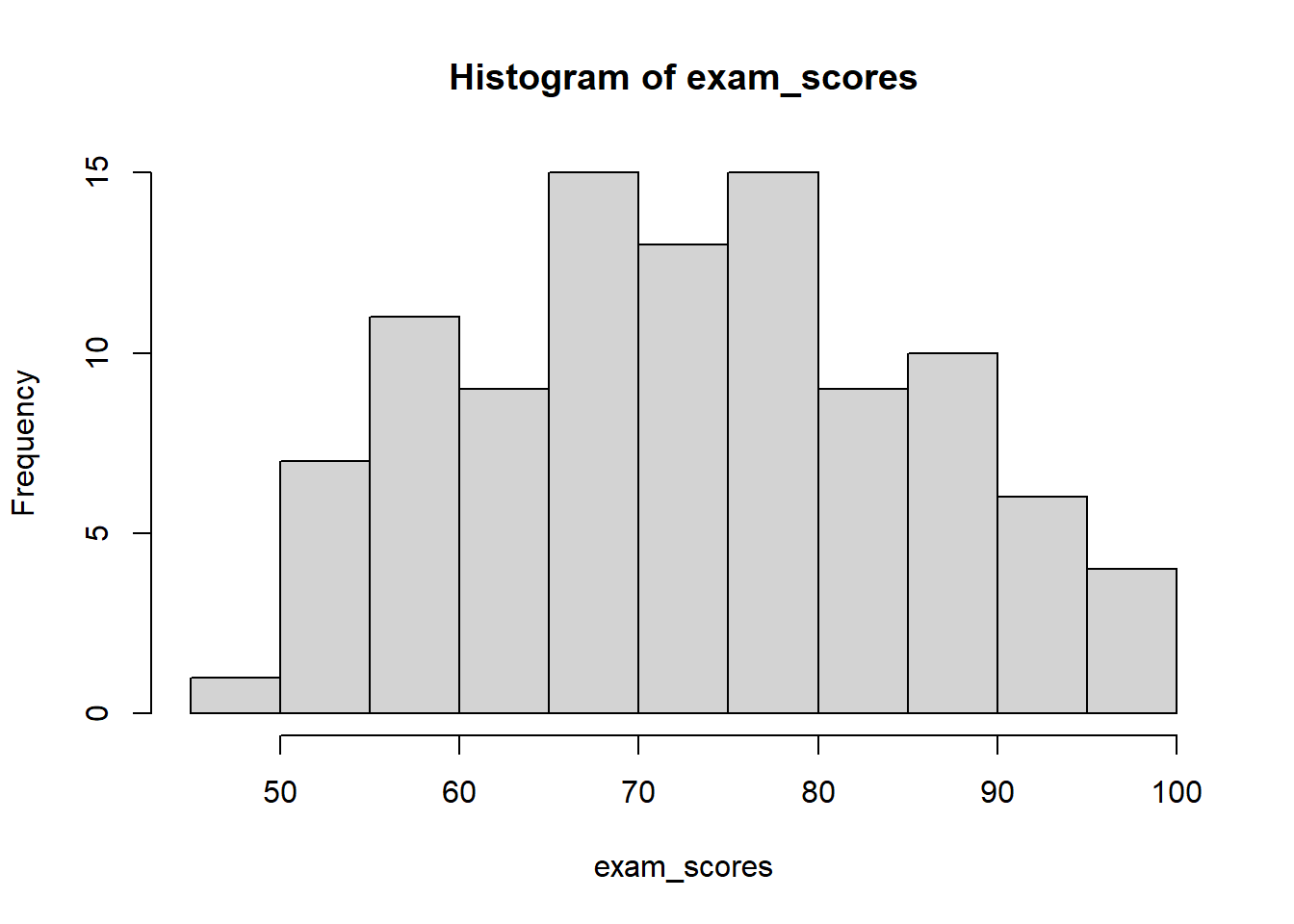

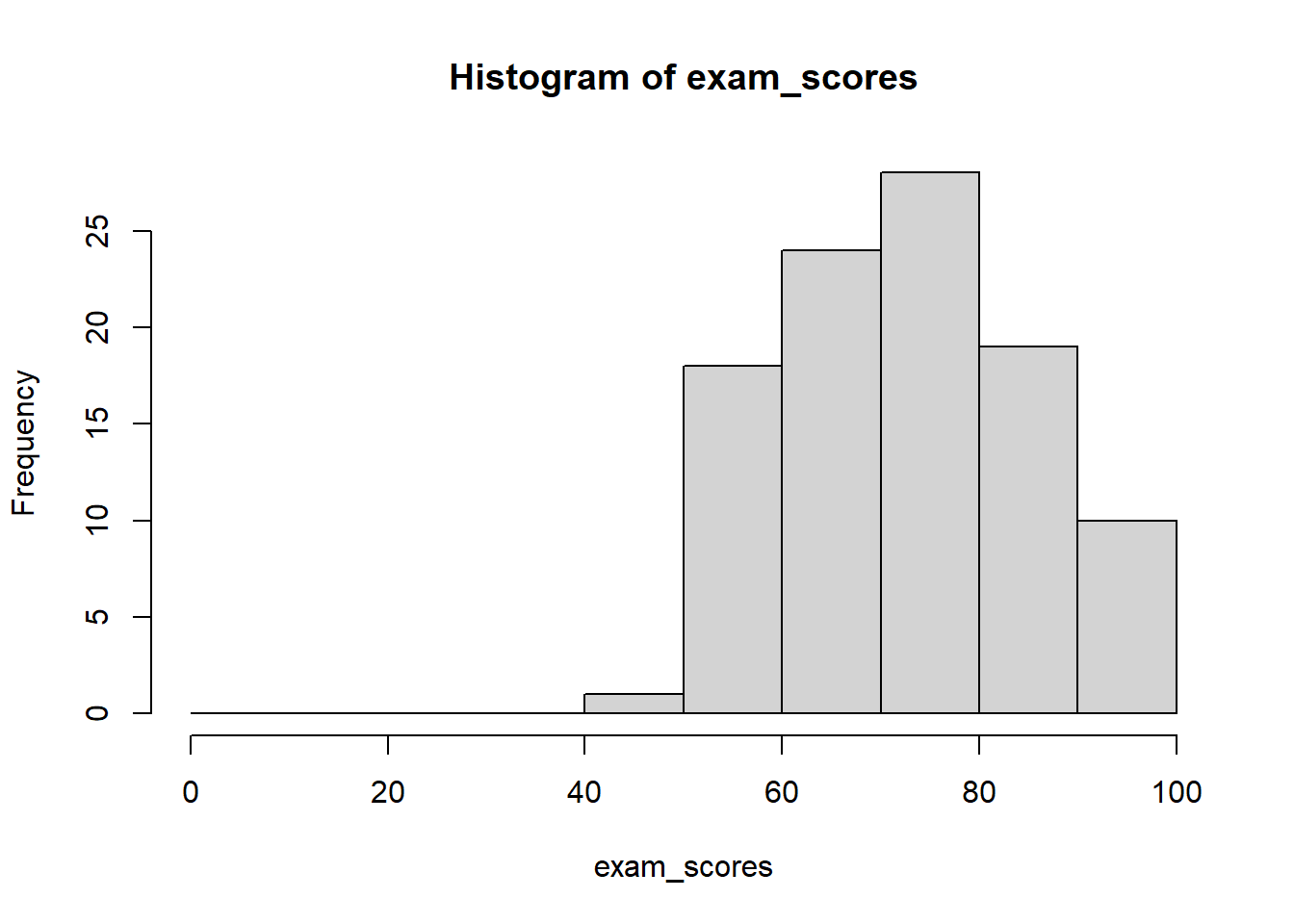

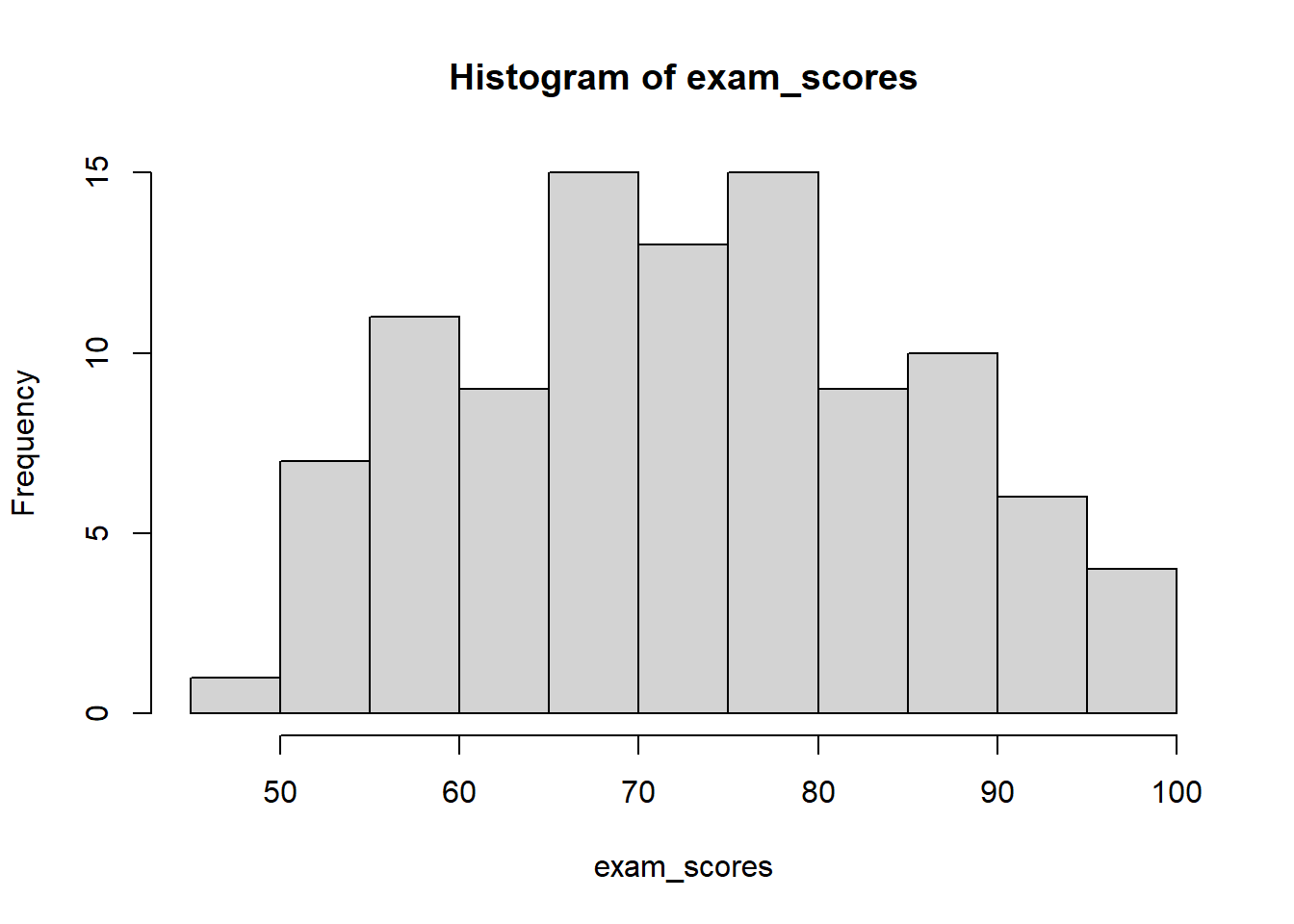

In R, you can specify bins in several ways:

# Generate exam scores dataset.seed(123) # For reproducibilityexam_scores <-c(rnorm(80, mean =75, sd =12), # Most students cluster around 75runif(15, 50, 65), # Some lower performersrunif(5, 85, 95) # A few high achievers)# Keep scores within valid range (0-100)exam_scores <-pmin(pmax(exam_scores, 0), 100)# Round to whole numbersexam_scores <-round(exam_scores)# Specify number of binshist(exam_scores, breaks =10)

# Specify exact break pointshist(exam_scores, breaks =seq(0, 100, by =10))

# Let R choose automatically (uses Sturges' rule by default)hist(exam_scores)

The best approach is often to experiment with different bin widths to find what best reveals your data’s pattern. Start with a default, then try fewer and more bins to see how the story changes.

Defining bin boundaries: When creating bins for a frequency table, you must decide how to handle values that fall exactly on the boundaries. For example, if you have bins 0-10 and 10-20, which bin does the value 10 belong to?

The solution is to use interval notation to specify whether each boundary is included or excluded:

Closed interval[a, b] includes both endpoints: a \leq x \leq b

Open interval(a, b) excludes both endpoints: a < x < b

Half-open interval[a, b) includes the left endpoint but excludes the right: a \leq x < b

Half-open interval(a, b] excludes the left endpoint but includes the right: a < x \leq b

Standard convention: Most statistical software, including R, uses left-closed, right-open intervals[a, b) for all bins except the last one, which is fully closed [a, b]. This means:

The value at the lower boundary is included in the bin

The value at the upper boundary belongs to the next bin

The very last bin includes both boundaries to capture the maximum value

For example, with bins 0-20, 20-40, 40-60, 60-80, 80-100:

Score Range

Interval Notation

Values Included

0-20

[0, 20)

0 ≤ score < 20

20-40

[20, 40)

20 ≤ score < 40

40-60

[40, 60)

40 ≤ score < 60

60-80

[60, 80)

60 ≤ score < 80

80-100

[80, 100]

80 ≤ score ≤ 100

This convention ensures that:

Every value is counted exactly once (no double-counting)

No values fall through the cracks

The bins partition the entire range completely

When presenting frequency tables in reports, you can simply write “0-20, 20-40, …” and note that bins are left-closed, right-open, or explicitly show the interval notation if precision is important.

Frequency histogram shows the raw counts:

# R code examplehist(exam_scores, breaks =seq(0, 100, by =10),main ="Distribution of Exam Scores",xlab ="Score",ylab ="Frequency",col ="lightblue")

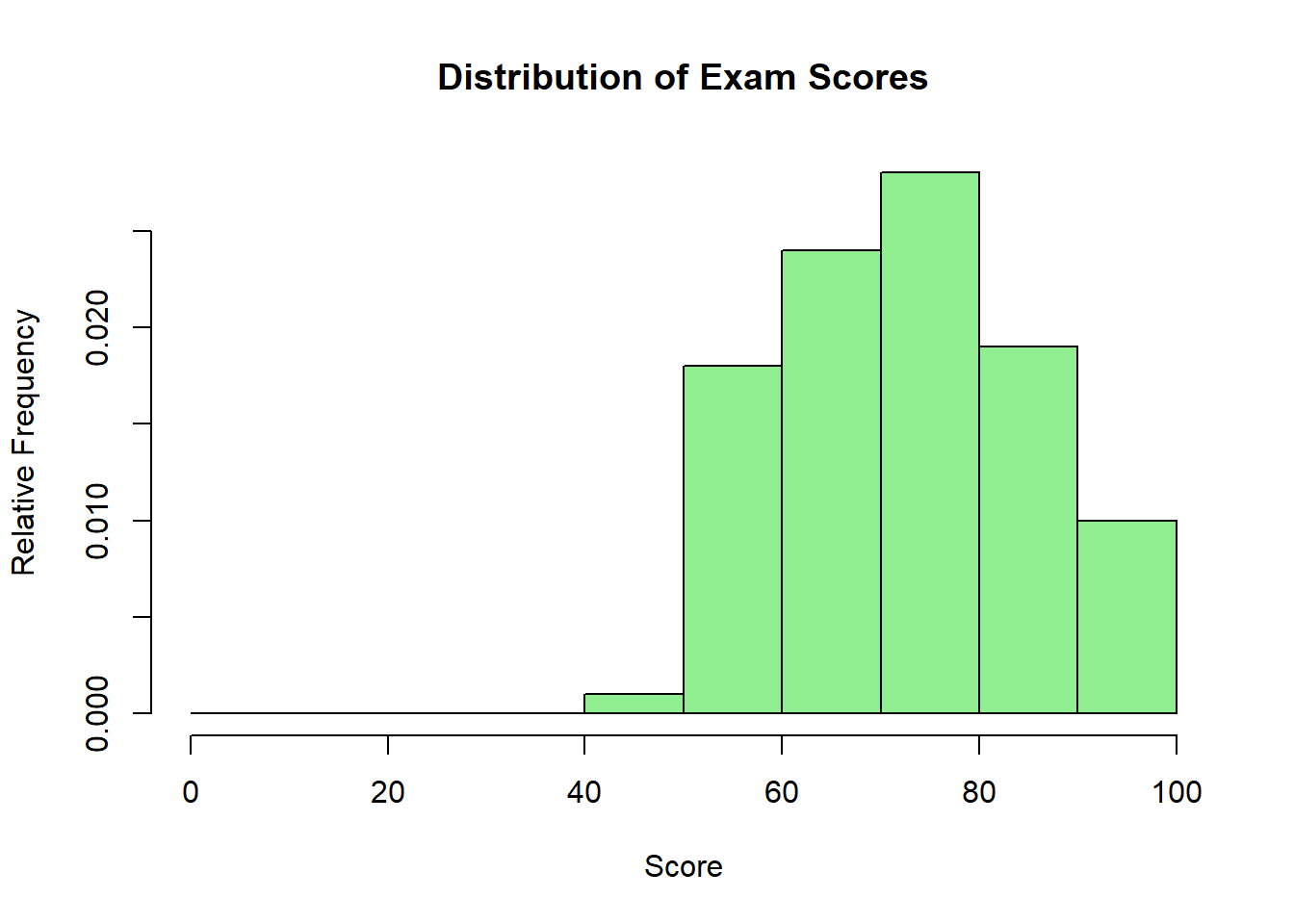

Relative frequency histogram shows proportions (useful when comparing groups of different sizes):

hist(exam_scores, breaks =seq(0, 100, by =10),freq =FALSE, # This creates relative frequency/densitymain ="Distribution of Exam Scores",xlab ="Score",ylab ="Relative Frequency",col ="lightgreen")

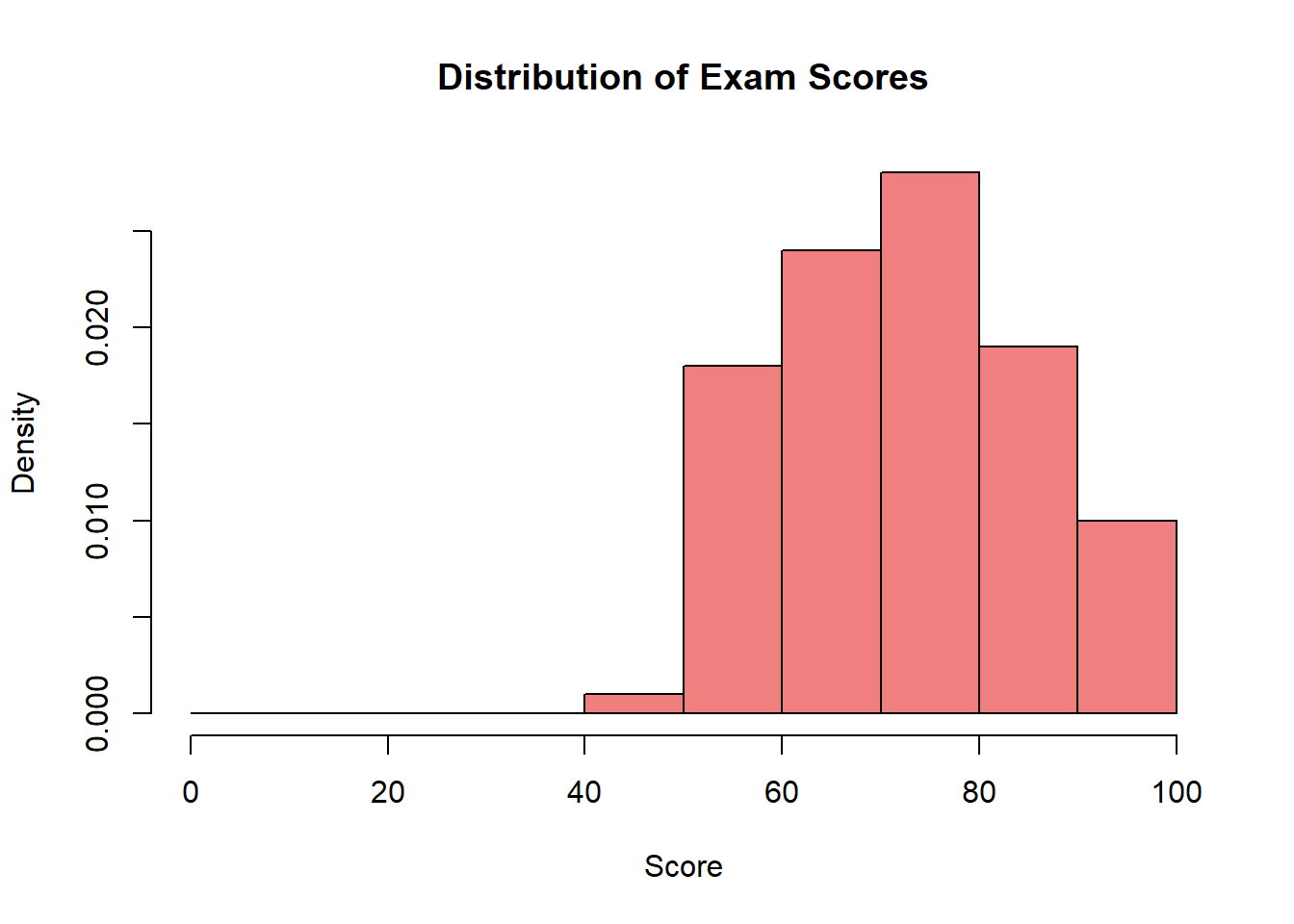

Density histogram adjusts for interval width and is used with density curves:

hist(exam_scores, breaks =seq(0, 100, by =10),freq =FALSE, # Creates density scalemain ="Distribution of Exam Scores",xlab ="Score",ylab ="Density",col ="lightcoral")

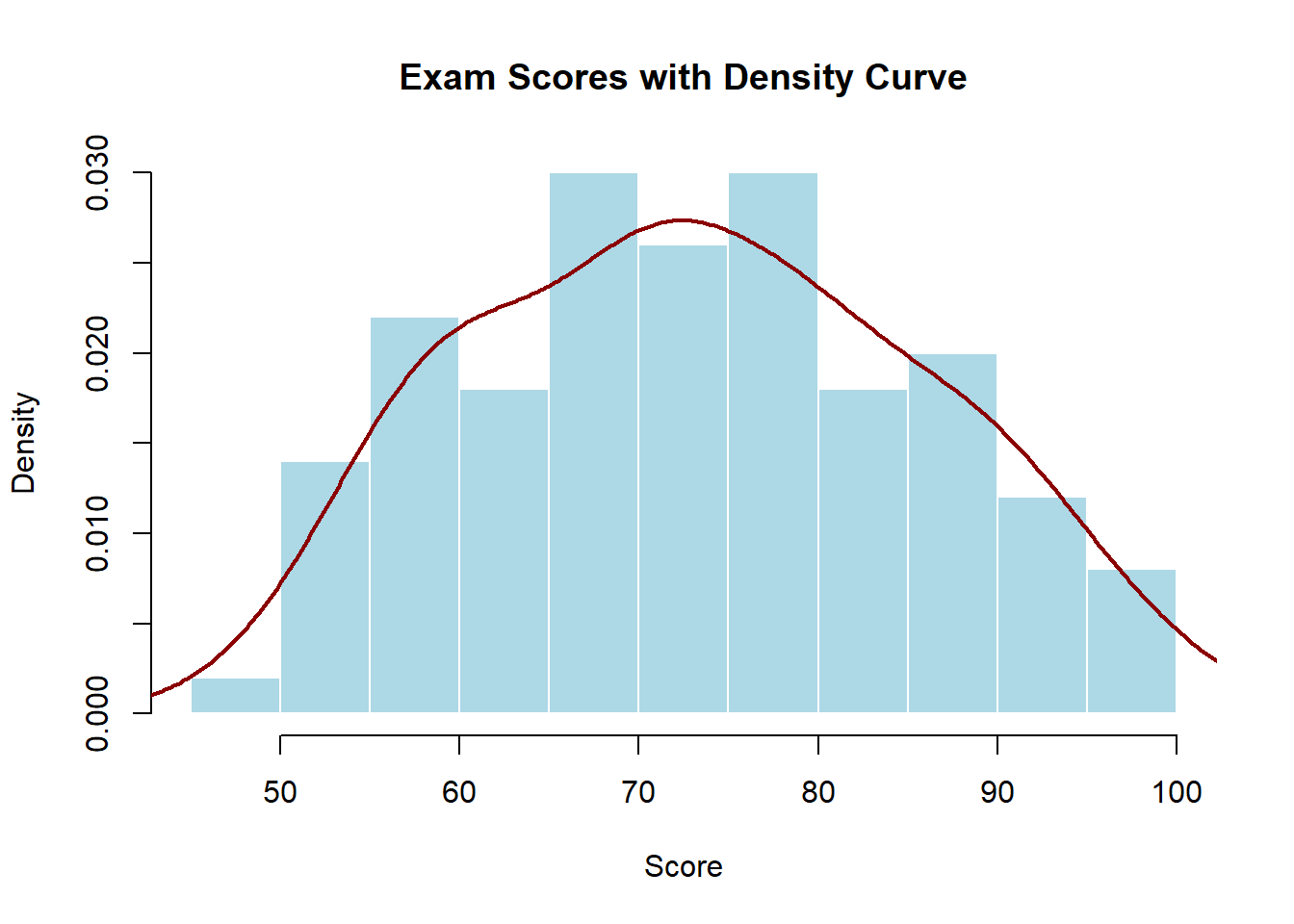

Density Curves

A density curve is a smooth line that approximates/models the shape of a distribution. Unlike histograms that show actual data in discrete bins, density curves show the overall pattern as a continuous function. The area under the entire curve always equals 1, and the area under any portion of the curve represents the proportion of observations in that range.

# Adding a density curve to a histogramhist(exam_scores, freq =FALSE,main ="Exam Scores with Density Curve",xlab ="Score",ylab ="Density",col ="lightblue",border ="white")lines(density(exam_scores), col ="darkred", lwd =2)

Density curves are particularly useful for:

Identifying the shape of the distribution (symmetric, skewed, bimodal)

Comparing multiple distributions on the same plot

Understanding the theoretical (true) distribution underlying your data

Tip

In statistics, a percentile indicates the relative position of a data point within a dataset by showing the percentage of observations that fall at or below that value. For example, if a student scores at the 90th percentile on a test, their score is equal to or higher than 90% of all other scores.

Quartiles are special percentiles that divide data into four equal parts: the first quartile (Q1, 25th percentile), second quartile (Q2, 50th percentile, also the median), and third quartile (Q3, 75th percentile). If Q1 = 65 points, then 25% of students scored 65 or below.

More generally, quantiles are values that divide data into equal-sized groups—percentiles divide into 100 parts, quartiles into 4 parts, deciles into 10 parts, and so on.

Visualizing Cumulative Frequency (*)

Cumulative frequency plots, also called ogives (pronounced “oh-jive”), display how frequencies accumulate across values. These plots use lines rather than bars and always increase from left to right, eventually reaching the total number of observations (for cumulative frequency) or 1.0 (for cumulative relative frequency).

Cumulative frequency plots are excellent for:

Finding percentiles and quartiles visually

Determining what proportion of data falls below or above a certain value

Comparing distributions of different groups

# Creating cumulative frequency datascore_breaks <-seq(0, 100, by =10)freq_counts <-hist(exam_scores, breaks = score_breaks, plot =FALSE)$countscumulative_freq <-cumsum(freq_counts)# Plotting cumulative frequencyplot(score_breaks[-1], cumulative_freq,type ="b", # both points and linesmain ="Cumulative Frequency of Exam Scores",xlab ="Score",ylab ="Cumulative Frequency",col ="darkblue",lwd =2,pch =19)grid()

For cumulative relative frequency (which is more commonly used):

The cumulative relative frequency curve makes it easy to read percentiles. For example, if you draw a horizontal line at 0.75 and see where it intersects the curve, the corresponding x-value is the 75th percentile—the score below which 75% of students fall.

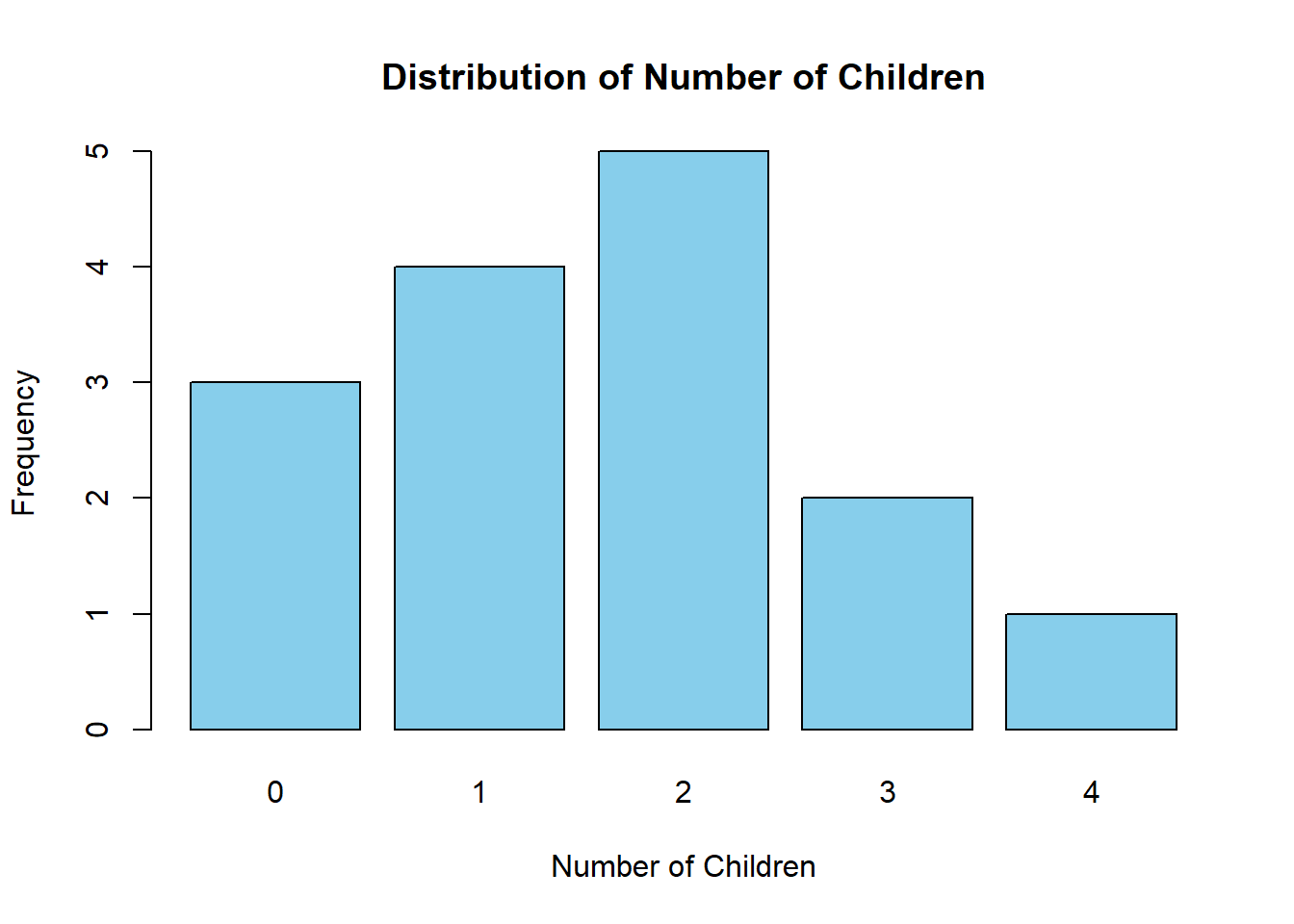

Discrete vs. Continuous Distributions

The type of variable you’re analyzing determines how you visualize its distribution:

Discrete distributions apply to variables that can only take specific, countable values. Examples include number of children in a family (0, 1, 2, 3…), number of customer complaints per day, or responses on a 5-point Likert scale.

For discrete data, we typically use:

Bar charts (with gaps between bars) rather than histograms

Frequency or relative frequency on the y-axis

Each distinct value gets its own bar

# Example: Number of children per familychildren <-c(0, 1, 2, 2, 1, 3, 0, 2, 1, 4, 2, 1, 0, 2, 3)barplot(table(children),main ="Distribution of Number of Children",xlab ="Number of Children",ylab ="Frequency",col ="skyblue")

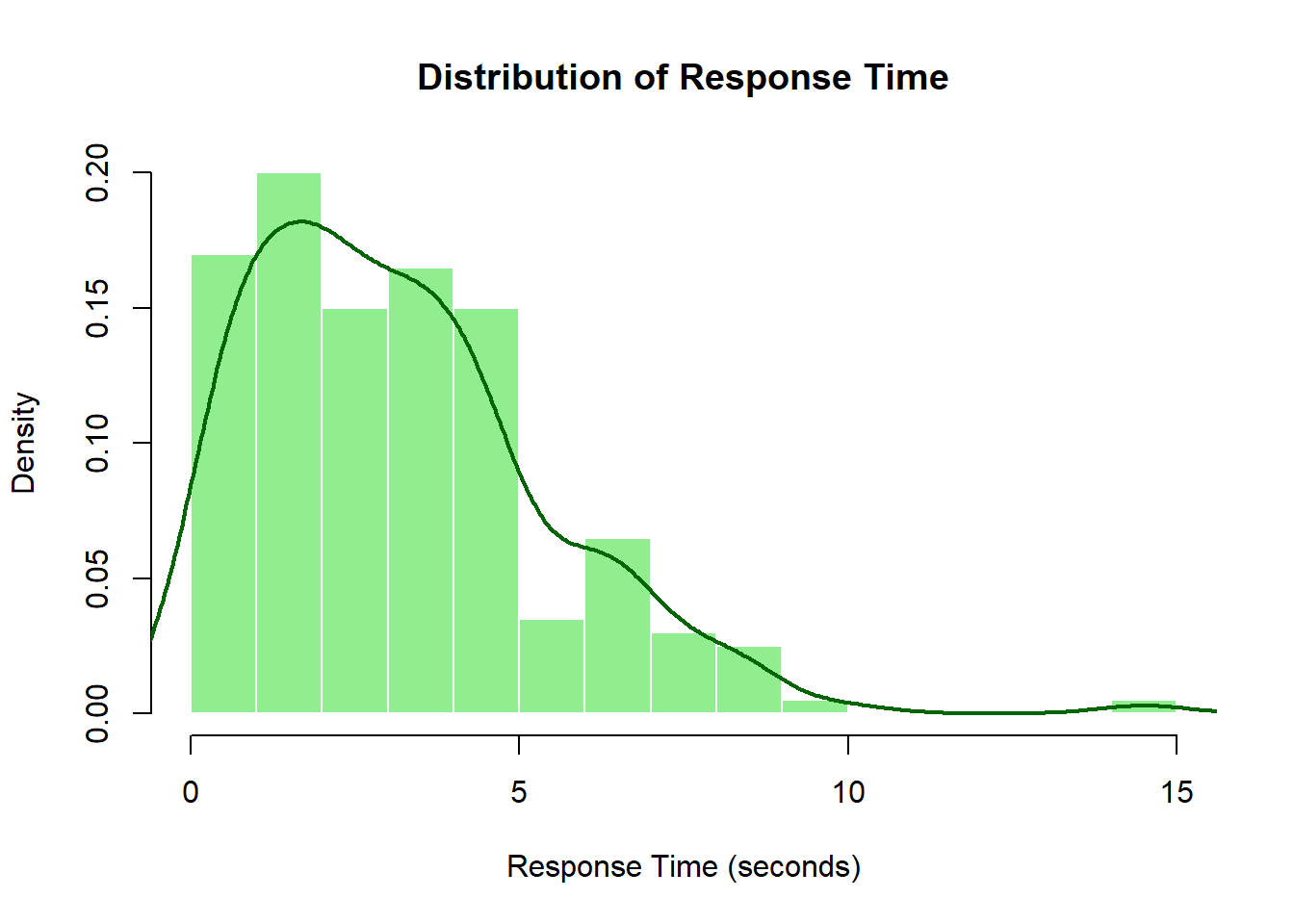

Continuous distributions apply to variables that can take any value within a range. Examples include temperature, response time, height, or turnout percentage.

For continuous data, we use:

Histograms (with touching bars) that group data into intervals

Density curves to show the smooth pattern

Density on the y-axis when using density curves

# Generate response time data (in seconds)set.seed(456) # For reproducibilityresponse_time <-rgamma(200, shape =2, scale =1.5)# Example: Response time distributionhist(response_time, breaks =15,freq =FALSE,main ="Distribution of Response Time",xlab ="Response Time (seconds)",ylab ="Density",col ="lightgreen",border ="white")lines(density(response_time), col ="darkgreen", lwd =2)

The key difference is that discrete distributions show probability at specific points, while continuous distributions show probability density across ranges. For continuous variables, the probability of any exact value is essentially zero—instead, we talk about the probability of falling within an interval.

Understanding whether your variable is discrete or continuous guides your choice of visualization and statistical methods, ensuring your analysis accurately represents the nature of your data.

Describing Distributions

Shape Characteristics:

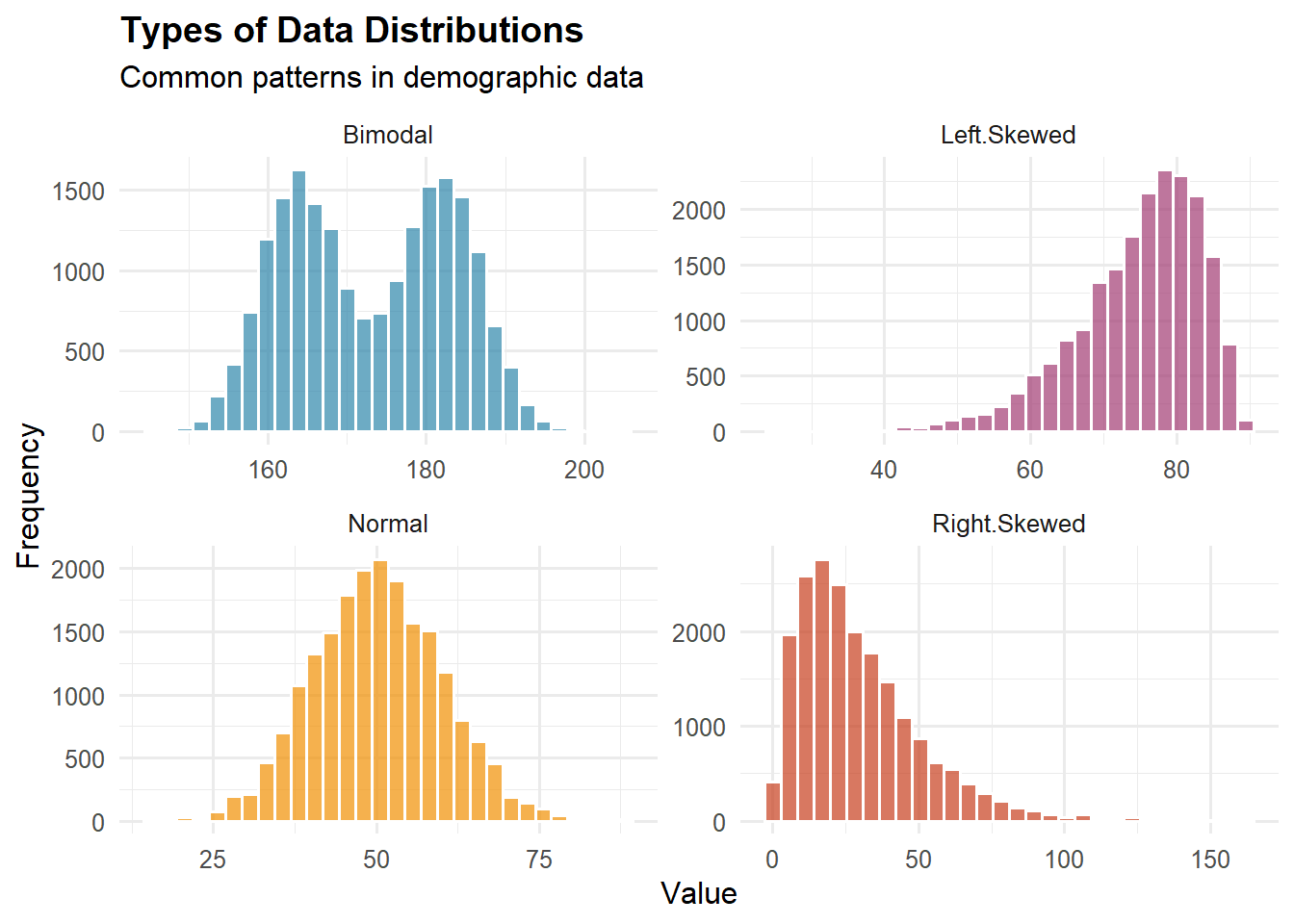

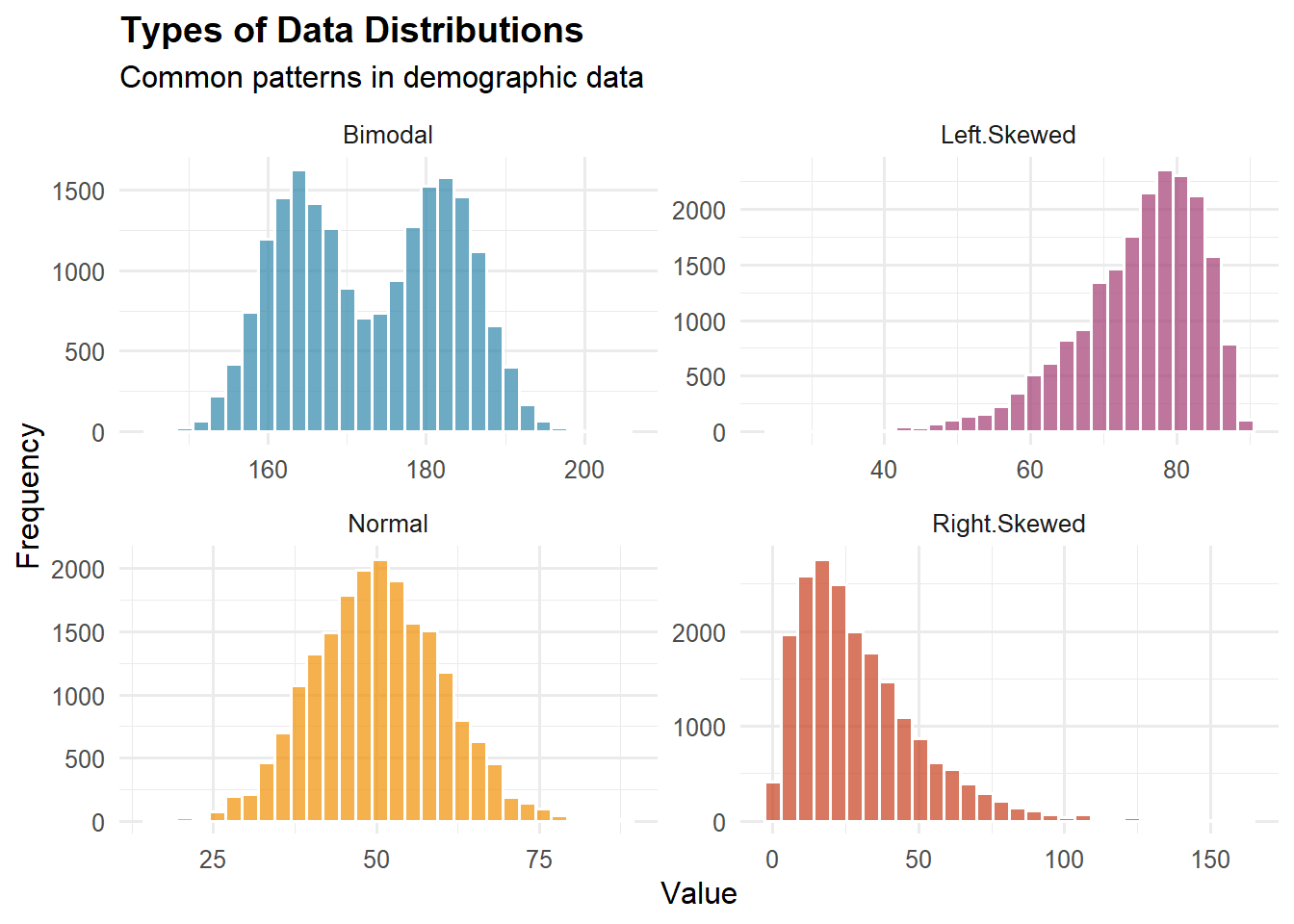

Symmetry vs. Skewness:

Symmetric: Mirror image around center (example: heights in homogeneous population)

Right-skewed (positive skew): Long tail to right (example: income, wealth)

Left-skewed (negative skew): Long tail to left (example: age at death in developed countries)

Example of Skewness Impact:

Income distribution in the U.S.:

Median household income: ~$70,000

Mean household income: ~$100,000

Mean > Median indicates right skew

A few very high incomes pull the mean up

Modality:

Unimodal: One peak (example: test scores)

Bimodal: Two peaks (example: height when mixing males and females)

Multimodal: Multiple peaks (example: age distribution in a college town—peaks at college age and middle age)

Important Probability Distributions:

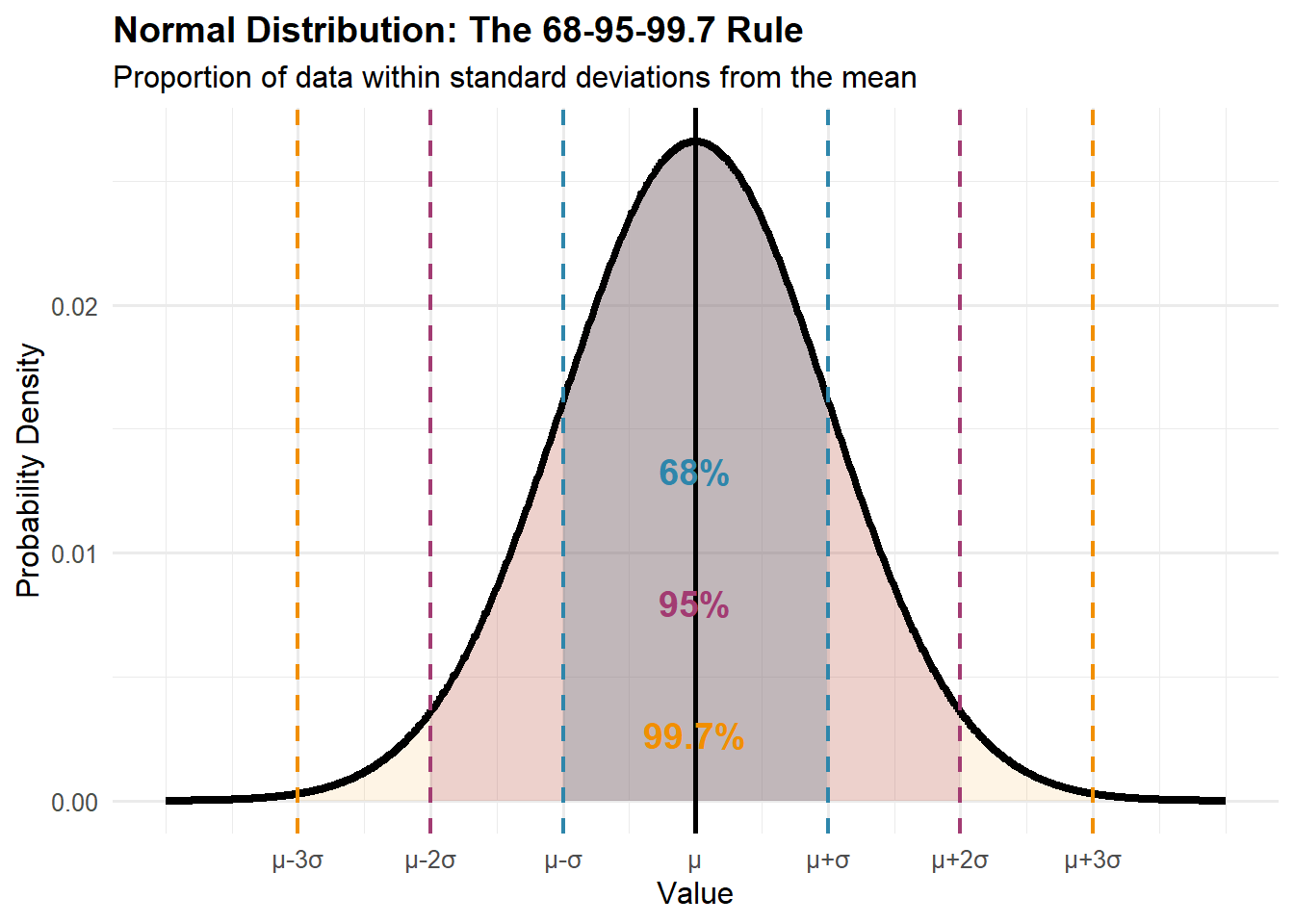

Normal (Gaussian) Distribution:

Bell-shaped, symmetric

Characterized by mean (\mu) and standard deviation (\sigma)

About 68% of values within \mu \pm \sigma

About 95% within \mu \pm 2\sigma

About 99.7% within \mu \pm 3\sigma

Demographic Applications:

Heights within homogeneous populations

Measurement errors

Sampling distributions of means (Central Limit Theorem)

Binomial Distribution:

Number of successes in n independent trials

Each trial has probability p of success

Mean = np, Variance = np(1-p)

Example: Number of male births out of 100 births (p \approx 0.512)

Poisson Distribution:

Count of events in fixed time/space

Mean = Variance = \lambda

Good for rare events

Demographic Applications:

Number of deaths per day in small town

Number of births per hour in hospital

Number of accidents at intersection per month

Visualizing Frequency Distributions (*)

Histogram: For continuous data, shows frequency with bar heights.

X-axis: Value ranges (bins)

Y-axis: Frequency or density

No gaps between bars (continuous data)

Bin width affects appearance

Bar Chart: For categorical data, shows frequency with separated bars.

X-axis: Categories

Y-axis: Frequency

Gaps between bars (discrete categories)

Order may or may not matter

Cumulative Distribution Function (CDF): Shows proportion of values ≤ each point of data.

Always increases (or stays flat)

Starts at 0, ends at 1

Steep slopes indicate common values

Flat areas indicate rare values

Box Plot (Box-and-Whisker Plot): A visual summary that displays the distribution’s key statistics using five key values.

The Five-Number Summary:

Minimum: Leftmost whisker end (excluding outliers)

Q1 (First Quartile): Left edge of the box (25th percentile)

Median (Q2): Line inside the box (50th percentile)

Q3 (Third Quartile): Right edge of the box (75th percentile)

Maximum: Rightmost whisker end (excluding outliers)

What It Reveals:

Skewness: If median line is off-center in the box, or whiskers are unequal

Spread: Wider boxes and longer whiskers indicate more variability

Outliers: Immediately visible as separate points

Symmetry: Equal whisker lengths and centered median suggest normal distribution

Quick Interpretation:

Narrow box = consistent data

Long whiskers = wide range of values

Many outliers = potential data quality issues or interesting extreme cases

Median closer to Q1 = right-skewed data (tail extends right)

Median closer to Q3 = left-skewed data (tail extends left)

Box plots are especially useful for comparing multiple groups side-by-side!

1.8 Variables and Measurement Scales

A variable is any characteristic that can take different values across units of observation.

Measurement: Transforming Concepts into Numbers

The Political World is Full of Data

Political science has evolved from a primarily theoretical discipline to one that increasingly relies on empirical evidence. Whether we’re studying:

Election outcomes: Why do people vote the way they do?

Public opinion: What shapes attitudes toward immigration or climate policy?

International relations: What factors predict conflict between nations?

Policy effectiveness: Did a new education policy actually improve outcomes?

We need systematic ways to analyze data and draw conclusions that go beyond anecdotes and personal impressions.

Consider this question: “Does democracy lead to economic growth?”

Your intuition might suggest yes—democratic countries tend to be wealthier. But is this causation or correlation? Are there exceptions? How confident can we be in our conclusions?

Statistics provides the tools to move from hunches to evidence-based answers, helping us distinguish between what seems true and what actually is true.

The Challenge of Measurement in Social Sciences

In social sciences, we often struggle with the fact that key concepts do not translate directly into numbers:

Quantitative Variables represent amounts or quantities and can be:

Continuous Variables: Can take any value within a range, limited only by measurement precision.

Age (22.5 years, 22.51 years, 22.514 years…)

Income ($45,234.67)

Height (175.3 cm)

Population density (432.7 people per square kilometer)

Discrete Variables: Can only take specific values, usually counts.

Number of children in a family (0, 1, 2, 3…)

Number of marriages (0, 1, 2…)

Number of rooms in a dwelling (1, 2, 3…)

Number of migrants entering a country per year

Qualitative Variables represent categories or qualities and can be:

Nominal Variables: Categories with no inherent order.

Country of birth (USA, Mexico, Canada…)

Religion (Christian, Muslim, Hindu, Buddhist…)

Blood type (A, B, AB, O)

Cause of death (heart disease, cancer, accident…)

Ordinal Variables: Categories with a meaningful order but unequal intervals.

Education level (no schooling, primary, secondary, tertiary)

Satisfaction with healthcare (very dissatisfied, dissatisfied, neutral, satisfied, very satisfied)

Socioeconomic status (low, middle, high)

Self-rated health (poor, fair, good, excellent)

Measurement Scales

Understanding measurement scales is crucial because they determine which statistical methods are appropriate:

Nominal Scale: Categories only—we can count frequencies but cannot order or perform arithmetic. Example: We can say 45% of residents were born locally, but we cannot calculate an “average birthplace.”

Ordinal Scale: Order matters but differences between values are not necessarily equal. Example: The difference between “poor” and “fair” health may not equal the difference between “good” and “excellent” health.

Interval Scale: Equal intervals between values but no true zero point. Example: Temperature in Celsius—the difference between 20°C and 30°C equals the difference between 30°C and 40°C, but 0°C doesn’t mean “no temperature.”

Ratio Scale: Equal intervals with a true zero point, allowing all mathematical operations. Example: Income—$40,000 is twice as much as $20,000, and $0 means no income.

1.9 Parameters, Statistics, Estimands, Estimators, and Estimates

Statistical inference is the process of learning unknown features of a population from finite samples. This section introduces five core ideas.

Quick comparison (summary table)

Term

What is it?

Random?

Typical notation

Example

Estimand

Precisely defined target quantity

No

words (specification)

“Median household income in CA on 2024-01-01.”

Parameter

The true population value of that quantity

No*

\theta,\ \mu,\ p,\ \beta

True mean age at first birth in France (2023)

Estimator

A rule/formula mapping data to an estimate

—

\hat\theta = g(X_1,\dots,X_n)

\bar X, \hat p = X/n, OLS \hat\beta

Statistic

Any function of the sample (includes estimators)

Yes

\bar X,\ s^2,\ r

Sample mean from n=500 births

Estimate

The numerical value obtained from the estimator

No

a number

\hat p = 0.433

*Fixed for the population/time frame you define; it can differ across places/times.

Parameter

A parameter is a numerical characteristic of a population—fixed but unknown.

Common parameters:\mu (mean), \sigma^2 (variance), p (proportion), \beta (regression effect), \lambda (rate).

Example. The true mean age at first birth for all women in France, 2023, is a parameter \mu. We do not know it without full population data.

Note

Notation. A common convention is Greek letters for population parameters and Roman letters for sample statistics. Consistency matters more than the specific symbols chosen.

Statistic

A statistic is any function of sample data. Statistics vary from sample to sample.

Examples:\bar x (sample mean), s^2 (sample variance), \hat p (sample proportion), r (sample correlation), b (sample regression slope).

Example. From a random sample of 500 births, \bar x = 30.9 years; a different sample might give 31.4.

Estimand

The estimand is the target quantity—specified clearly enough that two researchers would compute the same number from the same full population.

Well-specified estimands

“Median household income in California on 2024-01-01.”

“Male–female difference in life expectancy for births in Sweden, 2023.”

“Proportion of 25–34 year-olds in urban areas with tertiary education.”

Warning

Why precise definitions matter. “Unemployment rate” is ambiguous unless you specify (i) who counts as unemployed, (ii) age range, (iii) geography, (iv) time window. Different definitions lead to different parameters (e.g., U-1 … U-6 in the U.S.).

Estimator

An estimator is the rule that turns data into an estimate.

Bias — is the estimator centered on the truth? If the same study were repeated many times, an unbiased estimator would average to the true value. A biased estimator would systematically miss it (too high or too low).

Variance — how much do estimates differ across samples? Even without bias, repeated samples will not give exactly the same number. Lower variance means more stable results from sample to sample.

Mean Squared Error (MSE) — overall accuracy in one measure. MSE combines both components:

\mathrm{MSE}(\hat\theta)=\mathrm{Var}(\hat\theta)+\big(\mathrm{Bias}(\hat\theta)\big)^2.

Lower MSE is better. An estimator with a small bias but much lower variance can have a lower MSE than an unbiased but highly variable one.

Efficiency — comparative precision among estimators. Among unbiased estimators that target the same parameter with the same data, the more efficient estimator has the smaller variance. When small bias is allowed, compare using MSE instead.

Sources of precision (common cases)

Sample mean (simple random sample):

\operatorname{Var}(\bar X)=\frac{\sigma^2}{n},\qquad

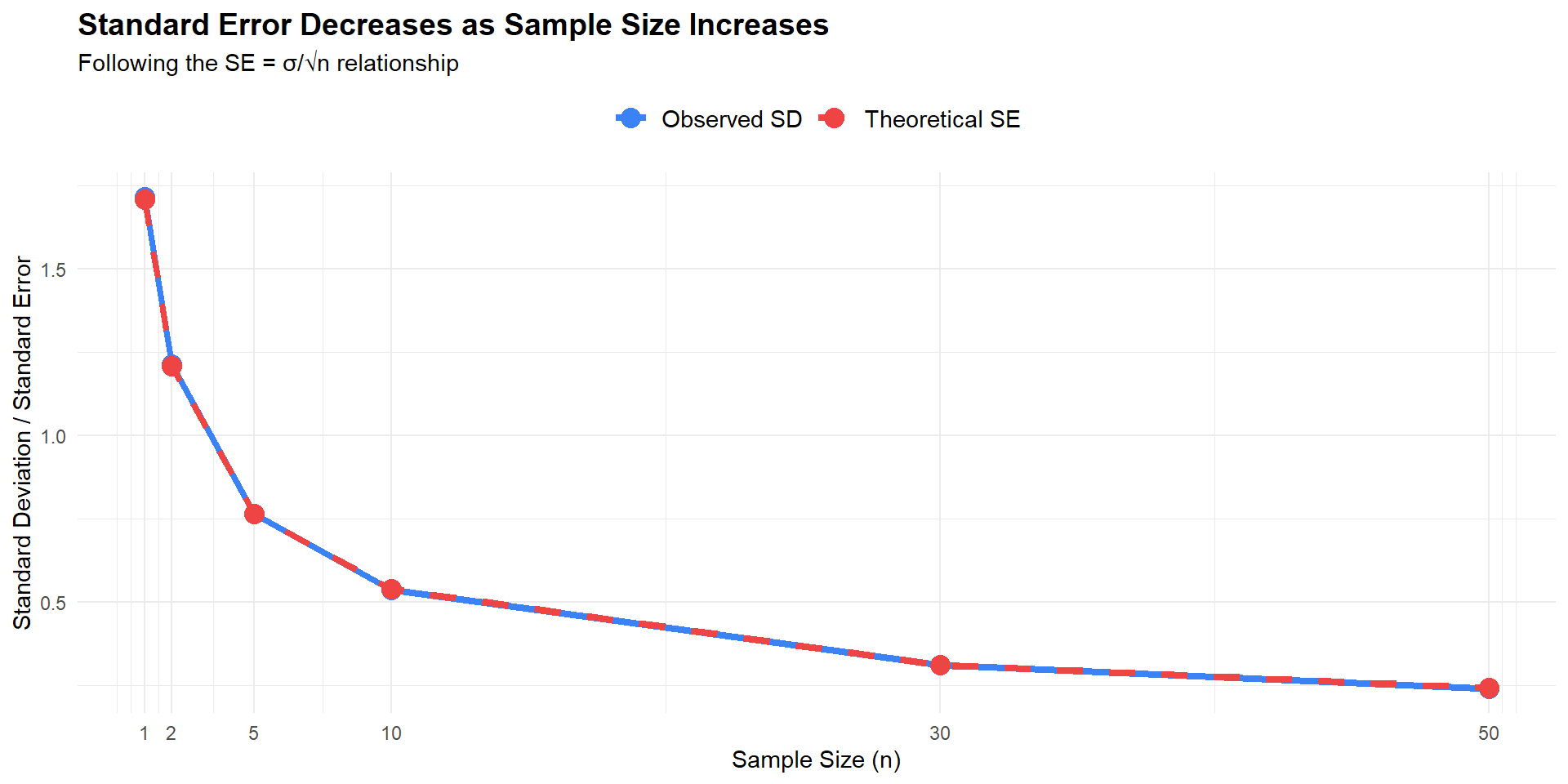

\mathrm{SE}(\bar X)=\frac{\sigma}{\sqrt{n}}.

Larger n reduces SE at the rate 1/\sqrt{n}.

Design effects: clustering, stratification, and weights can change variance. Match your SE method to the sampling design.

Tip

Practical guidance

Define the estimand precisely (population, time, unit, and definition).

Select an estimator that directly targets that estimand.

Among unbiased options, prefer lower variance (greater efficiency).

When bias–variance trade-offs are relevant, compare MSE.

Report the estimate and its uncertainty (SE or CI), and state key assumptions.

Estimate

An estimate is the numerical value obtained after applying the estimator to the data.

Worked example

Estimand: Approval share among all U.S. adults today.

Parameter: p (unknown true approval).

Estimator: \hat p = X/n.

Sample: n=1{,}500, approvals X=650.

Estimate: \hat p = 650/1500 = 0.433 (43.3%).

Common confusions and clarifications

Parameter vs statistic: Population quantity vs sample-derived quantity.

Estimator vs estimate: Procedure vs numerical result.

Time index: Parameters can change over time (e.g., Q2 vs Q3).

Definition first: Specify the estimand before choosing the estimator.

Understanding Different Types of Unpredictability

Not all uncertainty is the same. Understanding different sources of unpredictability helps us choose appropriate statistical methods and interpret results correctly.

Concept

What is it?

Source of unpredictability

Example

Randomness

Individual outcomes are uncertain, but the probability distribution is known or modeled.

Fluctuations across realizations; lack of information about a specific outcome.

Dice roll, coin toss, polling sample

Chaos

Deterministic dynamics highly sensitive to initial conditions (butterfly effect).

Tiny initial differences grow rapidly → large trajectory divergences.

Weather forecasting, double pendulum, population dynamics

Entropy

A measure of uncertainty/dispersion (information-theoretic or thermodynamic).

Larger when outcomes are more evenly distributed (less predictive information).

Shannon entropy in data compression

“Haphazardness” (colloquial)

A felt lack of order without an explicit model; a mixture of mechanisms.

No structured description or stable rules; overlapping processes.

Traffic patterns, social media trends

Quantum randomness

A single outcome is not determined; only the distribution is specified (Born rule).

Fundamental (ontological) indeterminacy of individual measurements.

Electron spin measurement, photon polarization

Key Distinctions for Statistical Practice

Deterministic chaos ≠ statistical randomness: A chaotic system is fully deterministic yet practically unpredictable due to extreme sensitivity to initial conditions. Statistical randomness, by contrast, models uncertainty via probability distributions where individual outcomes are genuinely uncertain.

Why this matters: In statistics, we typically model phenomena as random processes, assuming we can specify probability distributions even when individual outcomes are unpredictable. This assumption underlies most statistical inference.

Quantum Mechanics and Fundamental Randomness

In the Copenhagen interpretation, randomness is fundamental (ontological): a single outcome cannot be predicted, but the probability distribution is given by the Born rule.

This represents true randomness at the most basic level of nature.

1.10 Statistical Error and Uncertainty

Introduction: Why Uncertainty Matters

No measurement or estimate is perfect. Understanding different types of error is crucial for interpreting results and improving study design.

The Central Challenge

Every time we use a sample to learn about a population, we introduce uncertainty. The key is to:

Quantify this uncertainty honestly

Distinguish between different sources of error

Communicate results transparently

Types of Error

Random Error

Random error represents unpredictable fluctuations that vary from observation to observation without a consistent pattern. These errors arise from various sources of natural variability in the data collection and measurement process.

Key Characteristics

Unpredictable Direction: Sometimes too high, sometimes too low

No Consistent Pattern: Varies randomly across observations

Averages to Zero: Over many measurements, positive and negative errors cancel out

Quantifiable: Can be estimated and reduced through appropriate methods

Random error encompasses several subtypes:

Sampling Error

Sampling error is the most common type of random error—it arises because we observe a sample rather than the entire population. Different random samples from the same population will yield different estimates purely by chance.

Key properties: